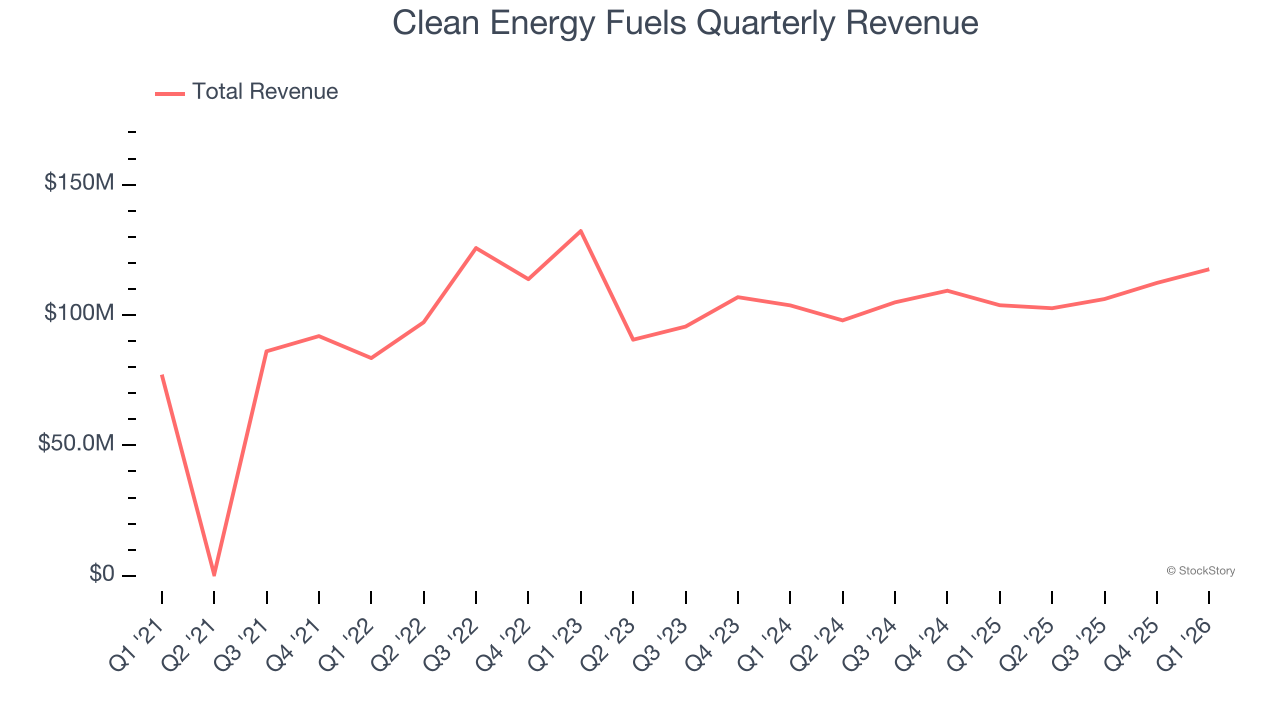

Alternative fuel provider Clean Energy Fuels (NASDAQ: CLNE) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 13.3% year on year to $117.6 million. Its non-GAAP loss of $0.01 per share was $0.02 above analysts’ consensus estimates.

Is now the time to buy Clean Energy Fuels? Find out by accessing our full research report, it’s free.

