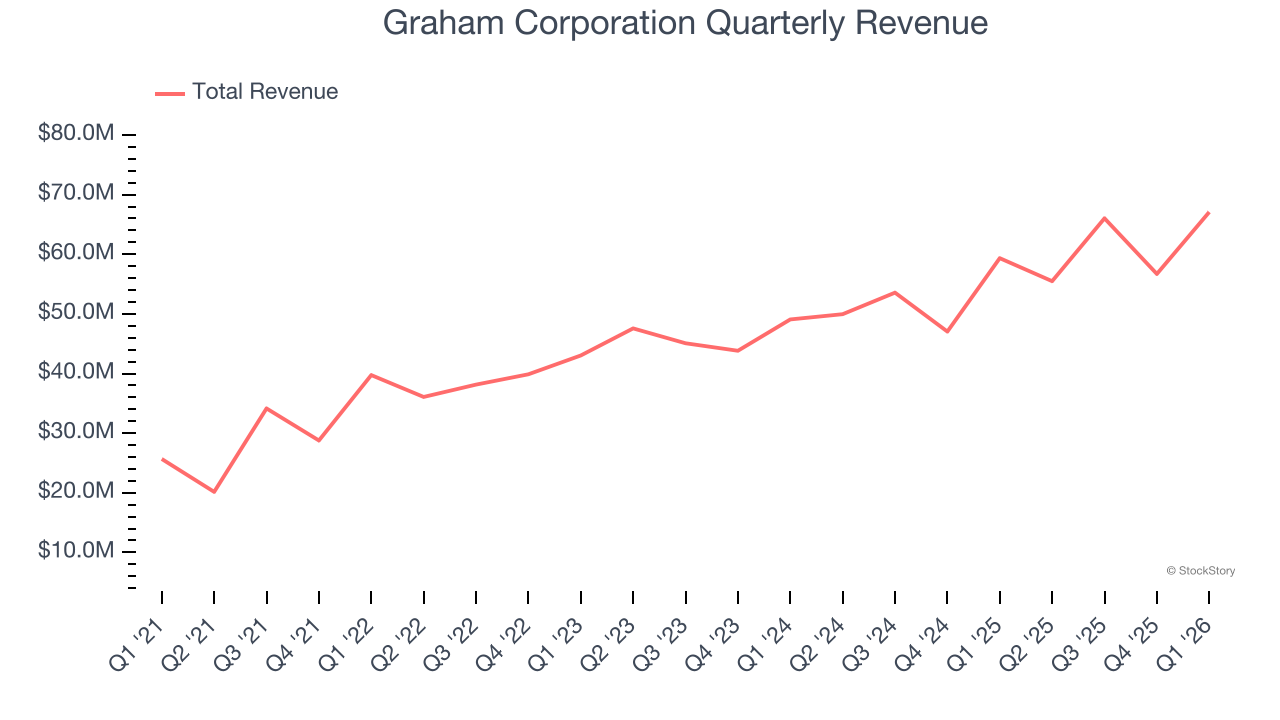

Industrial fluid and energy systems manufacturer Graham Corporation (NYSE: GHM) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 13% year on year to $67.08 million. The company’s full-year revenue guidance of $290 million at the midpoint came in 3% above analysts’ estimates. Its non-GAAP profit of $0.33 per share was 10.9% above analysts’ consensus estimates.

Is now the time to buy Graham Corporation? Find out by accessing our full research report, it’s free.

Graham Corporation (GHM) Q1 CY2026 Highlights:

- Revenue: $67.08 million vs analyst estimates of $59.95 million (13% year-on-year growth, 11.9% beat)

- Adjusted EPS: $0.33 vs analyst estimates of $0.30 (10.9% beat)

- Adjusted EBITDA: $6.82 million vs analyst estimates of $6.56 million (10.2% margin, 3.9% beat)

- EBITDA guidance for the upcoming financial year 2027 is $37.5 million at the midpoint, below analyst estimates of $39.5 million

