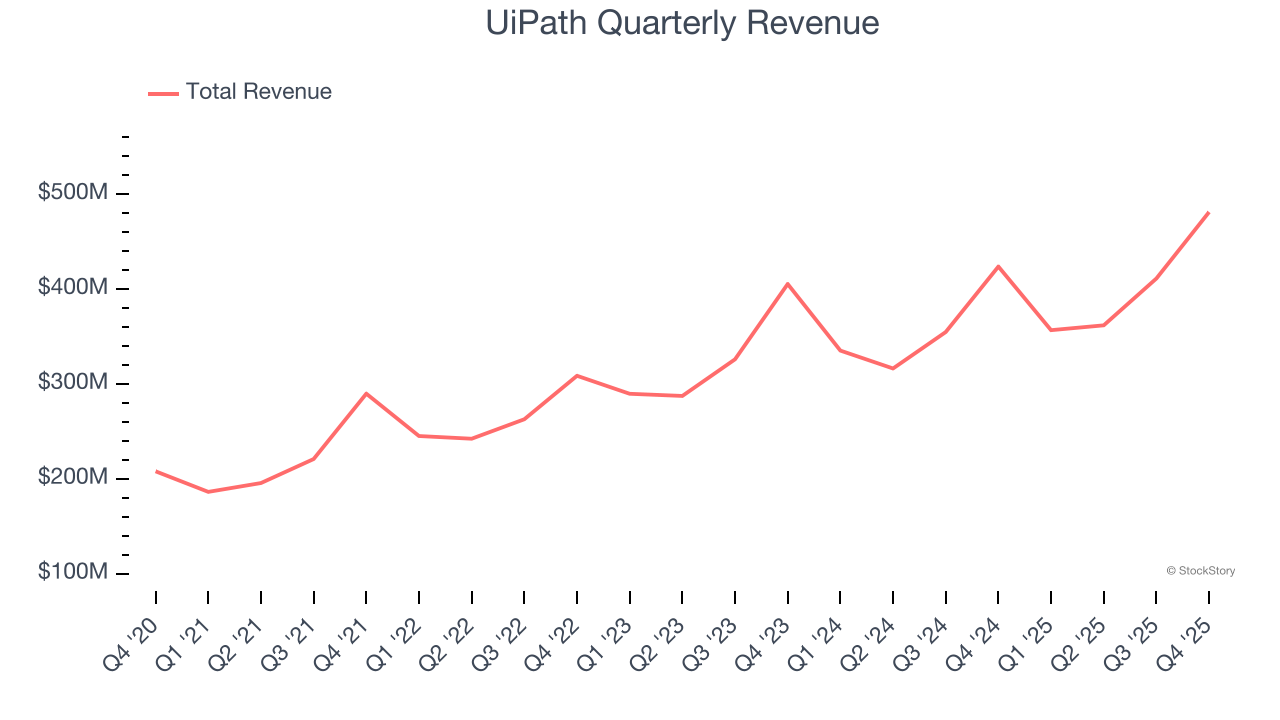

Automation software company UiPath (NYSE: PATH) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 13.6% year on year to $481.1 million. Guidance for next quarter’s revenue was better than expected at $397.5 million at the midpoint, 0.7% above analysts’ estimates. Its non-GAAP profit of $0.30 per share was 17.8% above analysts’ consensus estimates.

Is now the time to buy UiPath? Find out by accessing our full research report, it’s free.

UiPath (PATH) Q4 CY2025 Highlights:

- Revenue: $481.1 million vs analyst estimates of $464.8 million (13.6% year-on-year growth, 3.5% beat)

- Adjusted EPS: $0.30 vs analyst estimates of $0.25 (17.8% beat)

- Adjusted Operating Income: $150.1 million vs analyst estimates of $139.8 million (31.2% margin, 7.3% beat)

- Revenue Guidance for Q1 CY2026 is $397.5 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 16.7%, up from 7.9% in the same quarter last year

