The past six months have been a windfall for The New York Times’s shareholders. The company’s stock price has jumped 53.6%, hitting $85.39 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in The New York Times, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think The New York Times Will Underperform?

We’re glad investors have benefited from the price increase, but we're cautious about The New York Times. Here are three reasons there are better opportunities than NYT and a stock we'd rather own.

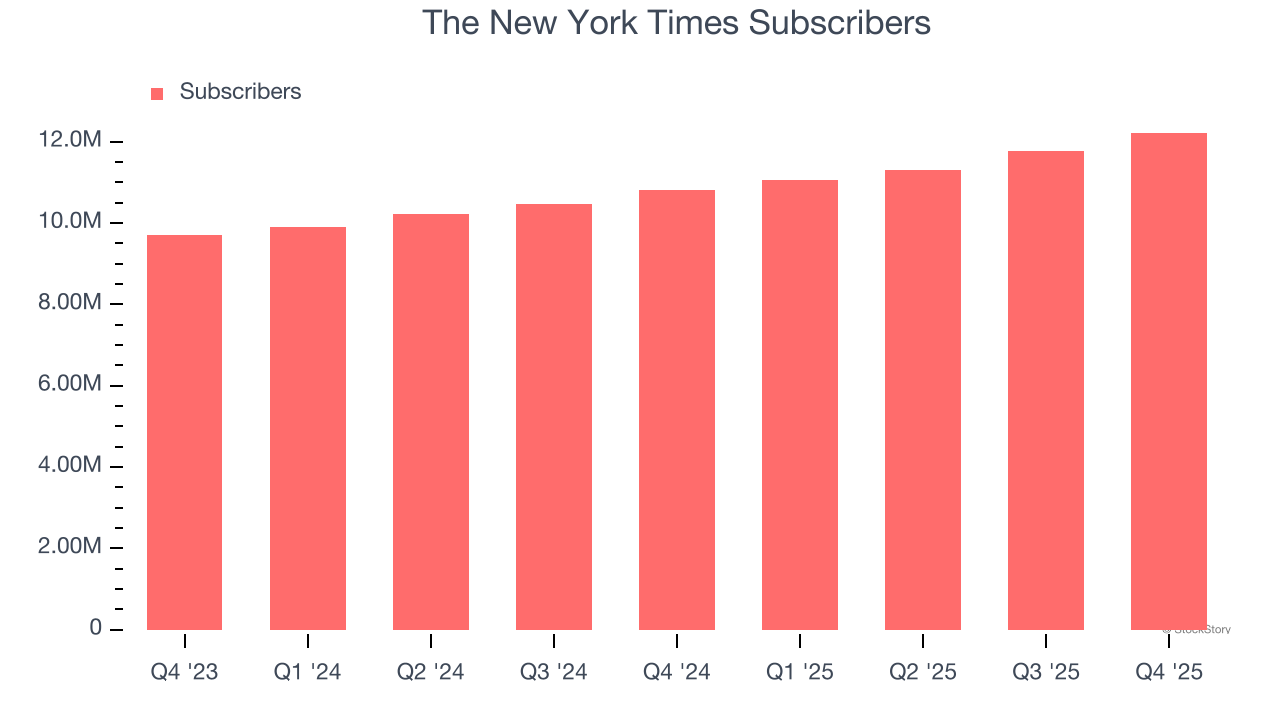

1. Weak Growth in Subscribers Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like The New York Times, our preferred volume metric is subscribers). While both are important, the latter is the most critical to analyze because prices have a ceiling.

The New York Times’s subscribers came in at 12.21 million in the latest quarter, and over the last two years, averaged 11.8% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

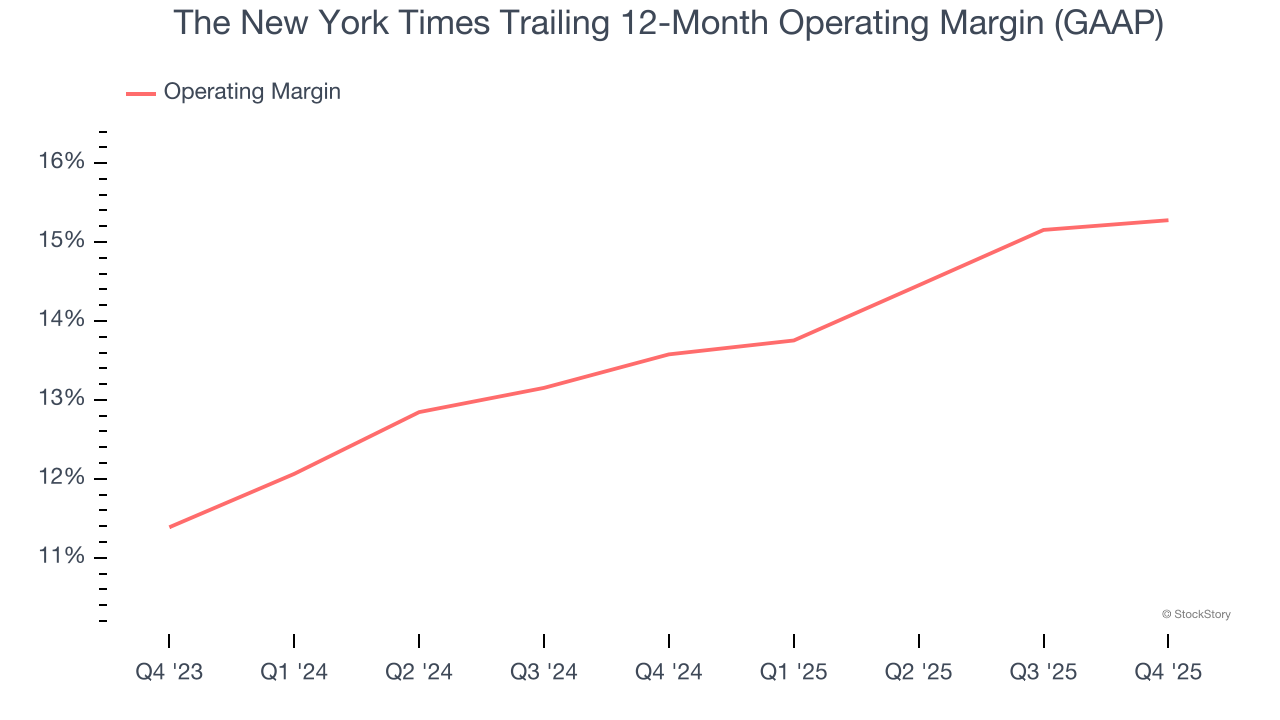

2. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

The New York Times’s operating margin has risen over the last 12 months and averaged 14.5% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

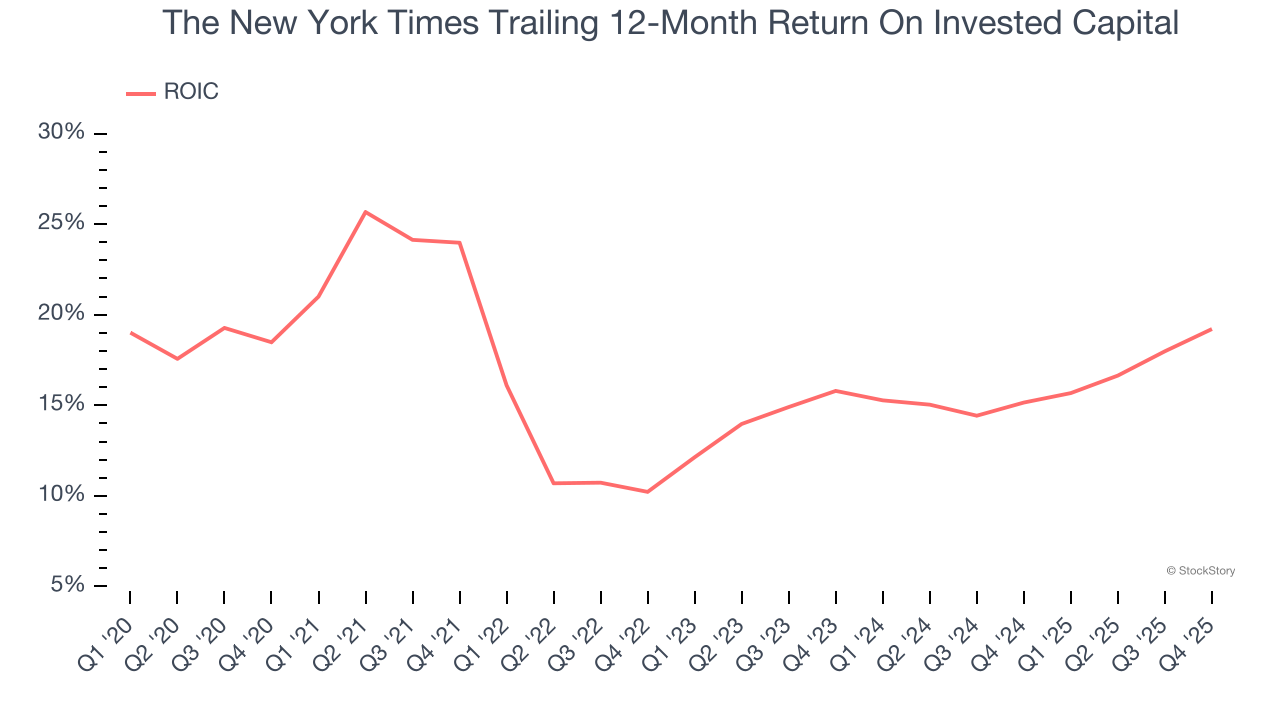

3. New Investments Aren’t Moving the Needle

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, The New York Times’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of The New York Times, we’ll be cheering from the sidelines. After the recent surge, the stock trades at 30.5× forward P/E (or $85.39 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of The New York Times

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.