Over the past six months, Centene’s shares (currently trading at $60.25) have posted a disappointing 18.2% loss while the S&P 500 was flat. This may have investors wondering how to approach the situation.

Following the pullback, is now an opportune time to buy CNC? Find out in our full research report, it’s free.

Why Does CNC Stock Spark Debate?

Serving nearly 1 in 15 Americans through its government healthcare programs, Centene (NYSE: CNC) is a healthcare company that manages government-sponsored health insurance programs like Medicaid and Medicare for low-income and complex-needs populations.

Two Positive Attributes:

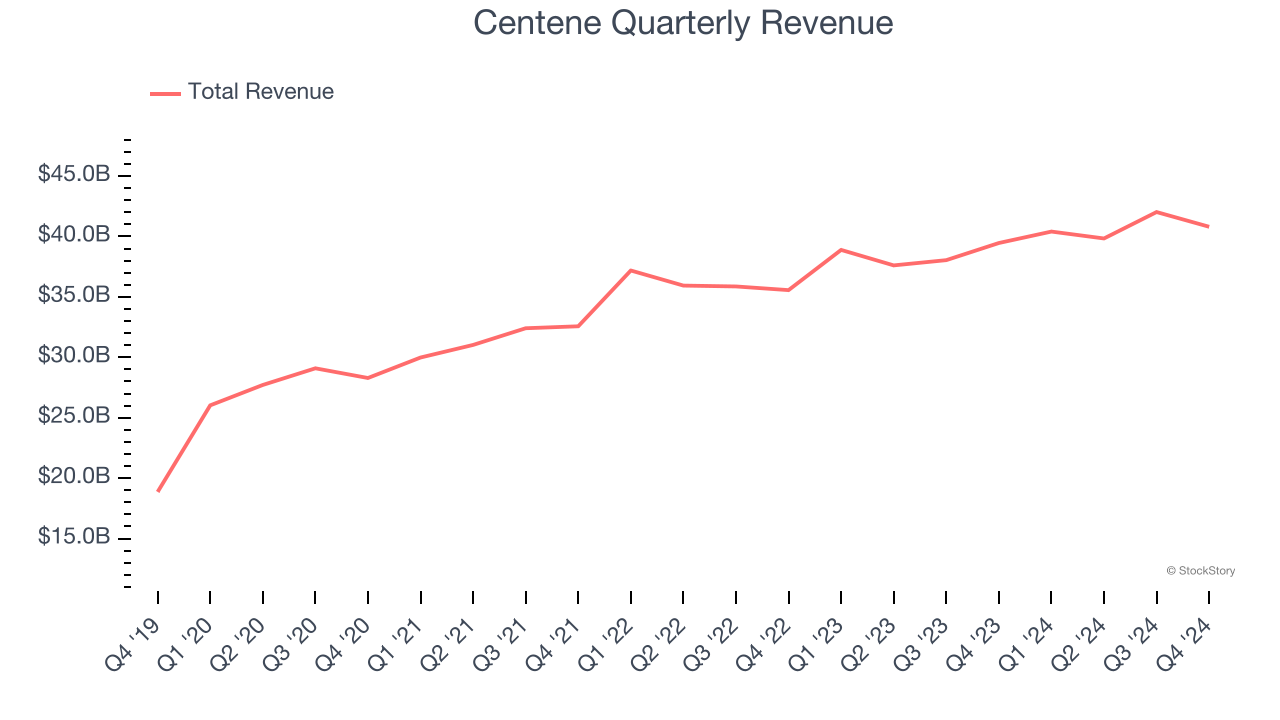

1. Skyrocketing Revenue Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Centene’s sales grew at an impressive 16.9% compounded annual growth rate over the last five years. Its growth surpassed the average healthcare company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $163.1 billion in revenue over the past 12 months, Centene is one of the most scaled enterprises in healthcare. This is particularly important because health insurance providers companies are volume-driven businesses due to their low margins.

One Reason to be Careful:

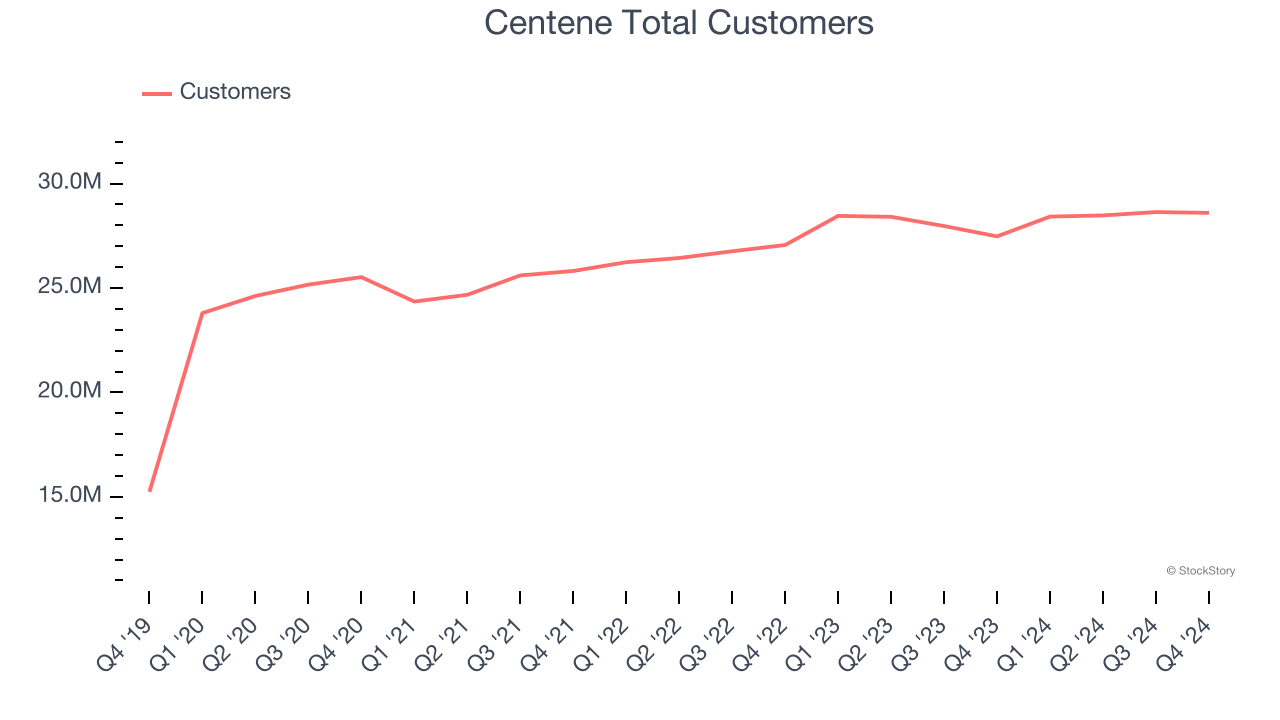

Weak Customer Growth Points to Soft Demand

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

Centene’s total customers came in at 28.6 million in the latest quarter, and over the last two years, their count averaged 3.6% year-on-year growth. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in landing new contracts.

Final Judgment

Centene has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 8.5× forward price-to-earnings (or $60.25 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Centene

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.