Oracle (ORCL) is making some uncomfortable moves. The Austin, Texas-based technology giant is reportedly planning to cut thousands of jobs across multiple divisions. At the same time, it has scrapped a planned flagship artificial intelligence data center project in Texas. And it is redirecting that spending toward a broader buildout of cloud infrastructure for clients like OpenAI and Meta (META).

For investors, this raises a fair question: Is Oracle trimming fat to run leaner, or is it a sign that the company is straining under the weight of its AI ambitions?

Oracle’s AI Infrastructure Bet Is Expensive

Oracle ended its fiscal second quarter of 2026 with remaining performance obligations, essentially its backlog of future contracted revenue, of $523.3 billion. That's up 433% from a year earlier. A large portion of that backlog comes from deals signed with Meta, Nvidia (NVDA), and others.

Oracle's cloud infrastructure revenue grew 66% year-over-year (YoY) in the most recent quarter. GPU-related revenue, which powers the AI workloads at the heart of all this demand, grew 177%. Capital expenditures hit $12 billion in just that single quarter.

To put that simply, Oracle is spending money at a staggering pace to build the data centers needed to serve its AI customers. And that's where the tension starts.

According to Simply Wall Street:

- Oracle is reallocating spending away from payroll and at least one large site, the now-cancelled Texas AI data center, toward a broader network of facilities.

- The company is also facing multiple securities class-action lawsuits questioning how its AI strategy was communicated to investors.

- Oracle Principal Financial Officer Doug Kehring told analysts on the December earnings call that Oracle expects full-year fiscal 2026 revenue of $67 billion.

- Notably, the cloud giant expects fiscal 2026 capital expenditures to increase by $15 billion compared to its earlier estimate.

Oracle's free cash flow in the second quarter was a negative $10 billion. The company is funding its buildout through a mix of debt, customer-supplied hardware, and vendor financing arrangements. Oracle Chairman Larry Ellison and other executives stressed on the earnings call that the AI infrastructure behemoth is committed to maintaining its investment-grade debt rating.

The layoffs and cancelled Texas project, as Simply Wall Street reported, look less like a retreat and more like a recalibration.

As Oracle Infrastructure President Clay Magouyrk said on the December call, the company won't accept customer contracts unless "all the necessary ingredients" are in place to deliver them at the right margins.

What's Next for the ORCL Stock Price Target?

On the positive side, Oracle is not just an AI infrastructure play. Its cloud applications business, covering finance, human resources, supply chain, and healthcare systems, is also growing.

Cloud application revenue grew 11% YoY in the most recent quarter.

Healthcare AI agents are now live with 274 customers. Industry cloud applications grew 21%.

The company's own AI data platform, which allows enterprise customers to run AI models on their private data, could be a powerful competitive differentiator against rivals such as Amazon (AMZN), Microsoft (MSFT), and Alphabet (GOOG) (GOOGL).

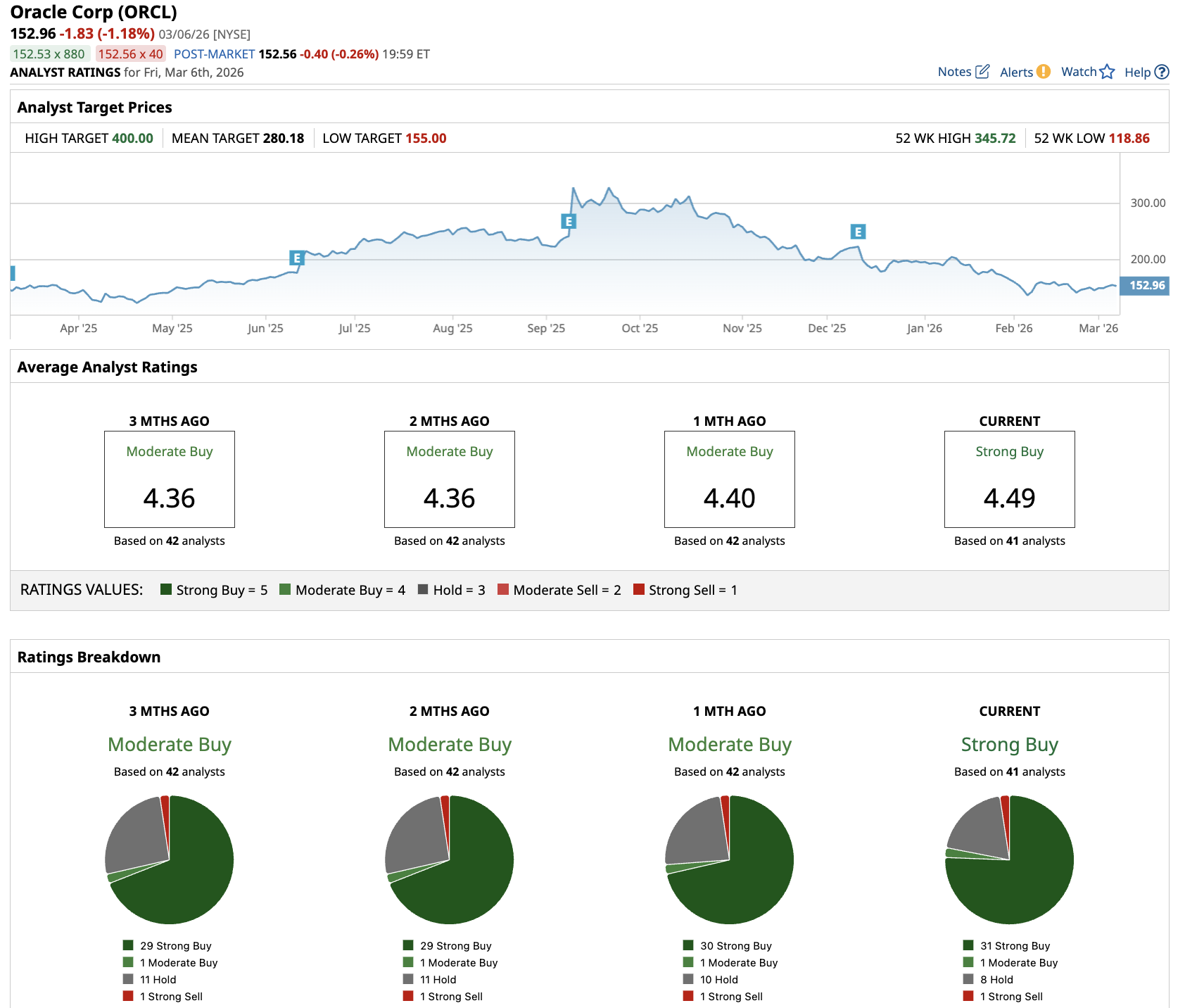

Valued at a market cap of $440 billion, ORCL stock is down 56% from its all-time high. Out of the 41 analysts covering Oracle stock, 31 recommend “Strong Buy,” one recommends “Moderate Buy,” eight recommend “Hold,” and one recommends “Strong Sell.” The average ORCL stock price target is $280.18, indicating an upside potential of almost 100% from current levels.

That said, there are real risks here:

- The securities lawsuits related to AI disclosures are an overhang.

- The sheer scale of capital commitments creates execution risk.

- And Oracle's ability to keep winning large AI infrastructure contracts depends heavily on whether it can deliver data centers on time and at the margins it has promised.

For investors weighing ORCL stock, the core question is this: Can Oracle scale fast enough to convert its $523 billion backlog into real revenue while keeping its balance sheet intact?

The numbers suggest the opportunity is real. The execution risk is equally real.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart