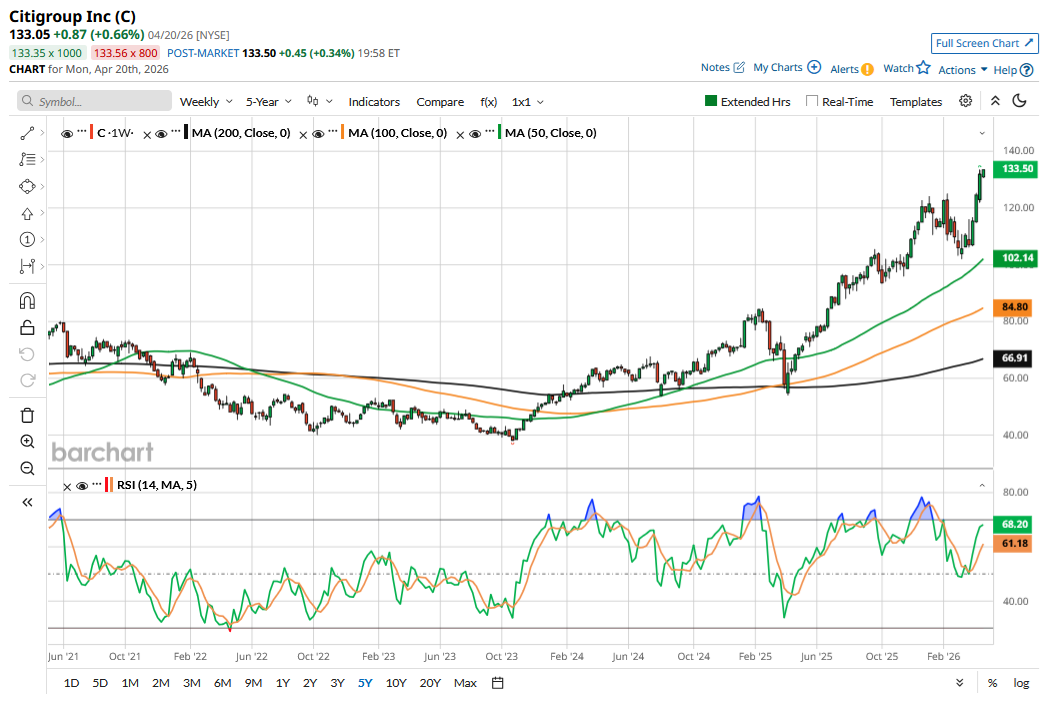

With a year-to-date (YTD) gain of 15%, Citigroup (C) is the best-performing major bank stock this year. The stock’s outperformance is not a 2026 thing; with gains of nearly 66% last year, it outperformed the broader markets and large bank peers by a good margin. The stock is up 87% over the last five years, while the Invesco KBW Bank ETF (KBWB) is up around 33%. Citi’s outperformance over the period could be attributable to the turnaround that CEO Jane Fraser has been leading since she took over the baton in March 2021. While “corporate turnarounds” is a much-abused term, Citi’s turnaround efforts are quite visible in its financials.

Citi Has Been Reporting Stellar Earnings

In Q1 2026, Citi reported revenues of $24.63 billion, which were up 14% year-over-year (YoY) and easily beat the $23.55 billion that analysts expected. Importantly, it was the highest quarterly revenue in a decade and is a testimony to how the turnaround actions are flowing to the income statement.

The performance on the bottom line was equally stellar, with earnings per share (EPS) rising 56% to $3.06, which was well ahead of the $2.65 that analysts expected. Citi’s return on average tangible common equity (RoTCE) was 13.1% in the quarter, which was above the 10%-11% that the company previously projected for the full year.

Notably, as part of the turnaround, Citi has exited several international markets, which has helped free up capital and led to an expansion of RoTCE. It has flattened its organizational structure, reduced bureaucracy, and is working to address the underlying issues that have put it in the crosshairs with regulators in the past. These issues not only put pressure on Citi’s earnings and return ratios but also meant that it traded at a discount to large banks.

Meanwhile, Citi’s turnaround is now nearing completion. As Fraser said in her prepared remarks in the Q1 earnings release, “We’ve entered into the final phase of our divestitures, and 90% of our transformation programs are now at or near our target state.”

