Coinbase’s stock price has taken a beating over the past six months, shedding 55% of its value and falling to $174.10 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is this a buying opportunity for COIN? Find out in our full research report, it’s free.

Why Does Coinbase Spark Debate?

Widely regarded as the face of crypto, Coinbase (NASDAQ: COIN) is a blockchain infrastructure company updating the financial system with its trading, staking, stablecoin, and other payment solutions.

Two Things to Like:

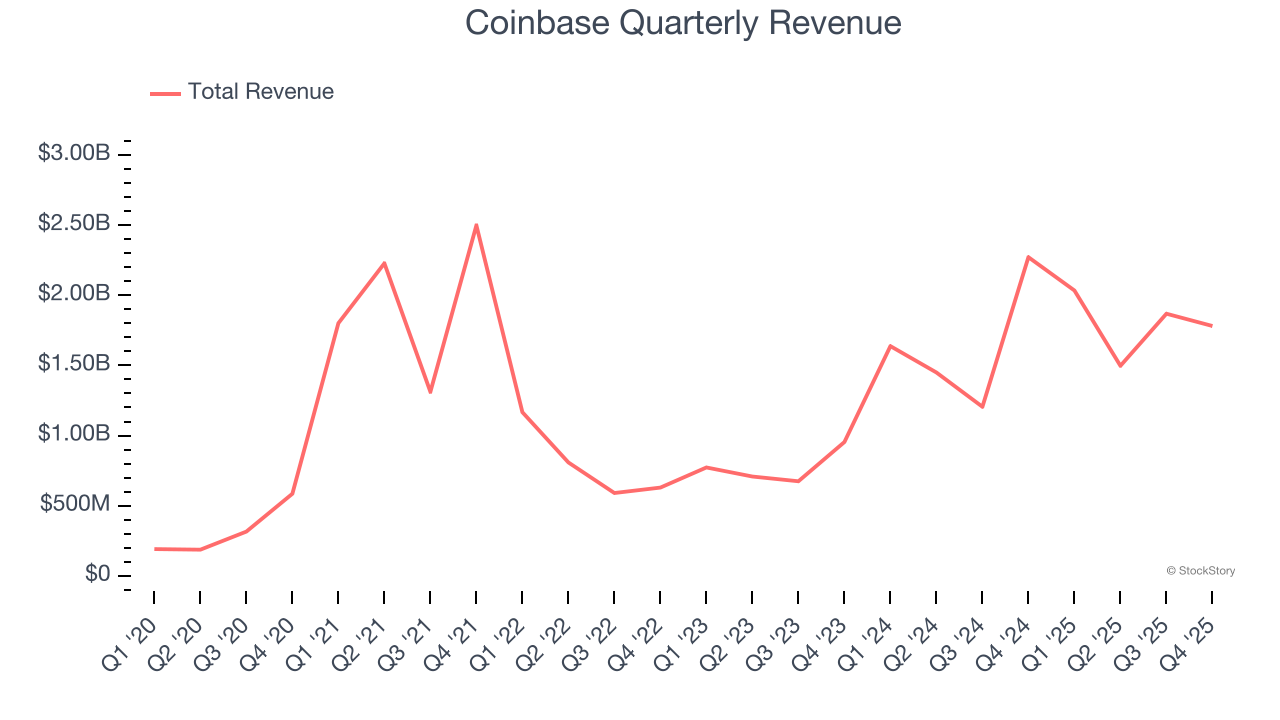

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Coinbase’s sales grew at an incredible 41.2% compounded annual growth rate over the last five years. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

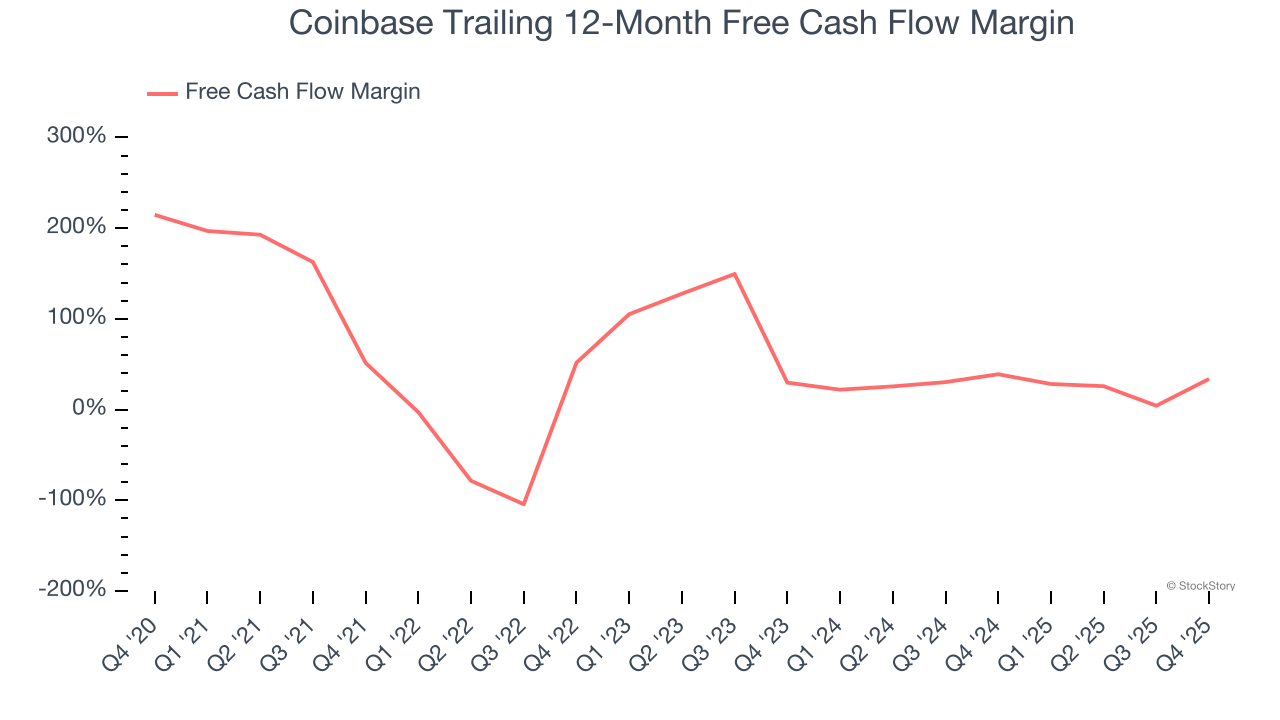

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Coinbase has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 36.3% over the last two years.

One Reason to be Careful:

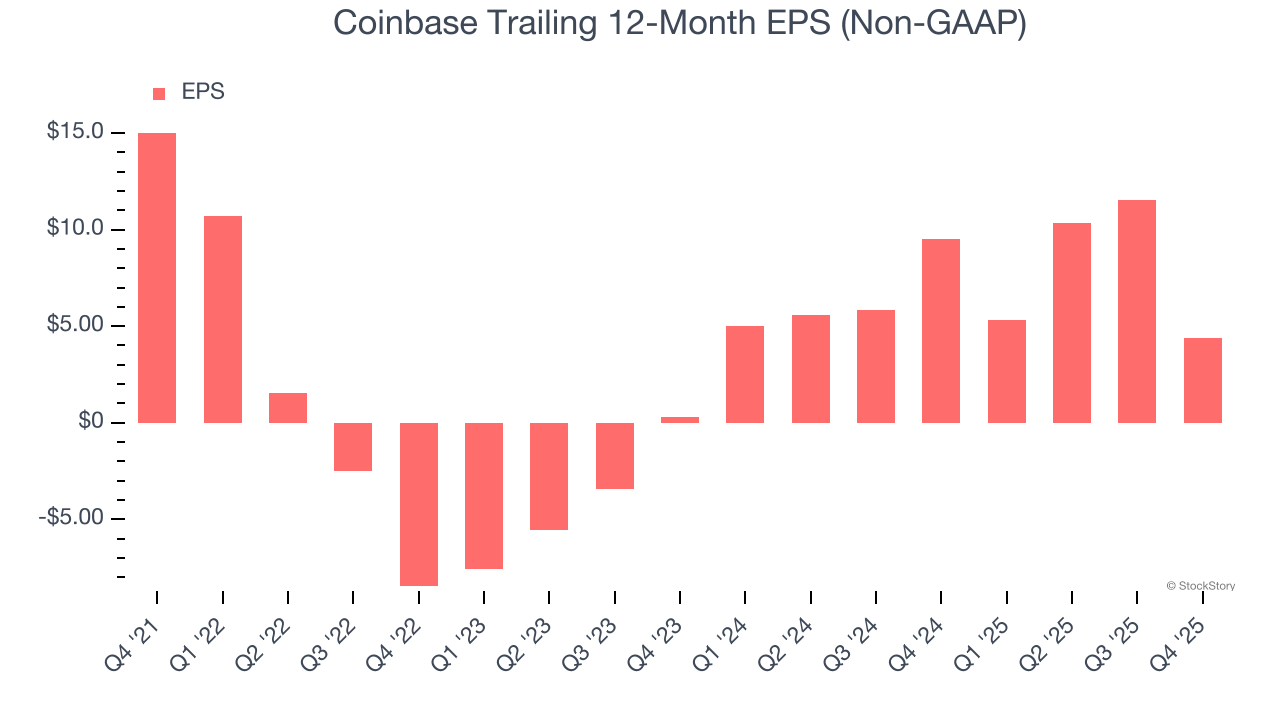

EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Coinbase’s full-year EPS dropped over the last four years. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Final Judgment

Coinbase’s merits more than compensate for its flaws. With the recent decline, the stock trades at 15× forward EV/EBITDA (or $174.10 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.