Shareholders of Angi would probably like to forget the past six months even happened. The stock dropped 55.6% and now trades at $5.44. This may have investors wondering how to approach the situation.

Is now the time to buy Angi, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Angi Not Exciting?

Even though the stock has become cheaper, we’re swiping left on Angi for now. Here are three reasons you should be careful with ANGI, plus one stock we’d rather own.

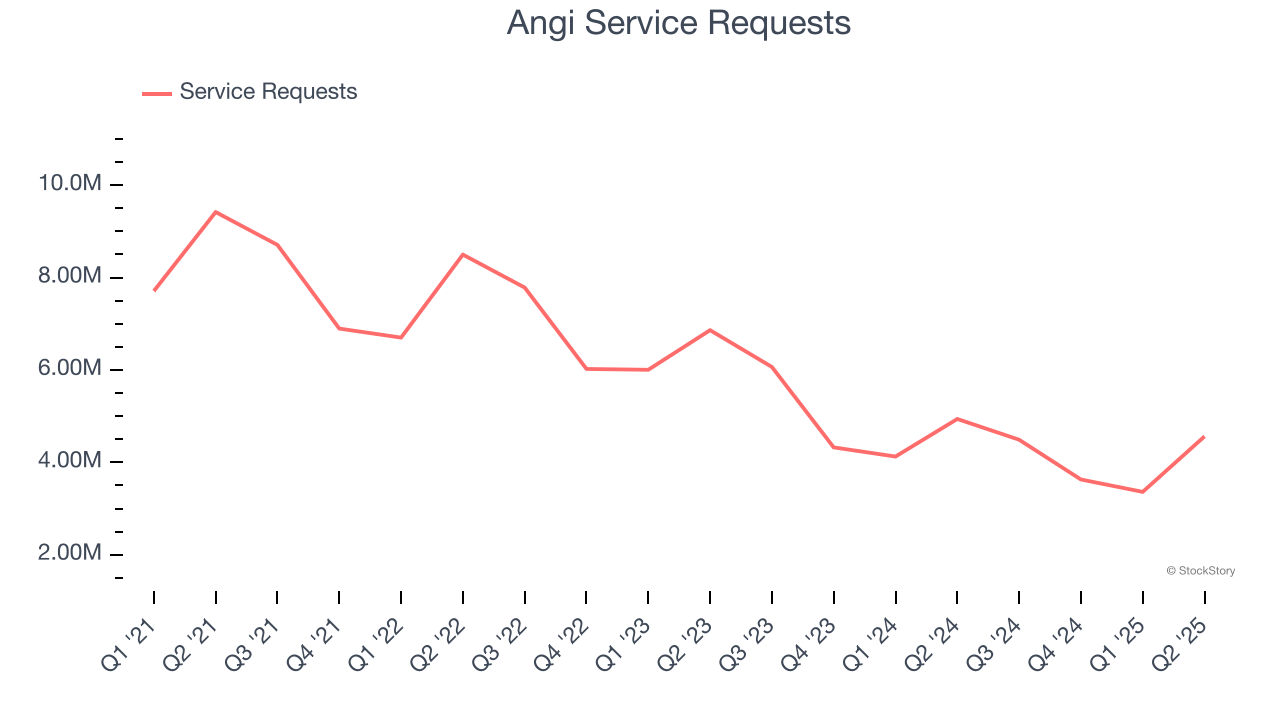

1. Declining Service Requests Reflect Product Weakness

As a gig economy marketplace, Angi generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Angi struggled with new customer acquisition over the last two years as its service requests have declined by 19.2% annually. This performance isn’t ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Angi wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Angi’s revenue to drop by 3.6%. it’s tough to feel optimistic about a company facing demand difficulties.

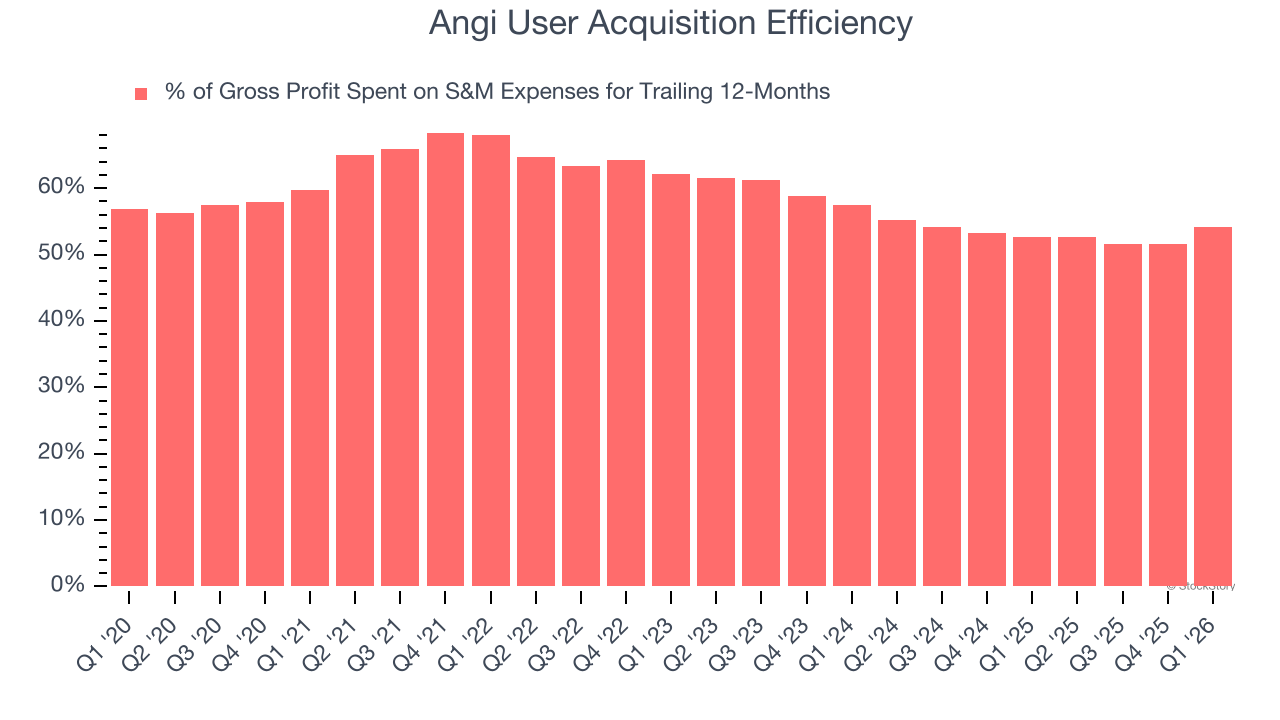

3. Poor Marketing Efficiency Drains Profits

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Angi grow from a combination of product virality, paid advertisement, and incentives.

It’s expensive for Angi to acquire new users as the company has spent 54.2% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates that Angi’s product offering can be easily replicated and that it must continue investing to maintain an acceptable growth trajectory.

Final Judgment

Angi isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 4.3× forward EV/EBITDA (or $5.44 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Angi

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.