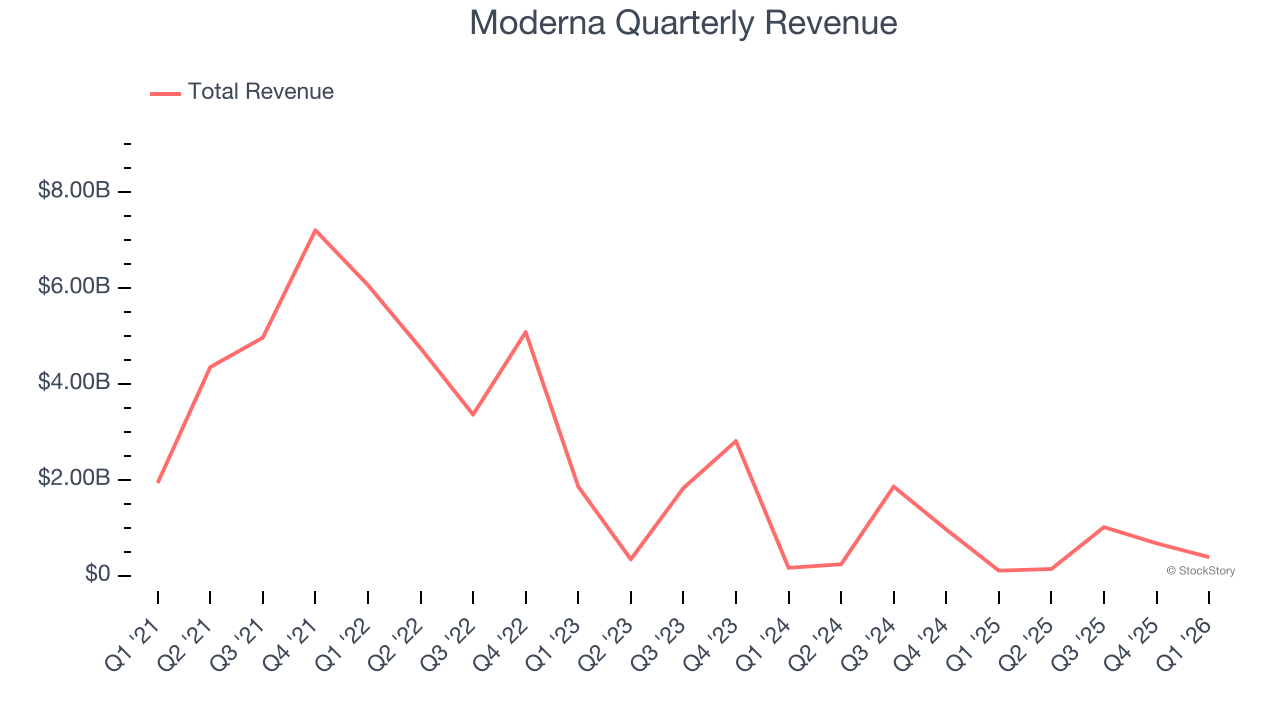

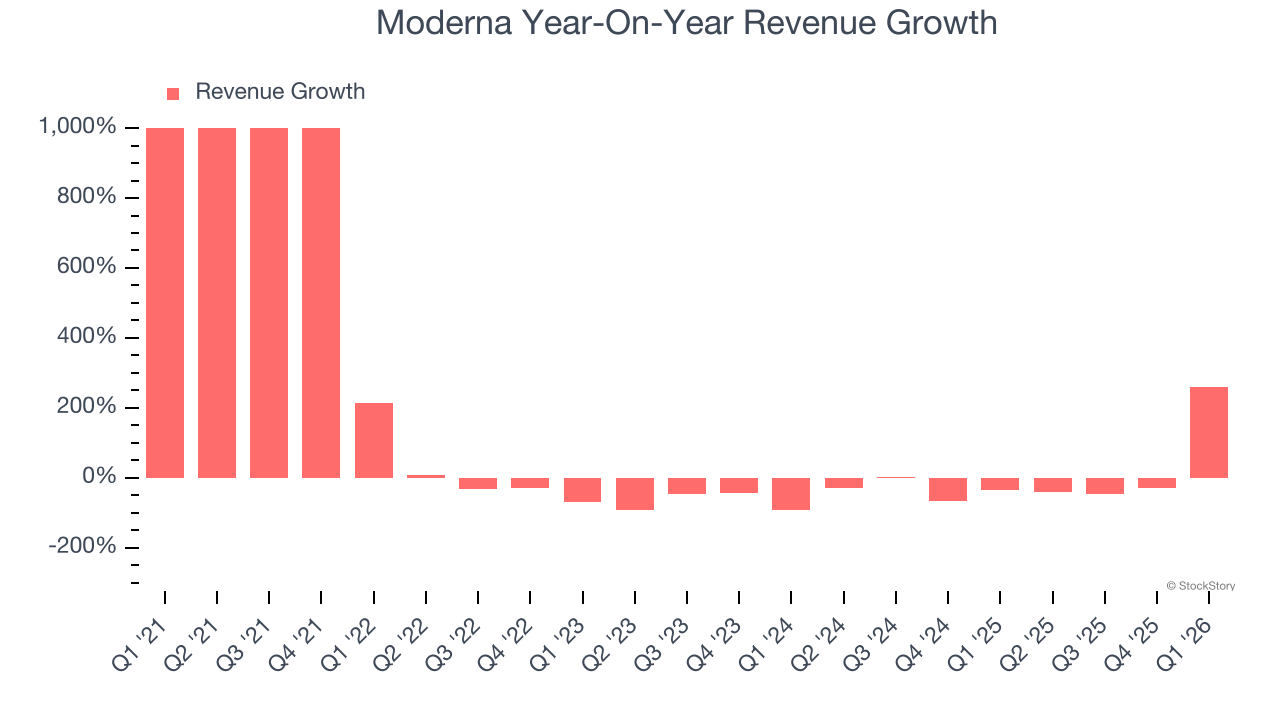

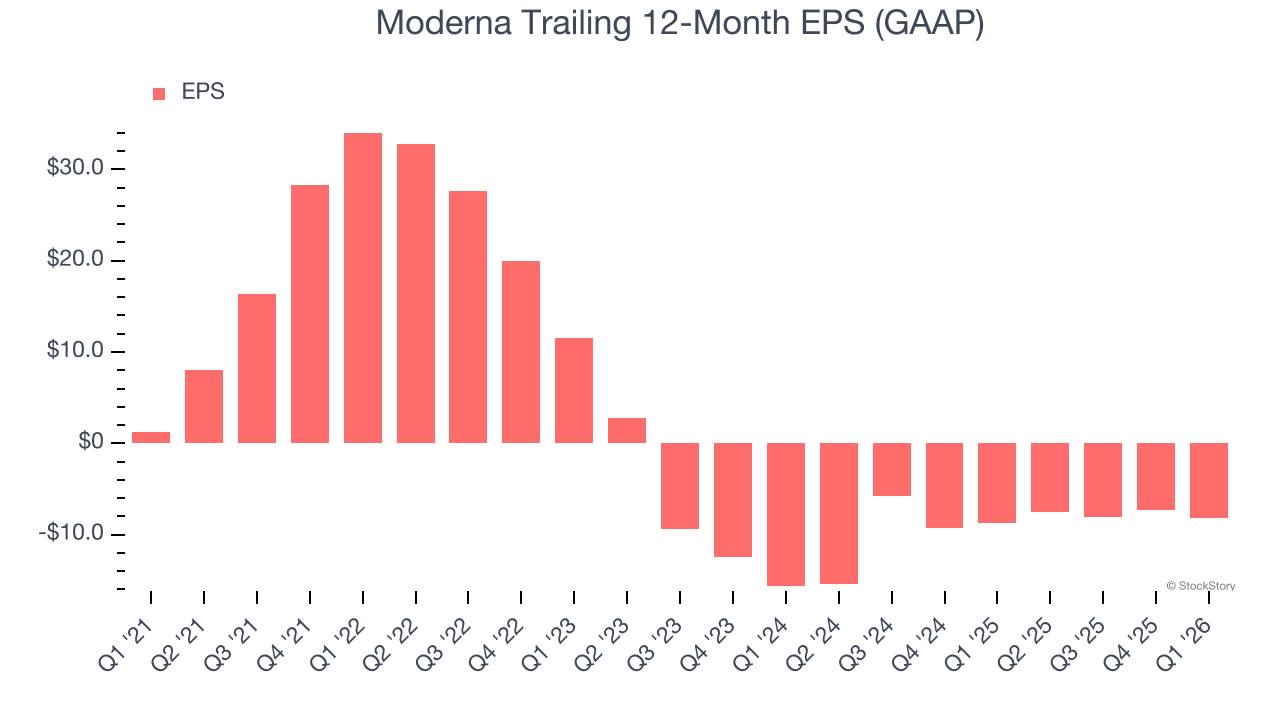

Biotechnology company Moderna (NASDAQ: MRNA) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 260% year on year to $389 million. Its GAAP loss of $3.40 per share was 12.4% above analysts’ consensus estimates.

Is now the time to buy Moderna? Find out by accessing our full research report, it’s free.

Moderna (MRNA) Q1 CY2026 Highlights:

- Revenue: $389 million vs analyst estimates of $249.7 million (260% year-on-year growth, 55.8% beat)

- EPS (GAAP): -$3.40 vs analyst estimates of -$3.88 (12.4% beat)

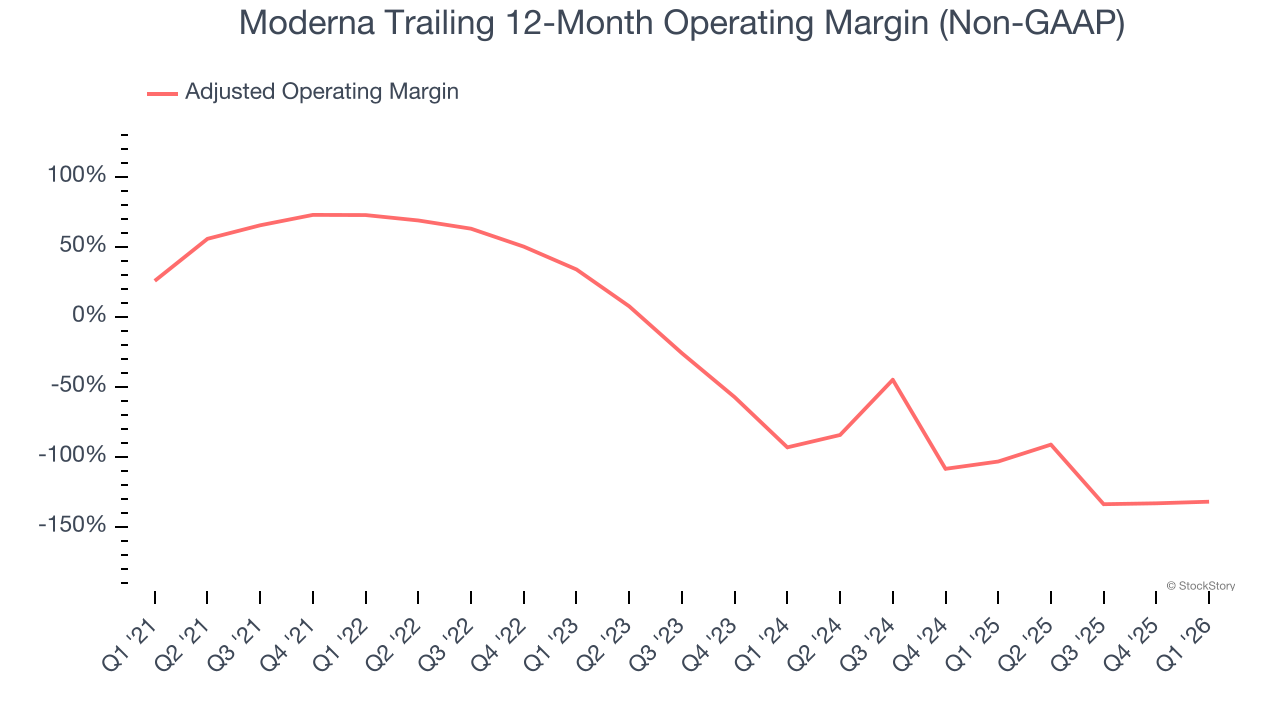

- Adjusted EBITDA: -$1.23 billion (-315% margin, 21.2% year-on-year decline)

- Operating Margin: -357%, up from -972% in the same quarter last year

- Free Cash Flow was -$692 million compared to -$1.15 billion in the same quarter last year

- Market Capitalization: $18.22 billion

"The Moderna team delivered a great start to the year, driving significant revenue growth and substantial cost reductions building on actions taken in 2025. We received two product approvals in Europe, including the world's first flu plus COVID combination vaccine, mCOMBRIAX. We also started a new pivotal trial for intismeran-our first Phase 3 monotherapy study for high-risk Stage 1 non-small cell lung cancer patients," said Stéphane Bancel, Chief Executive Officer of Moderna.

Company Overview

Rising to global prominence during the COVID-19 pandemic with one of the first effective vaccines, Moderna (NASDAQ: MRNA) develops messenger RNA (mRNA) medicines that direct the body's cells to produce proteins with therapeutic or preventive benefits for various diseases.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Moderna struggled to consistently generate demand over the last five years as its sales dropped at a 4% annual rate. This was below our standards and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Moderna’s recent performance shows its demand remained suppressed as its revenue has declined by 34.3% annually over the last two years.

This quarter, Moderna reported magnificent year-on-year revenue growth of 260%, and its $389 million of revenue beat Wall Street’s estimates by 55.8%.

Looking ahead, sell-side analysts expect revenue to decline by 12.1% over the next 12 months. While this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Moderna has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 21.7%.

Analyzing the trend in its profitability, Moderna’s adjusted operating margin decreased significantly over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 38.8 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Moderna generated an adjusted operating margin profit margin of negative 330%, up 535.7 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Moderna, its EPS declined by 53.5% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of Moderna’s earnings can give us a better understanding of its performance. As we mentioned earlier, Moderna’s adjusted operating margin expanded this quarter but declined by 204.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Moderna reported EPS of negative $3.40, down from negative $2.51 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Moderna to improve its earnings losses. Analysts forecast its full-year EPS of negative $8.15 will advance to negative $6.50. This is unusual as its revenue and operating margin are anticipated to fall, signaling the increase likely stems from "below-the-line" items such as taxes.

Key Takeaways from Moderna’s Q1 Results

We were impressed by how significantly Moderna blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 5.5% to $48.70 immediately after reporting.

Indeed, Moderna had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).