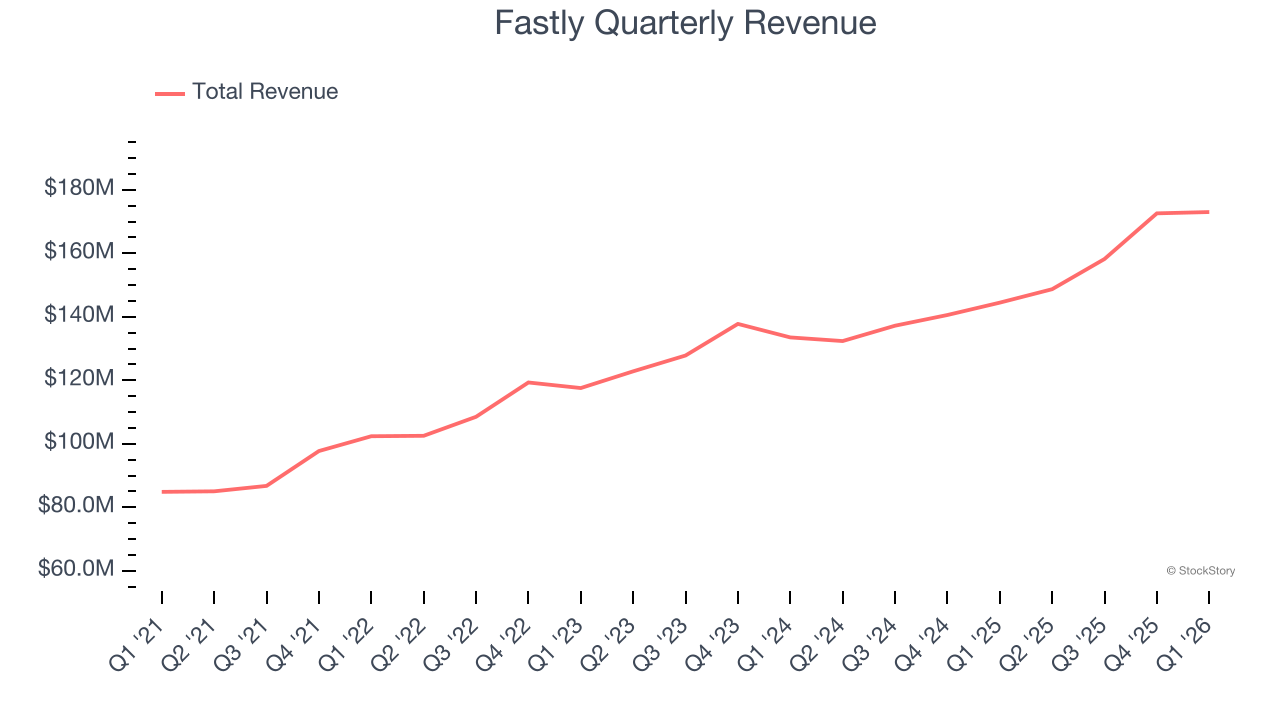

Edge cloud platform Fastly (NASDAQ: FSLY) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 19.8% year on year to $173 million. Guidance for next quarter’s revenue was better than expected at $173 million at the midpoint, 0.6% above analysts’ estimates. Its non-GAAP profit of $0.13 per share was 50.2% above analysts’ consensus estimates.

Is now the time to buy Fastly? Find out by accessing our full research report, it’s free.