The next key trigger for C stock would be the Investor Day that’s set for May 7. At that event, the management is expected to provide long-term plans. These include updates on its artificial intelligence (AI) strategy and how it plans to leverage the technology to cut costs, improve compliance, and offer personalized services to customers. The bank is also expected to provide long-term RoTCE and efficiency goal targets and lay out the vision to grow all five of its business segments organically and sustainably.

Citi should also provide color on its capital allocation strategy during the upcoming Investor Day. Notably, in Q1, it repurchased $6.3 billion worth of shares and overall returned $7.4 billion to shareholders, which represents a payout ratio of 134%.

Should Dividend Investors Buy C Stock?

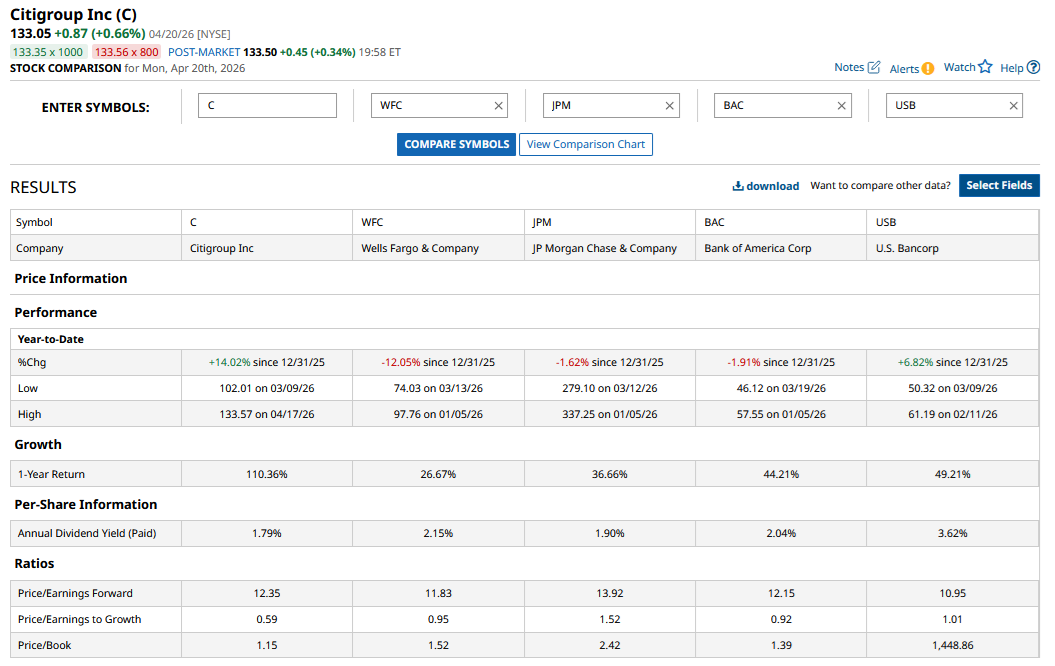

Citi’s dividend yield has now fallen to 1.8%, which is below J.P. Morgan Chase (JPM), Bank of America (BAC), and Wells Fargo (BAC). While Citi’s dividend yield was the highest among the top four U.S. banks by assets, it is now the lowest. However, it is more of a denominator thing, as while Citi has been increasing its dividend, the sharp rise in its stock price has pulled down the dividend yield.

From a valuation perspective, Citi trades at a price-to-book multiple of 1.15, and while it has narrowed the gap with other large banks, the multiple is still the lowest among the top four banks.

I believe there is still scope for Citi to bridge its valuation gap, especially as the company structurally improves its profitability and return metrics. One area where the bank still has some work to do is on the regulatory front. Its Stress Capital Buffer (SCB) is higher compared to peers, as its business is more complex and globally spread out, and it has a large credit card portfolio that warrants higher capital requirements. The bank expects SCB to come down as it progresses in its turnaround and structurally addresses the regulatory issues that have plagued it in the past.

Overall, I believe there is still scope for rerating in Citi, and while it is not as attractive a dividend stock as it was in the past, its total returns after accounting for capital gains should be higher than its average banking peer over the next couple of years.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Keeps Hitting It Out of the Park: Should You Buy?

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?