Clean Energy Fuels (CLNE) Q1 CY2026 Highlights:

- Revenue: $117.6 million vs analyst estimates of $99.2 million (13.3% year-on-year growth, 18.5% beat)

- Adjusted EPS: -$0.01 vs analyst estimates of -$0.03 ($0.02 beat)

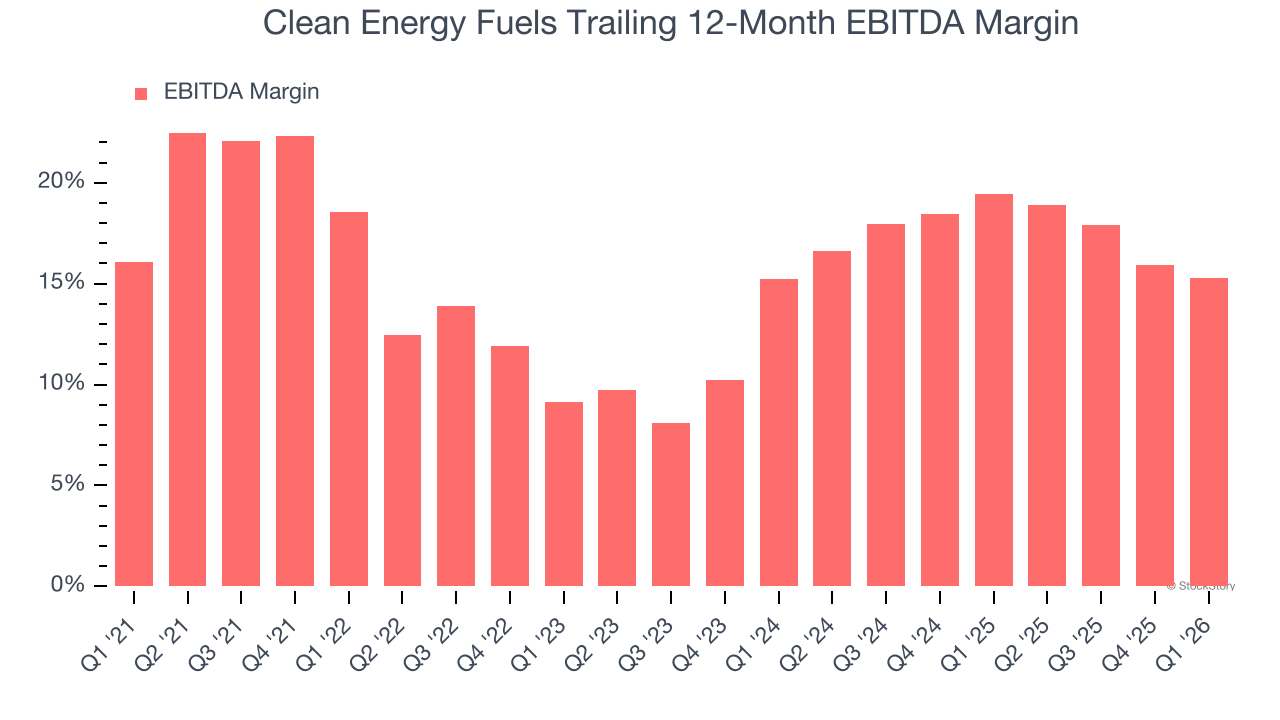

- Adjusted EBITDA: $16.6 million vs analyst estimates of $13.5 million (14.1% margin, 22.9% beat)

- Operating Margin: -2.5%, up from -122% in the same quarter last year

- Market Capitalization: $491.5 million

Company Overview

Operating the largest network of natural gas fueling stations in North America with over 600 locations, Clean Energy Fuels (NASDAQ: CLNE) supplies renewable natural gas and conventional natural gas as fuel for commercial vehicle fleets.

Revenue Growth

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Unfortunately, Clean Energy Fuels’s 9.2% annualized revenue growth over the last five years was mediocre. This was below our standard for the energy upstream and integrated energy sector and is a tough starting point for our analysis.

Even a long stretch in Energy can be shaped by a single commodity cycle, so extending the view to ten years adds another perspective and reveals which companies are built to grow regardless of the pricing regime. Clean Energy Fuels’s annualized revenue growth of 1.1% over the last ten years is below its five-year trend, but we still think the results were respectable.