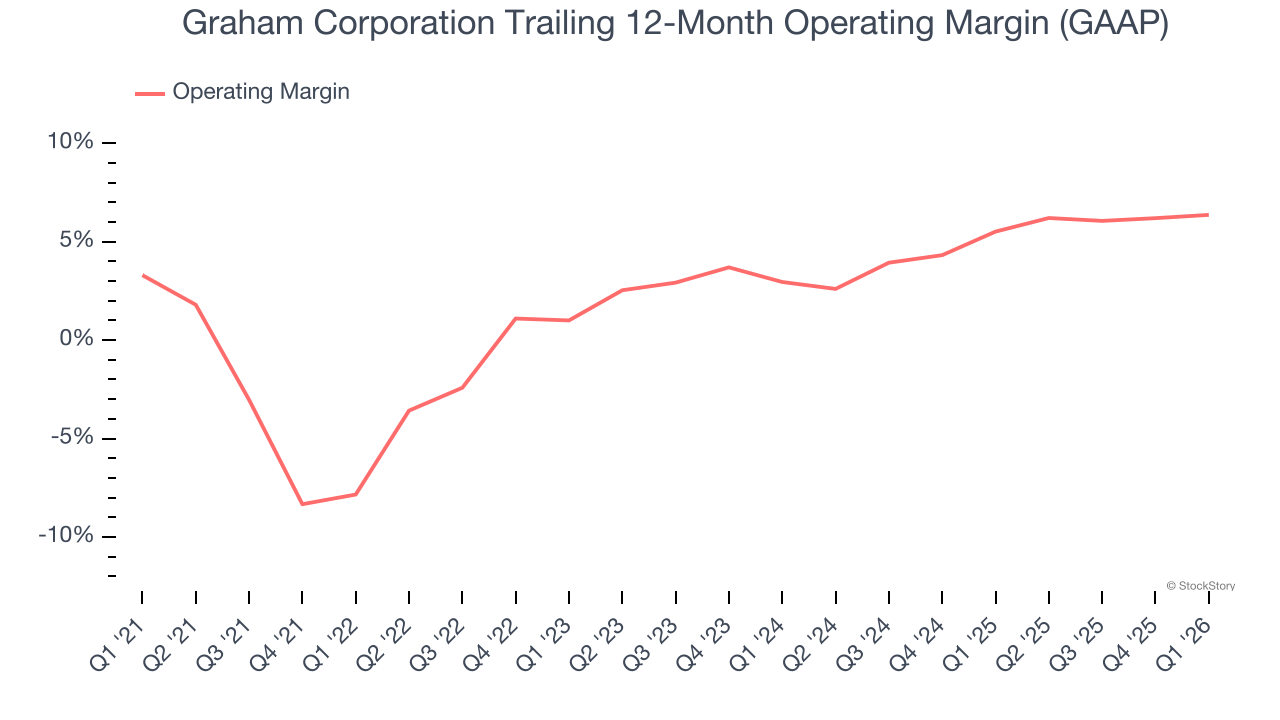

- Operating Margin: 4%, in line with the same quarter last year

- Free Cash Flow was -$2.72 million compared to -$8.71 million in the same quarter last year

- Backlog: $532.6 million at quarter end, up 29.2% year on year

- Market Capitalization: $1.25 billion

Graham’s President and Chief Executive Officer, Matthew J. Malone stated, “Fiscal 2026 was another year of strong execution and continued momentum across Graham. We delivered record annual revenue, orders, and backlog, as well as a 1.5x book-to-bill ratio, reflecting sustained demand across our core end markets and the strength of our diversified business model. During the year, we continued executing on strategic initiatives to drive sustainable long-term value creation including investments focused on capability and capacity expansion, operational excellence, and next generation technology, which are expected to deliver returns on invested capital above 20%.”

Company Overview

Founded when its founder patented a unique design for a vacuum system used in the sugar refining process, Graham (NYSE: GHM) provides vacuum and heat transfer equipment for the energy, petrochemical, refining, and chemical sectors.

