Over the past six months, Franklin BSP Realty Trust’s shares (currently trading at $8.15) have posted a disappointing 19.4% loss, well below the S&P 500’s 8.5% gain. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Franklin BSP Realty Trust, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Franklin BSP Realty Trust Will Underperform?

Despite the more favorable entry price, we’re swiping left on Franklin BSP Realty Trust for now. Here are three reasons why there are better opportunities than FBRT, plus one stock we’d rather own.

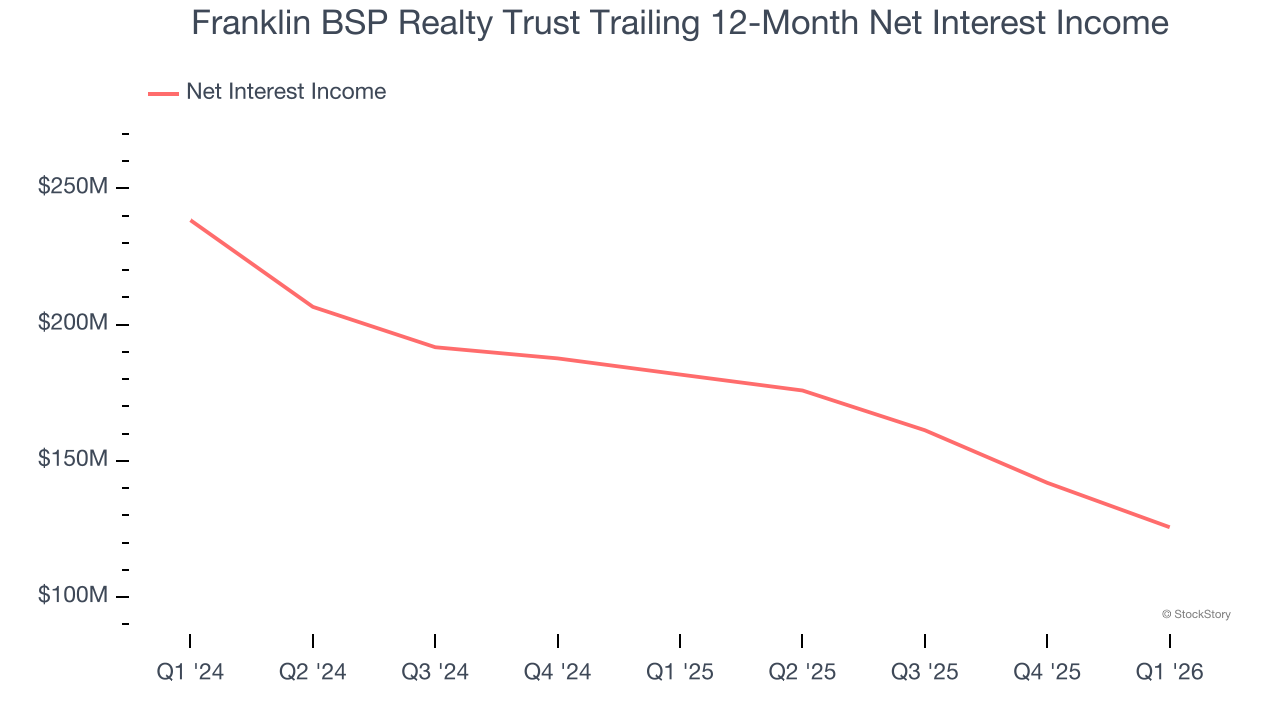

1. Net Interest Income Hits a Plateau

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

Franklin BSP Realty Trust’s net interest income was flat over the last five years, much worse than the broader banking industry. This shows that lending underperformed its other business lines.

