Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Kulicke and Soffa (NASDAQ: KLIC) and the best and worst performers in the semiconductor manufacturing industry.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a very strong Q3. As a group, revenues beat analysts’ consensus estimates by 3.3% while next quarter’s revenue guidance was in line.

Luckily, semiconductor manufacturing stocks have performed well with share prices up 36.6% on average since the latest earnings results.

Kulicke and Soffa (NASDAQ: KLIC)

Headquartered in Singapore, Kulicke & Soffa (NASDAQ: KLIC) is a provider of production equipment and tools used to assemble semiconductor devices

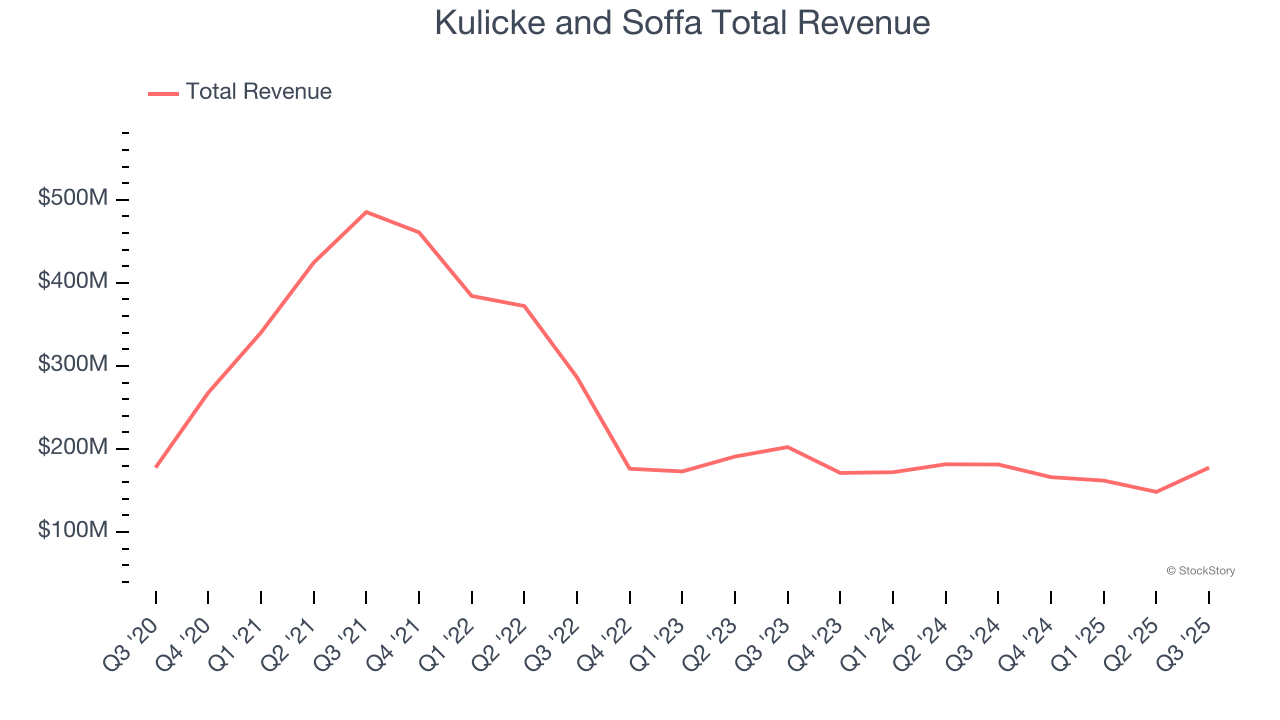

Kulicke and Soffa reported revenues of $177.6 million, down 2.1% year on year. This print exceeded analysts’ expectations by 4.4%. Overall, it was an exceptional quarter for the company with a significant improvement in its inventory levels and a beat of analysts’ EPS estimates.

Lester Wong, Kulicke & Soffa's Interim Chief Executive Officer and Chief Financial Officer, stated, "We continue to focus on multiple technology engagements and are increasingly encouraged by improving end market dynamics and order activity. Our global operations and supply chain teams are preparing for increased customer demand over the coming quarters."

Interestingly, the stock is up 62.8% since reporting and currently trades at $57.46.

Is now the time to buy Kulicke and Soffa? Access our full analysis of the earnings results here, it’s free.

Best Q3: Teradyne (NASDAQ: TER)

Sporting most major chip manufacturers as its customers, Teradyne (NASDAQ: TER) is a US-based supplier of automated test equipment for semiconductors as well as other technologies and devices.