This quarter, Clean Energy Fuels reported year-on-year revenue growth of 13.3%, and its $117.6 million of revenue exceeded Wall Street’s estimates by 18.5%.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted EBITDA Margin

Clean Energy Fuels was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 15.1% was among the worst in the energy upstream and integrated energy sector.

Looking at the trend in its profitability, Clean Energy Fuels’s EBITDA margin decreased by 3.3 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Clean Energy Fuels’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Clean Energy Fuels generated an EBITDA margin profit margin of 14.1%, down 2.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue. This adjusted EBITDA beat Wall Street’s estimates by 22.9%.

Cash Is King

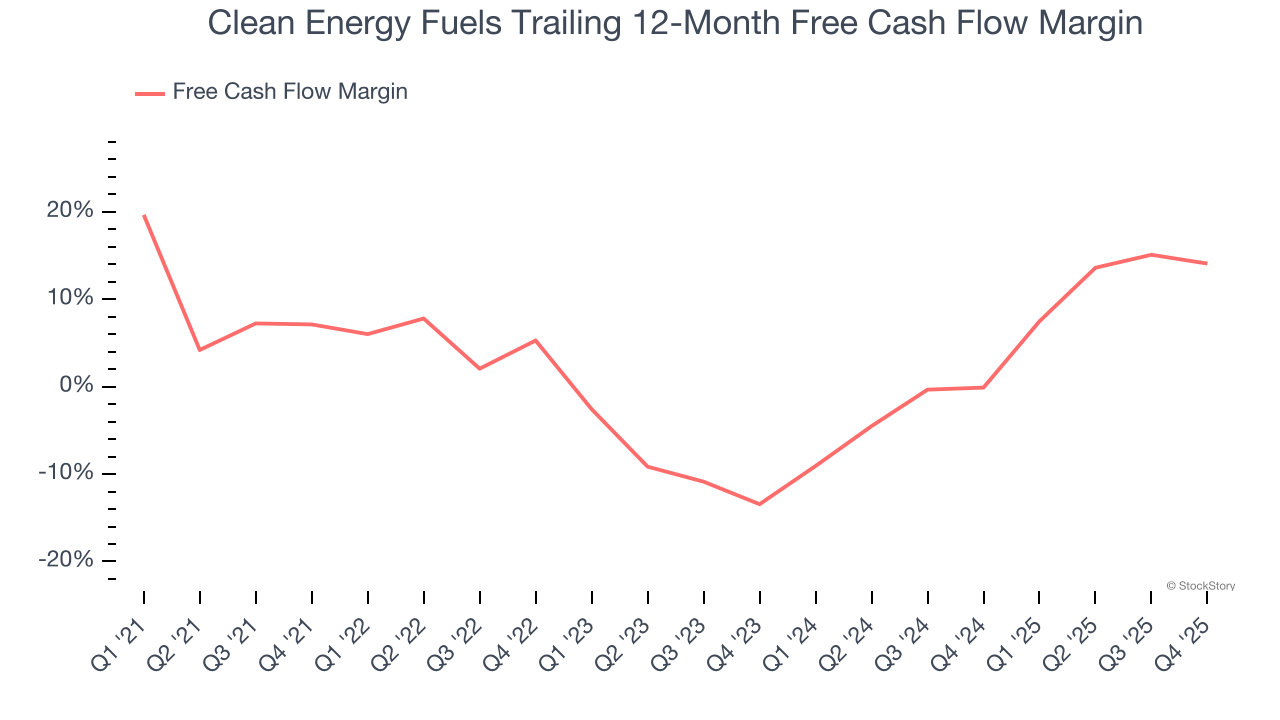

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Clean Energy Fuels has shown weak cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 2.3%, below what we’d expect for an upstream and integrated energy business.

While the level of free cash flow margins is important, their consistency matters just as much.

Clean Energy Fuels’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 46.5 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Clean Energy Fuels? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Key Takeaways from Clean Energy Fuels’s Q1 Results

It was good to see Clean Energy Fuels beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 1.9% to $2.27 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).