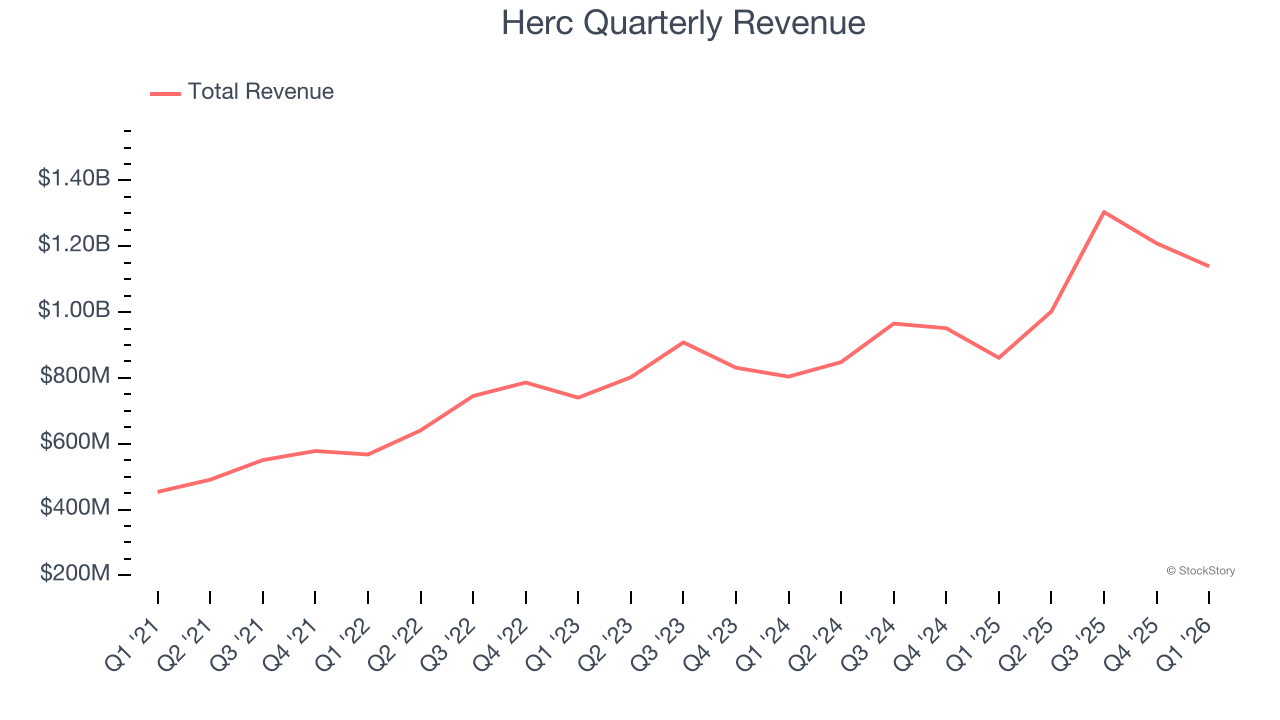

Equipment rental company Herc Holdings (NYSE: HRI) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 32.3% year on year to $1.14 billion. On the other hand, the company’s full-year revenue guidance of $4.34 billion at the midpoint came in 8.4% below analysts’ estimates. Its non-GAAP profit of $0.21 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Herc? Find out by accessing our full research report, it’s free.

Herc (HRI) Q1 CY2026 Highlights:

- Revenue: $1.14 billion vs analyst estimates of $1.08 billion (32.3% year-on-year growth, 5.3% beat)

- Adjusted EPS: $0.21 vs analyst estimates of -$0.21 (significant beat)

- Adjusted EBITDA: $448 million vs analyst estimates of $448.7 million (39.3% margin, in line)

- The company reconfirmed its revenue guidance for the full year of $4.34 billion at the midpoint

- EBITDA guidance for the full year is $2.05 billion at the midpoint, below analyst estimates of $2.06 billion

- Operating Margin: 15.8%, up from 6.2% in the same quarter last year

- Free Cash Flow Margin: 0.4%, down from 5.7% in the same quarter last year

- Market Capitalization: $4.16 billion

"The first quarter of 2026 marked a defining milestone for Herc Rentals as we successfully completed the integration of our H&E acquisition — the largest in the history of our industry — and we are already capturing the strategic benefits we anticipated: 25% more specialty locations, a stronger and deeper sales network, expanded share in local and regional accounts, and greater density in top metropolitan markets, where construction activity is most resilient. Financial performance in the first quarter was in line with our expectations and seasonal trends. While we expect performance to build as we move through the second half of 2026, the value of this combination will be realized over our three-year synergy plan, and we are executing against that roadmap with confidence,” said Larry Silber, chief executive officer.