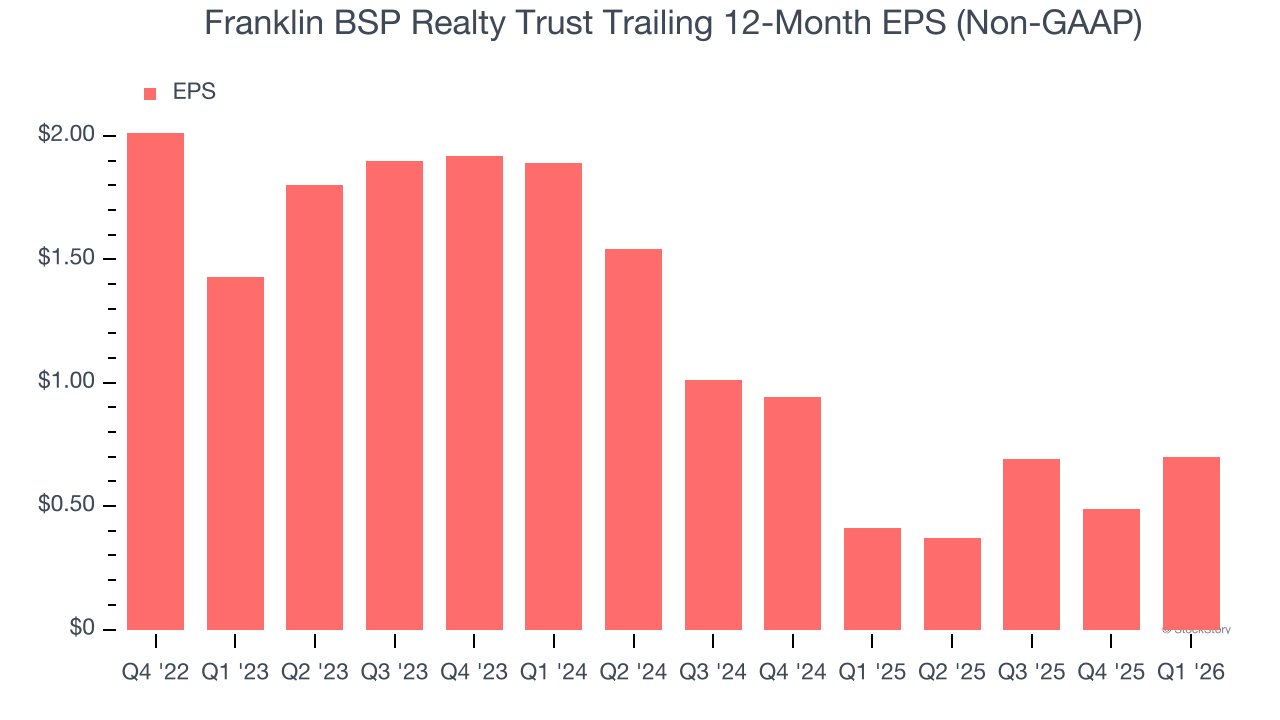

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Franklin BSP Realty Trust’s full-year EPS dropped 24.4%, or 7.5% annually, over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Franklin BSP Realty Trust’s low margin of safety could leave its stock price susceptible to large downswings.

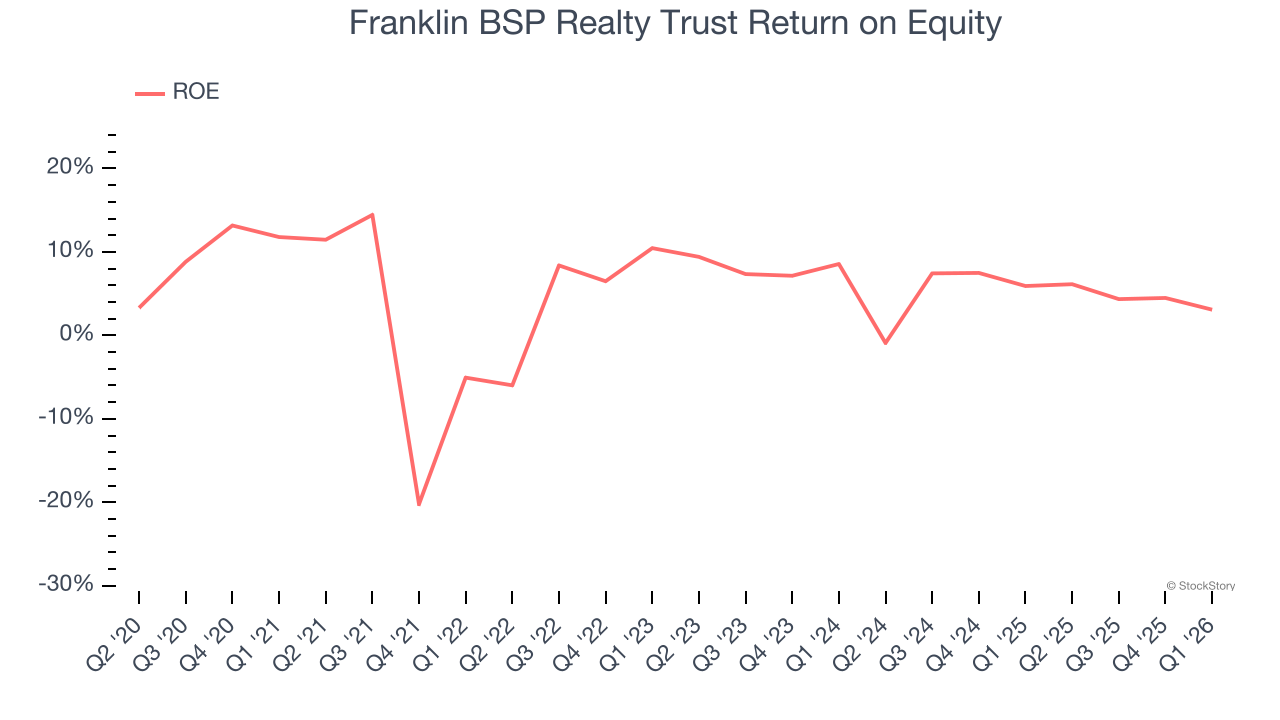

3. Previous Growth Initiatives Haven’t Impressed

Return on equity, or ROE, quantifies bank profitability relative to shareholder equity - an essential capital source for these institutions. Over extended periods, superior ROE performance drives faster shareholder wealth compounding through reinvestment, share repurchases, and dividend growth.

Over the last five years, Franklin BSP Realty Trust has averaged an ROE of 4.5%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

Final Judgment

We see the value of companies driving economic growth, but in the case of Franklin BSP Realty Trust, we’re out. After the recent drawdown, the stock trades at 0.6× forward P/B (or $8.15 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Franklin BSP Realty Trust

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.