- Free Cash Flow Margin: 37.3%, up from 6.1% in the previous quarter

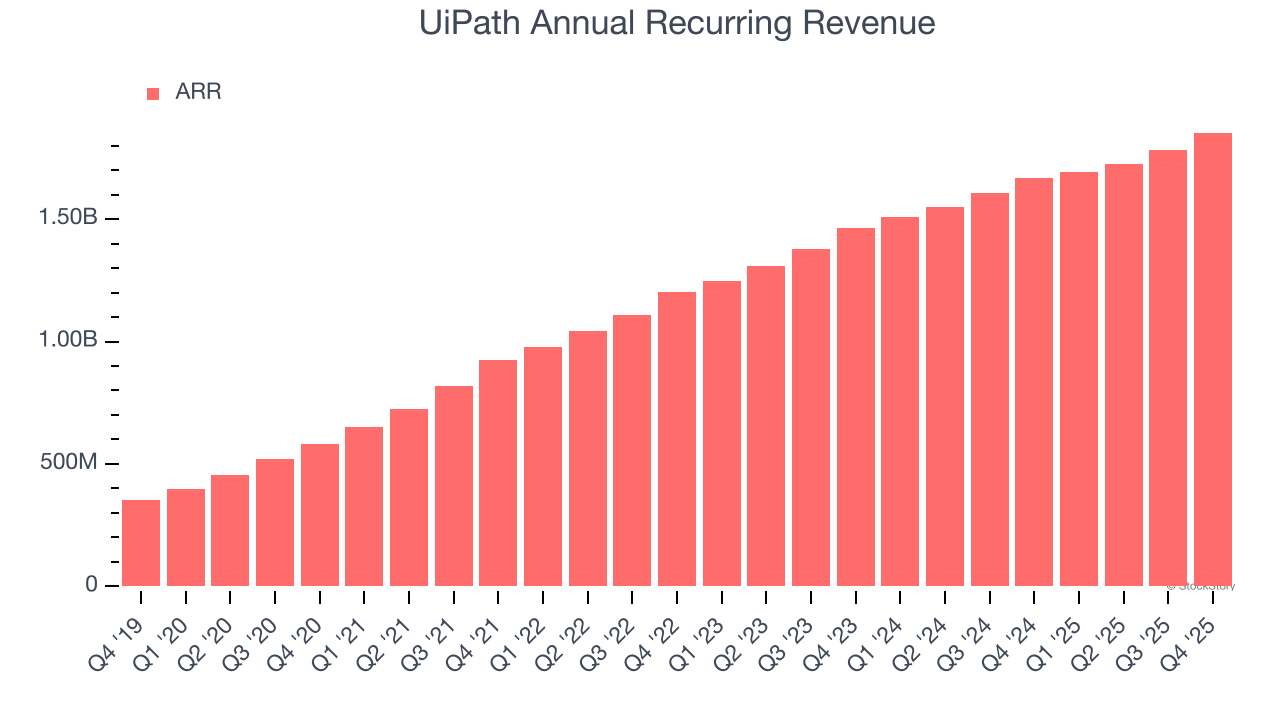

- Annual Recurring Revenue: $1.85 billion vs analyst estimates of $1.85 billion (11.2% year-on-year growth, in line)

- Market Capitalization: $6.20 billion

Company Overview

Starting with robotic process automation (RPA) and evolving into a comprehensive automation powerhouse, UiPath (NYSE: PATH) provides an AI-powered business automation platform that enables organizations to create software robots that mimic human actions to streamline repetitive tasks and processes.

Revenue Growth

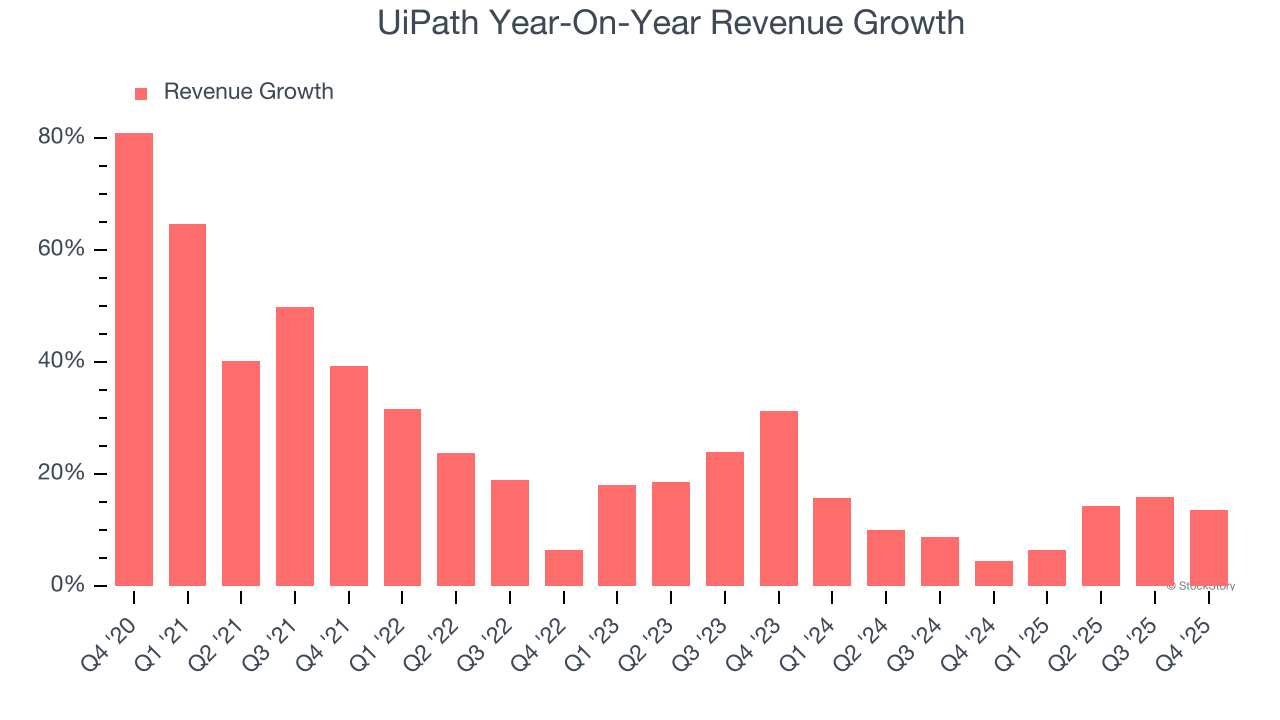

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, UiPath grew its sales at a decent 21.5% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. UiPath’s recent performance shows its demand has slowed as its annualized revenue growth of 11% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, UiPath reported year-on-year revenue growth of 13.6%, and its $481.1 million of revenue exceeded Wall Street’s estimates by 3.5%. Company management is currently guiding for a 11.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

UiPath’s ARR came in at $1.85 billion in Q4, and over the last four quarters, its growth was underwhelming as it averaged 11.4% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in securing longer-term commitments.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

UiPath is quite efficient at acquiring new customers, and its CAC payback period checked in at 31 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

Key Takeaways from UiPath’s Q4 Results

It was encouraging to see UiPath beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 1.6% to $12.24 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).