Company Overview

Formerly a subsidiary of Hertz Corporation and with a logo that still bears some similarities to its former parent, Herc Holdings (NYSE: HRI) provides equipment rental and related services to a wide range of industries.

Revenue Growth

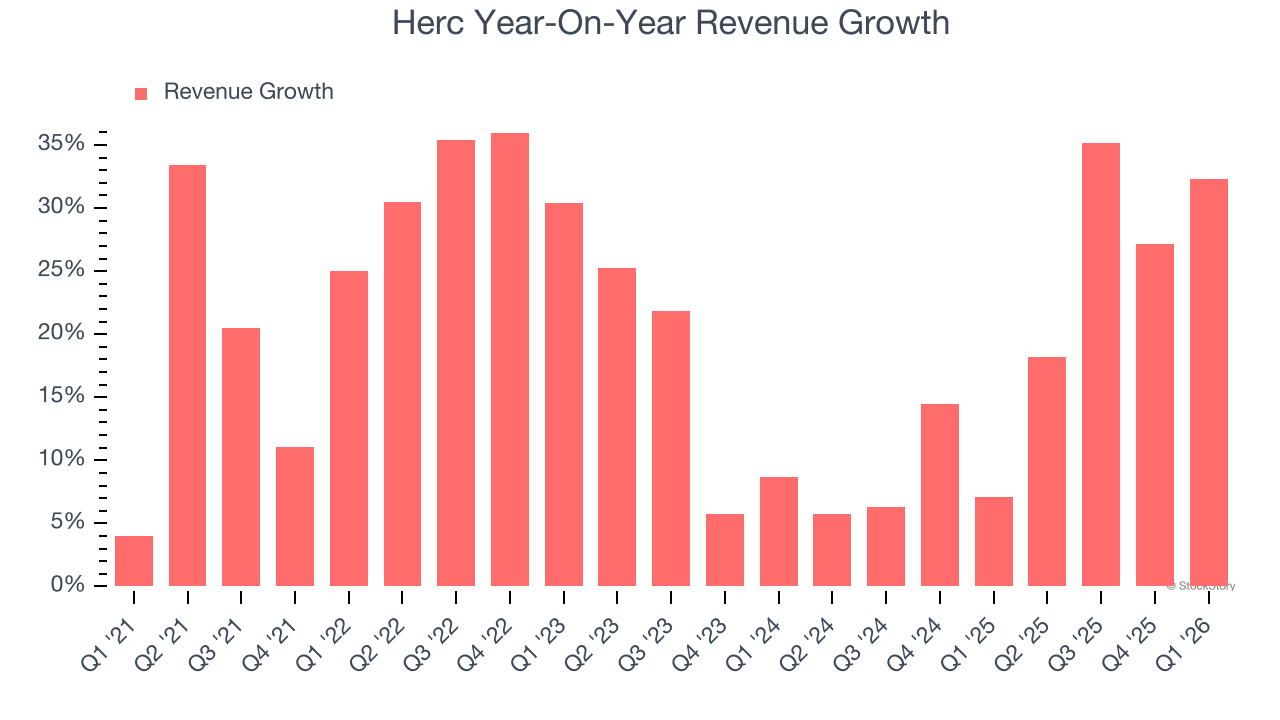

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Herc’s sales grew at an incredible 20.9% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Herc’s annualized revenue growth of 18% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