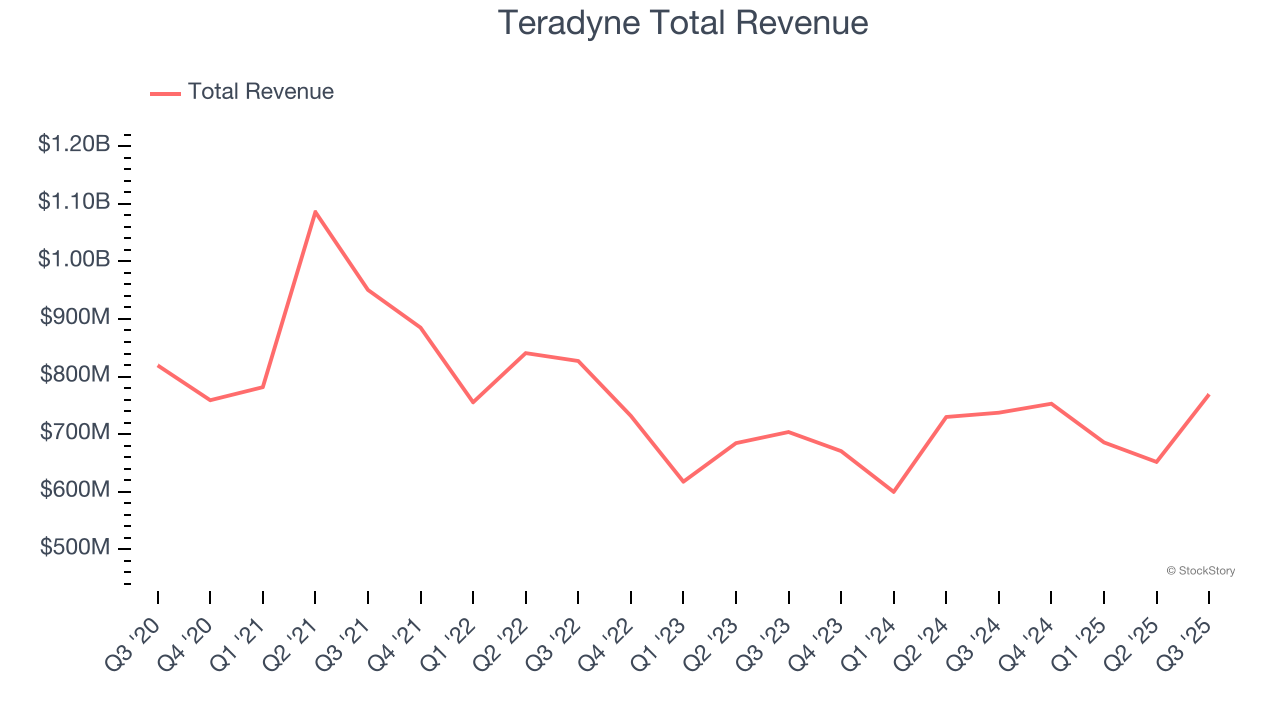

Teradyne reported revenues of $769.2 million, up 4.3% year on year, outperforming analysts’ expectations by 3.3%. The business had a stunning quarter with an impressive beat of analysts’ adjusted operating income estimates and revenue guidance for next quarter exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 58.2% since reporting. It currently trades at $228.40.

Is now the time to buy Teradyne? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Entegris (NASDAQ: ENTG)

With fabs representing the company’s largest customer type, Entegris (NASDAQ: ENTG) supplies products that purify, protect, and generally ensure the integrity of raw materials needed for advanced semiconductor manufacturing.

Entegris reported revenues of $807.1 million, flat year on year, exceeding analysts’ expectations by 0.6%. Still, it was a slower quarter as it posted revenue guidance for next quarter missing analysts’ expectations significantly and EPS in line with analysts’ estimates.

Interestingly, the stock is up 24.2% since the results and currently trades at $117.45.

Read our full analysis of Entegris’s results here.

KLA Corporation (NASDAQ: KLAC)

Formed by the 1997 merger of the two leading semiconductor yield management companies, KLA Corporation (NASDAQ: KLAC) is the leading supplier of equipment used to measure and inspect semiconductor chips.

KLA Corporation reported revenues of $3.21 billion, up 13% year on year. This number topped analysts’ expectations by 1.1%. It was a strong quarter as it also recorded a decent beat of analysts’ adjusted operating income and EPS estimates.

The stock is up 26.9% since reporting and currently trades at $1,568.

Read our full, actionable report on KLA Corporation here, it’s free.

Marvell Technology (NASDAQ: MRVL)

Moving away from a low margin storage device management chips in one of the biggest semiconductor business model pivots of the past decade, Marvell Technology (NASDAQ: MRVL) is a fabless designer of special purpose data processing and networking chips used by data centers, communications carriers, enterprises, and autos.

Marvell Technology reported revenues of $2.07 billion, up 36.8% year on year. This result was in line with analysts’ expectations. It was a satisfactory quarter as it also logged a beat of analysts’ EPS estimates.

Marvell Technology pulled off the fastest revenue growth among its peers. The stock is down 13.4% since reporting and currently trades at $80.53.

Read our full, actionable report on Marvell Technology here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.