As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the reinsurance industry, including AXIS Capital (NYSE: AXS) and its peers.

This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. The primary headwind remains the immense and concentrated exposure to large-scale catastrophe losses, as the growing impact of climate change challenges traditional risk models and creates significant earnings volatility. Additionally, they face the risk of adverse prior-year reserve development, where claims prove more costly than anticipated, while the eventual influx of new capital from alternative sources threatens to soften the market and compress future returns.

The 6 reinsurance stocks we track reported a strong Q1. As a group, revenues missed analysts’ consensus estimates by 1.4%.

Thankfully, share prices of the companies have been resilient as they are up 9.8% on average since the latest earnings results.

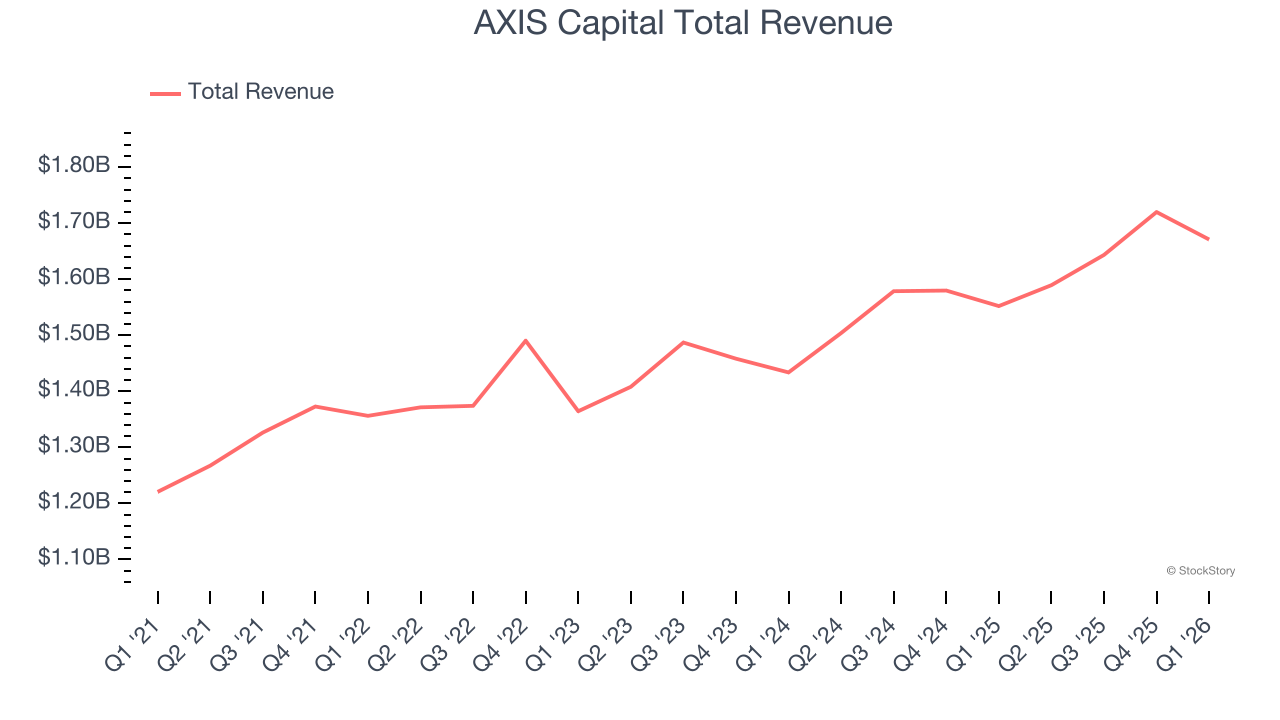

AXIS Capital (NYSE: AXS)

Founded in the aftermath of the 9/11 attacks when insurance capacity was scarce, AXIS Capital Holdings Limited (NYSE: AXS) is a global specialty insurer and reinsurer that provides coverage for complex risks across property, liability, professional lines, cyber, and other specialty markets.

AXIS Capital reported revenues of $1.67 billion, up 7.7% year on year. This print fell short of analysts’ expectations by 3.1%. Overall, it was a softer quarter for the company with a miss of analysts’ net premiums earned and book value per share estimates.

Interestingly, the stock is up 15.4% since reporting and currently trades at $113.09.

Read our full report on AXIS Capital here, it’s free.