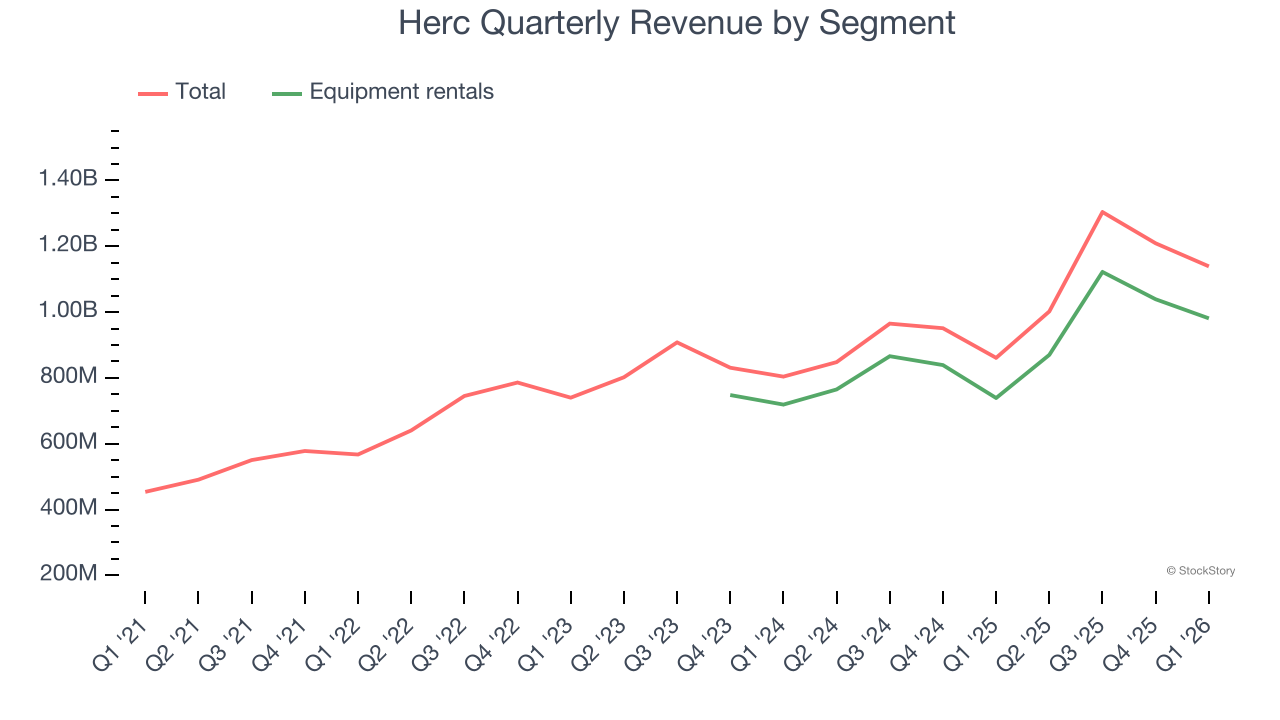

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Equipment rentals. Over the last two years, Herc’s Equipment rentals revenue (aerial, earthmoving, material handling) averaged 19.1% year-on-year growth.

This quarter, Herc reported wonderful year-on-year revenue growth of 32.3%, and its $1.14 billion of revenue exceeded Wall Street’s estimates by 5.3%.

Looking ahead, sell-side analysts expect revenue to grow 4.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

