Occidental Petroleum’s 35% return over the past six months has outpaced the S&P 500 by 28.6%, and its stock price has climbed to $55.44 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Following the strength, is OXY a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Do Investors Watch Occidental Petroleum?

Backed by Warren Buffett's Berkshire Hathaway as a major shareholder, Occidental Petroleum (NYSE: OXY) explores for, develops, and produces oil, natural gas liquids, and natural gas, primarily in the United States and Middle East.

Three Positive Attributes:

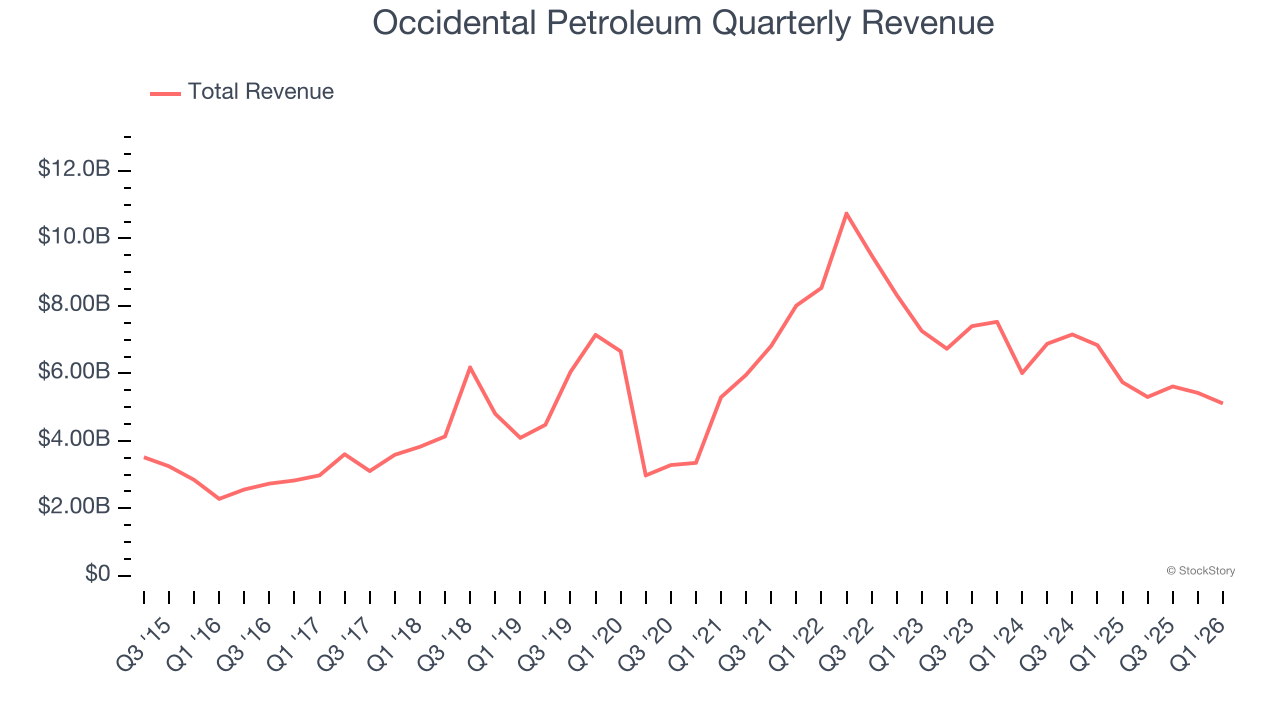

1. Long-Term Revenue Growth Disappoints

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Over the last five years, Occidental Petroleum grew its sales at a tepid 7.6% compounded annual growth rate. This wasn’t a great result compared to the rest of the energy upstream and integrated energy sector, but there are still things to like about Occidental Petroleum.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Occidental Petroleum’s $21.45 billion of revenue in the last year is top-tier for the industry, suggesting the type of diversification that reduces operational risk.

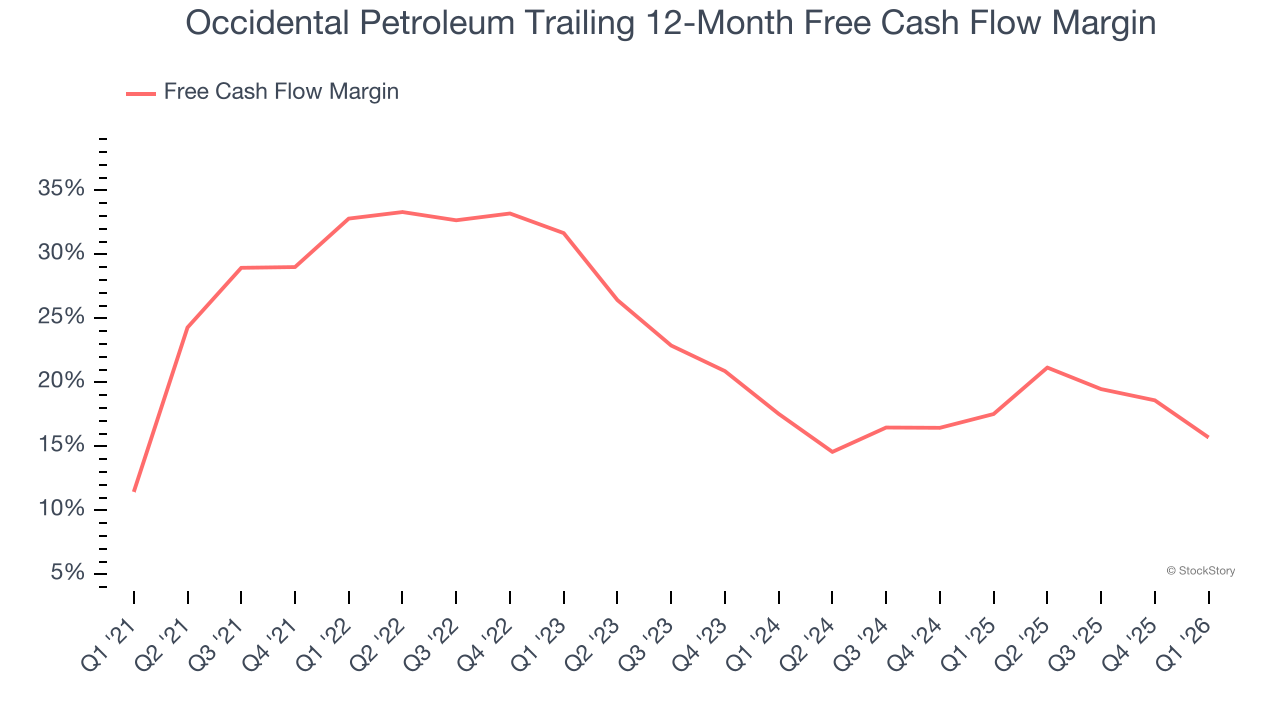

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Occidental Petroleum has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 24% over the last five years.

Final Judgment

Occidental Petroleum is an interesting business with potential, and with its shares outperforming the market lately, the stock trades at 9.7× forward P/E (or $55.44 per share). Is now the right time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Occidental Petroleum

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.