Revenue Growth

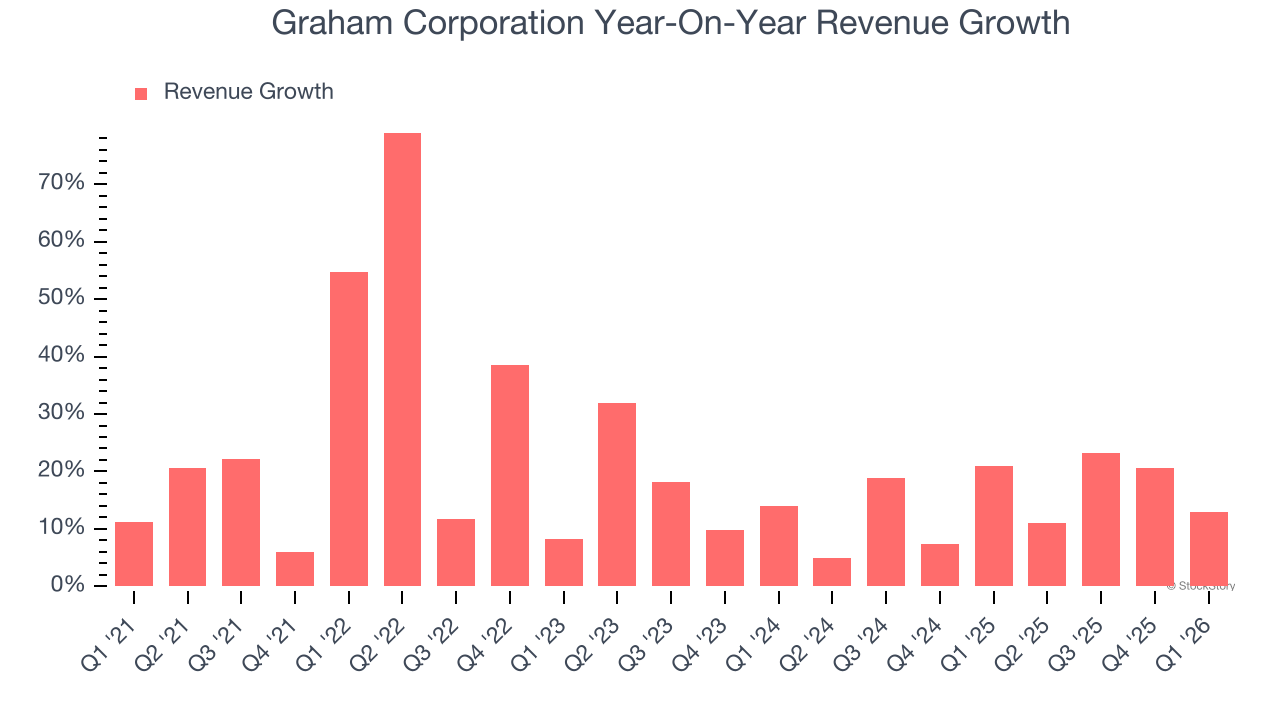

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Graham Corporation’s 20.3% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Graham Corporation’s annualized revenue growth of 15% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Graham Corporation reported year-on-year revenue growth of 13%, and its $67.08 million of revenue exceeded Wall Street’s estimates by 11.9%.

Looking ahead, sell-side analysts expect revenue to grow 16.5% over the next 12 months, similar to its two-year rate. This projection is eye-popping and implies its newer products and services will catalyze better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Graham Corporation was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.7% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Graham Corporation’s operating margin rose by 14.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q1, Graham Corporation generated an operating margin profit margin of 4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

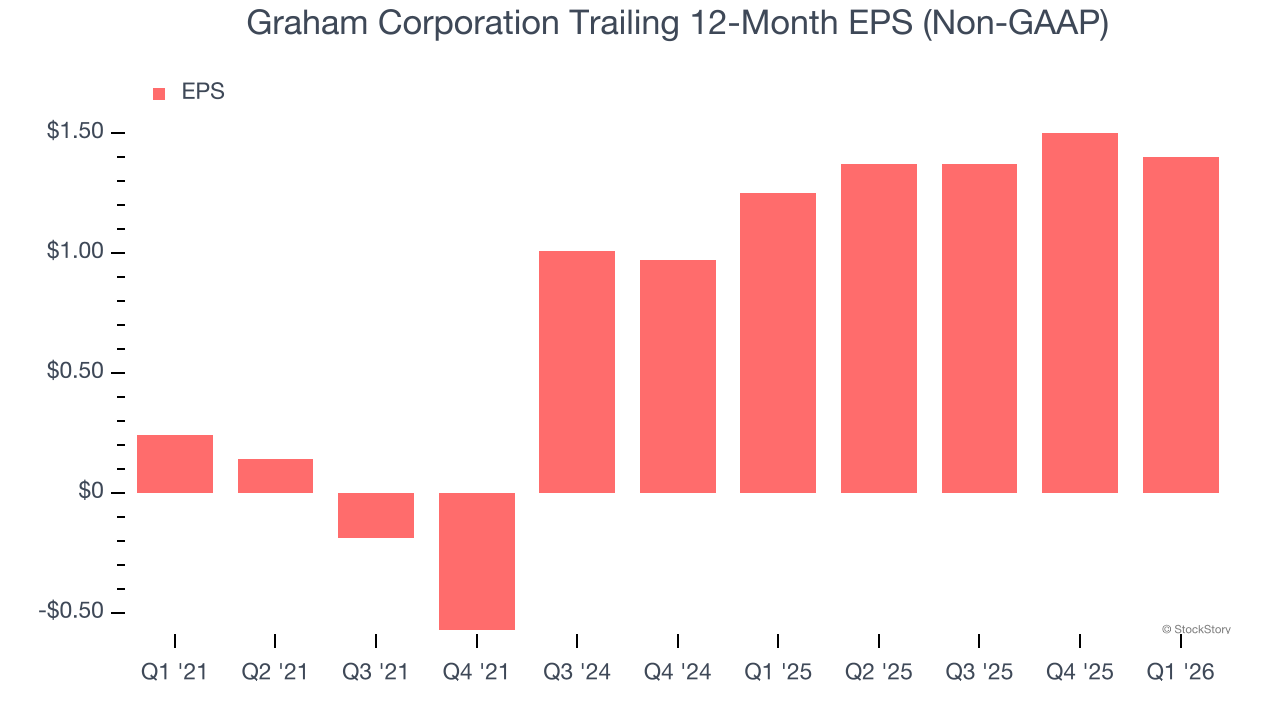

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

Graham Corporation’s EPS grew at 42.3% compounded annual growth rate over the last five years, higher than its 20.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Graham Corporation’s earnings can give us a better understanding of its performance. As we mentioned earlier, Graham Corporation’s operating margin was flat this quarter but expanded by 14.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Graham Corporation, its two-year annual EPS growth of 31.5% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Graham Corporation reported adjusted EPS of $0.33, down from $0.43 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Graham Corporation’s full-year EPS to grow 55% from $1.40 to $2.17.

Key Takeaways from Graham Corporation’s Q1 Results

We were impressed by how significantly Graham Corporation blew past analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Overall, this print was mixed. The market seemed to be hoping for more, and the stock traded down 1.6% to $105.39 immediately after reporting.

Is Graham Corporation an attractive investment opportunity at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).