Fastly (FSLY) Q1 CY2026 Highlights:

- Revenue: $173 million vs analyst estimates of $172 million (19.8% year-on-year growth, 0.6% beat)

- Adjusted EPS: $0.13 vs analyst estimates of $0.09 (50.2% beat)

- Adjusted Operating Income: $19.14 million vs analyst estimates of $16.33 million (11.1% margin, 17.2% beat)

- The company lifted its revenue guidance for the full year to $717.5 million at the midpoint from $710 million, a 1.1% increase

- Management raised its full-year Adjusted EPS guidance to $0.30 at the midpoint, a 15.4% increase

- Operating Margin: -13.8%, up from -26.4% in the same quarter last year

- Free Cash Flow Margin: 2.4%, down from 5% in the previous quarter

- Market Capitalization: $5.06 billion

Company Overview

Taking its name from the core advantage it delivers to customers, Fastly (NASDAQ: FSLY) operates an edge cloud platform that processes, secures, and delivers web content as close to end users as possible, enabling faster digital experiences.

Revenue Growth

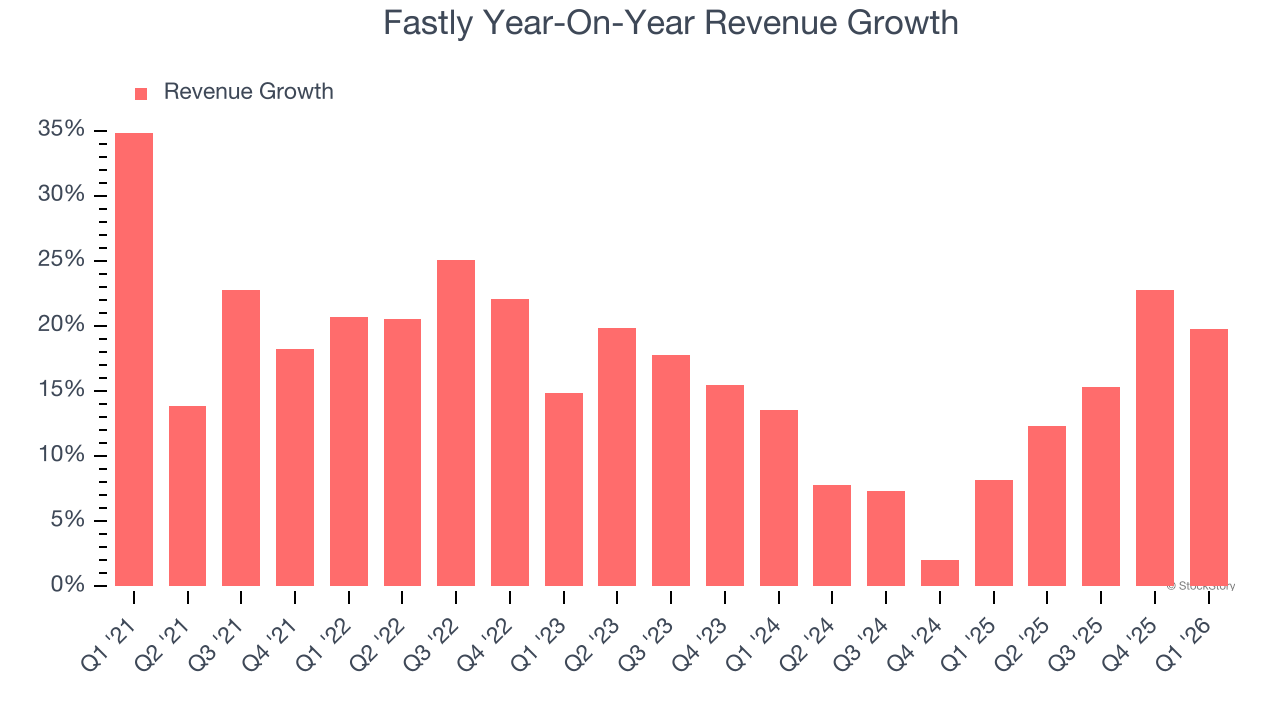

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Fastly grew its sales at a 15.8% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Fastly’s recent performance shows its demand has slowed as its annualized revenue growth of 11.8% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Fastly reported year-on-year revenue growth of 19.8%, and its $173 million of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 16.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and suggests its newer products and services will not catalyze better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

