Over the past six months, Impinj’s stock price fell to $144.76. Shareholders have lost 15.7% of their capital, which is disappointing considering the S&P 500 has climbed by 8.2%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Impinj, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Impinj Not Exciting?

Even though the stock has become cheaper, we’re sitting this one out for now. Here are three reasons we avoid PI, plus one stock we’d rather own.

1. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Impinj’s revenue to rise by 9.3%, close to its 21.5% annualized growth for the past five years. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet.

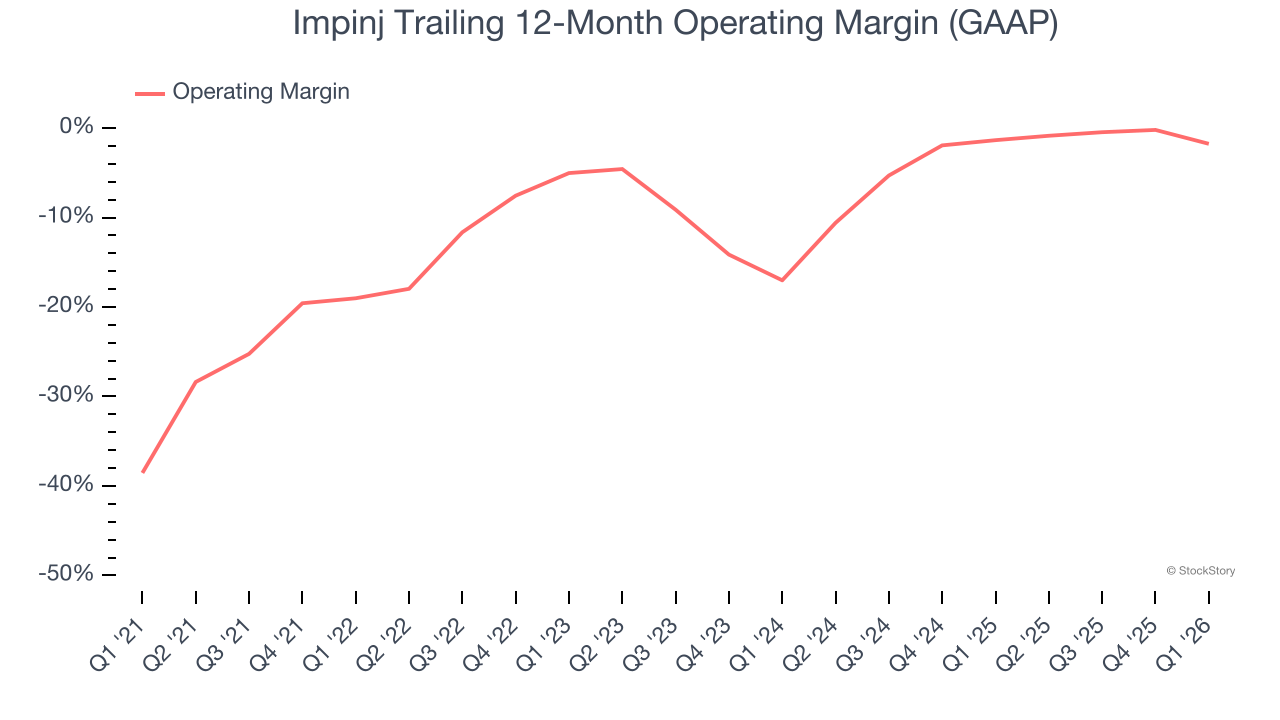

2. Operating Losses Sound the Alarm

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Impinj’s high expenses have contributed to an average operating margin of negative 1.6% over the last two years. Unprofitable semiconductor companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

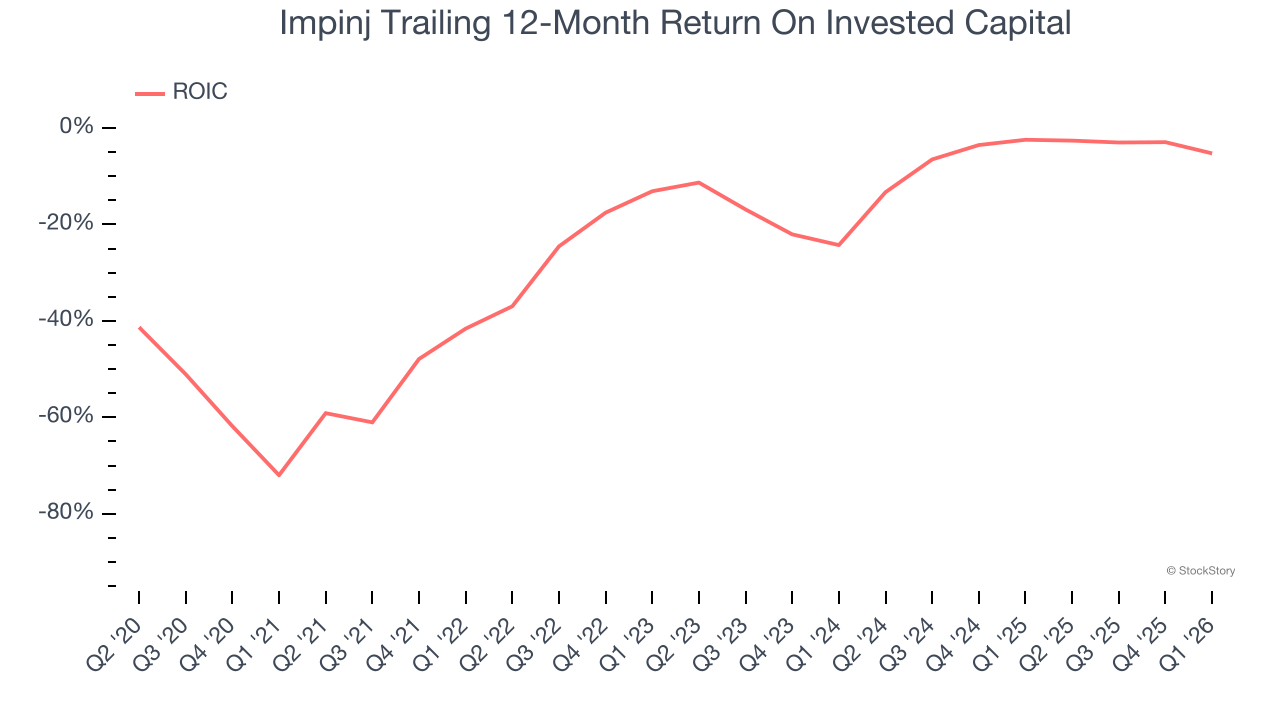

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Impinj’s five-year average ROIC was negative 17.3%, meaning management lost money while trying to expand the business. Its returns were among the worst in the semiconductor sector.

Final Judgment

Impinj isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 68.9× forward P/E (or $144.76 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d suggest looking at the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+214% between June 2020 and June 2025). Find your next big winner with StockStory today.