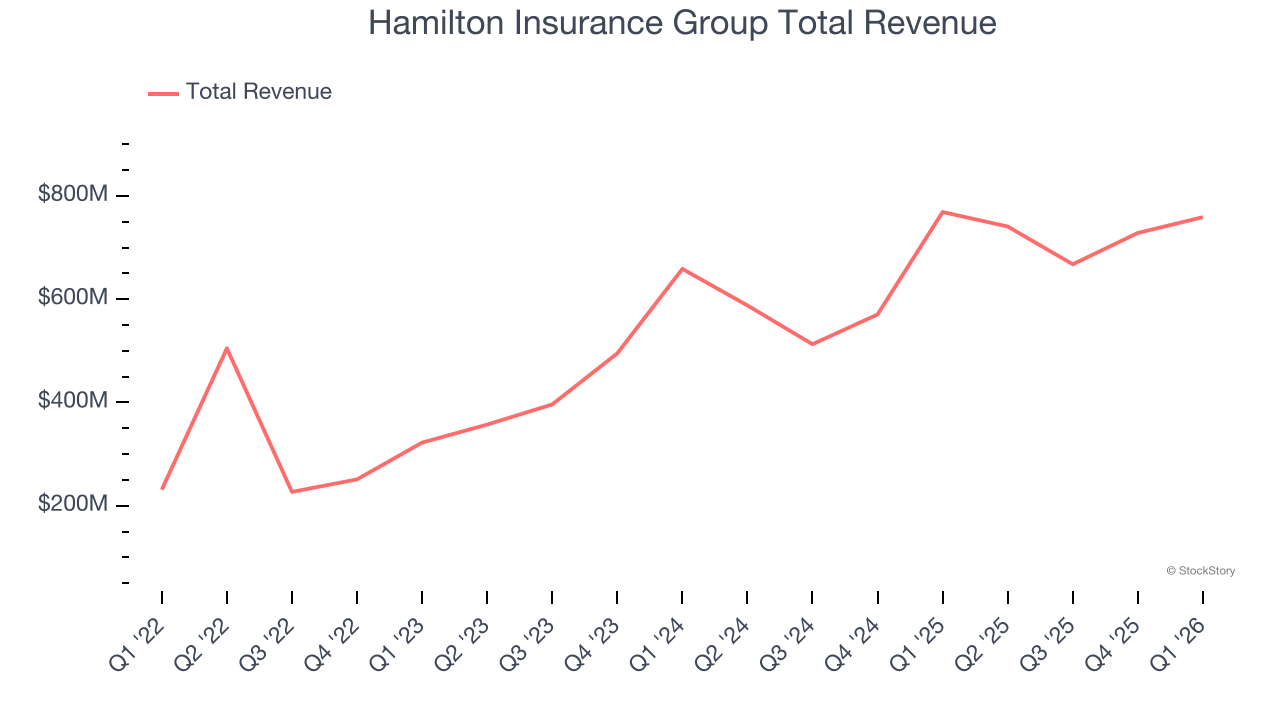

Best Q1: Hamilton Insurance Group (NYSE: HG)

Founded in 2013 and operating through three distinct underwriting platforms across four countries, Hamilton Insurance Group (NYSE: HG) operates global specialty insurance and reinsurance platforms across Lloyd's, Ireland, Bermuda, and the United States.

Hamilton Insurance Group reported revenues of $758.9 million, down 1.3% year on year, outperforming analysts’ expectations by 14.1%. The business had an incredible quarter with a beat of analysts’ EPS estimates.

Hamilton Insurance Group delivered the biggest analyst estimate beat among its peers. The market seems content with the results as the stock is up 3.8% since reporting. It currently trades at $34.00.

Is now the time to buy Hamilton Insurance Group? Access our full analysis of the earnings results here, it’s free.

Everest Group (NYSE: EG)

Rebranded from Everest Re in 2023 to reflect its evolution beyond just reinsurance, Everest Group (NYSE: EG) underwrites property and casualty reinsurance and insurance worldwide, serving insurance companies, corporations, and other clients across six continents.

Everest Group reported revenues of $4.07 billion, down 4.6% year on year, falling short of analysts’ expectations by 5.5%. It was a slower quarter as it posted a significant miss of analysts’ net premiums earned and book value per share estimates.

Interestingly, the stock is up 8.4% since the results and currently trades at $372.96.

Read our full analysis of Everest Group’s results here.

Pelagos Insurance (NYSE: PLGO)

Founded in Bermuda in 2014 and designed to adapt nimbly to evolving market conditions, Pelagos Insurance (NYSE: PLGO) is a global specialty insurance and reinsurance company focused on creating value through strategic capital allocation, expert risk selection and a network of long-term underwriting partnerships.

Pelagos Insurance reported revenues of $610.6 million, down 7.3% year on year. This print topped analysts’ expectations by 4.7%. Overall, it was a stunning quarter as it also logged a beat of analysts’ EPS and net premiums earned estimates.

The stock is up 21.6% since reporting and currently trades at $24.62.

Read our full, actionable report on Pelagos Insurance here, it’s free.

RenaissanceRe (NYSE: RNR)

Born in Bermuda after the devastating Hurricane Andrew created a crisis in the catastrophe insurance market, RenaissanceRe (NYSE: RNR) provides property, casualty, and specialty reinsurance and insurance solutions to customers worldwide, primarily through intermediaries.

RenaissanceRe reported revenues of $2.19 billion, down 36.8% year on year. This result lagged analysts’ expectations by 21.4%. Aside from that, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but a significant miss of analysts’ net premiums earned estimates.

RenaissanceRe had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is up 4.1% since reporting and currently trades at $323.42.

Read our full, actionable report on RenaissanceRe here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.