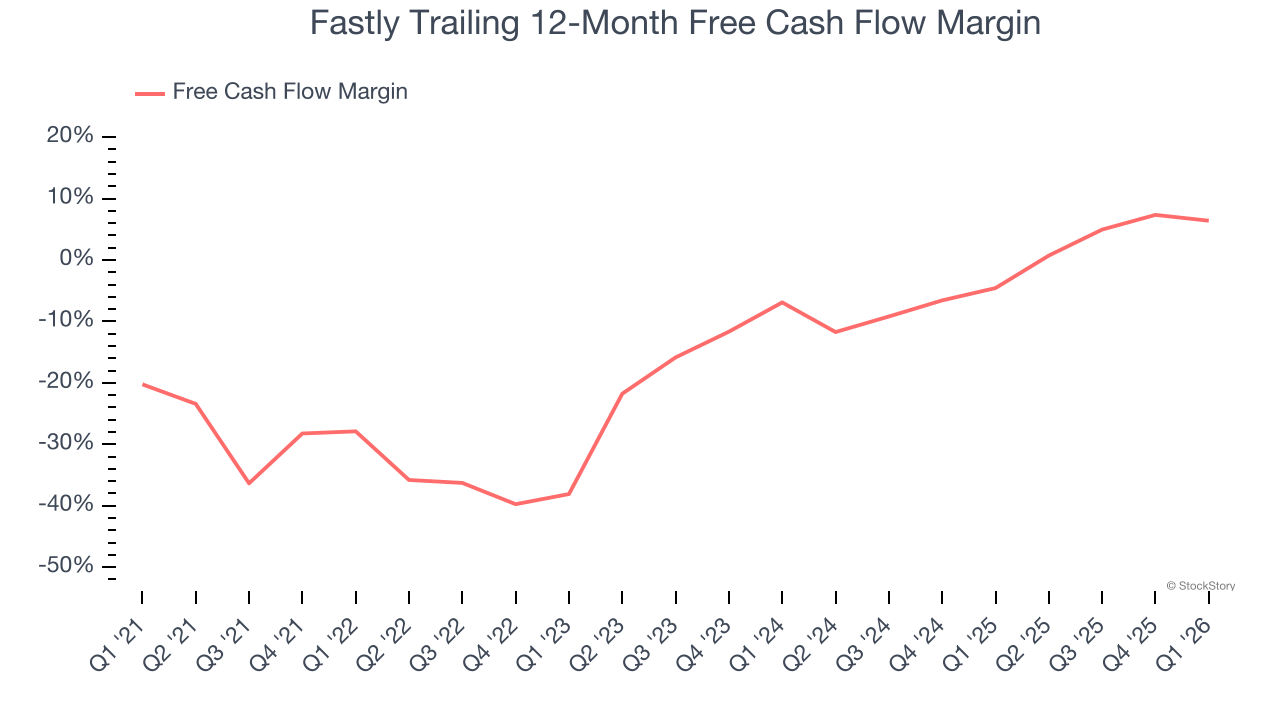

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Fastly has shown weak cash profitability relative to peers over the last year, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 6.4%, below what we’d expect for a software business.

Fastly’s free cash flow clocked in at $4.11 million in Q1, equivalent to a 2.4% margin. The company’s cash profitability regressed as it was 3.3 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts’ consensus estimates show they’re expecting Fastly’s free cash flow margin of 6.4% for the last 12 months to remain the same.

Key Takeaways from Fastly’s Q1 Results

Revenue beat slightly and adjusted operating income beat more convincingly. Guidance was also solid, with next quarter's revenue and EPS guides above Wall Street's expectations. Full-year revenue and EPS guidance also beat. However, with the stock up roughly 270% in the last three months and nearly 450% in the last year on AI hype, it seems these results were not good enough. The market seemed to be hoping for more, and the stock traded down 27.3% to $22.95 immediately following the results.

So do we think Fastly is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).