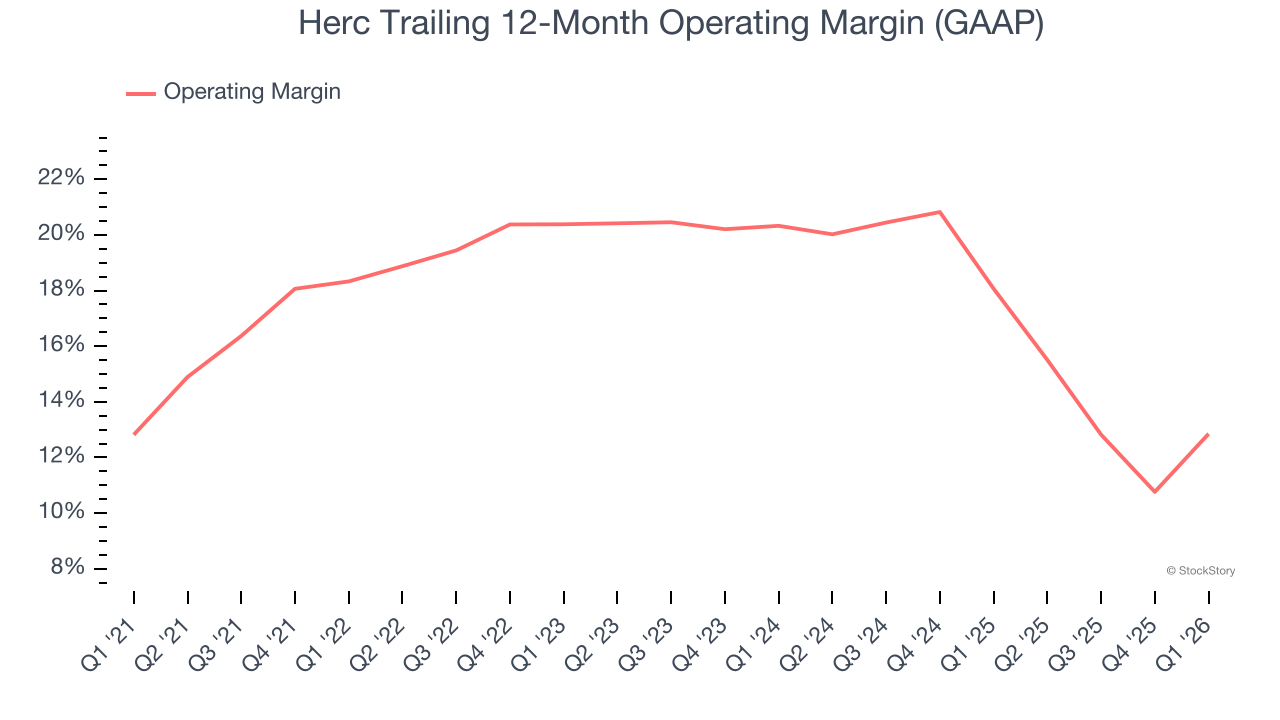

Herc has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.5%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Herc’s operating margin decreased by 5.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Herc generated an operating margin profit margin of 15.8%, up 9.6 percentage points year on year. The increase was solid, and because its gross margin actually decreased, we can assume it was more efficient because its operating expenses like marketing, R&D, and administrative overhead grew slower than its revenue.

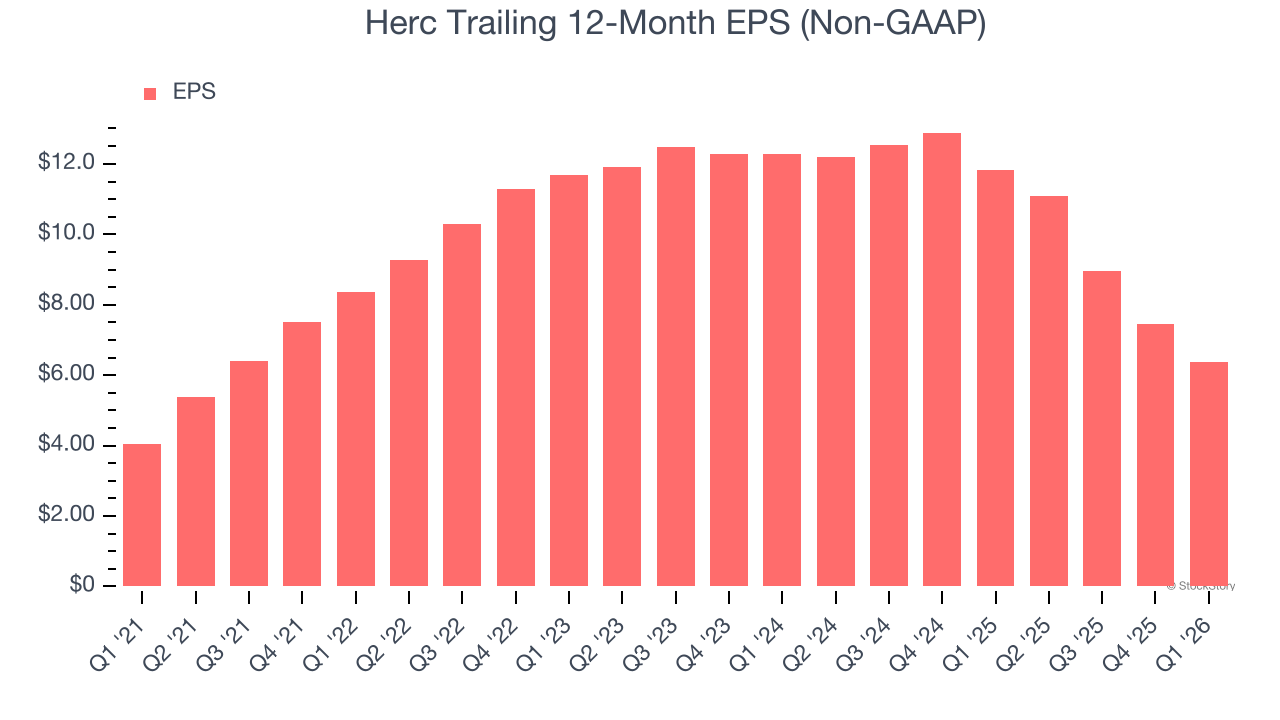

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Herc’s EPS grew at a decent 9.5% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 20.9% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

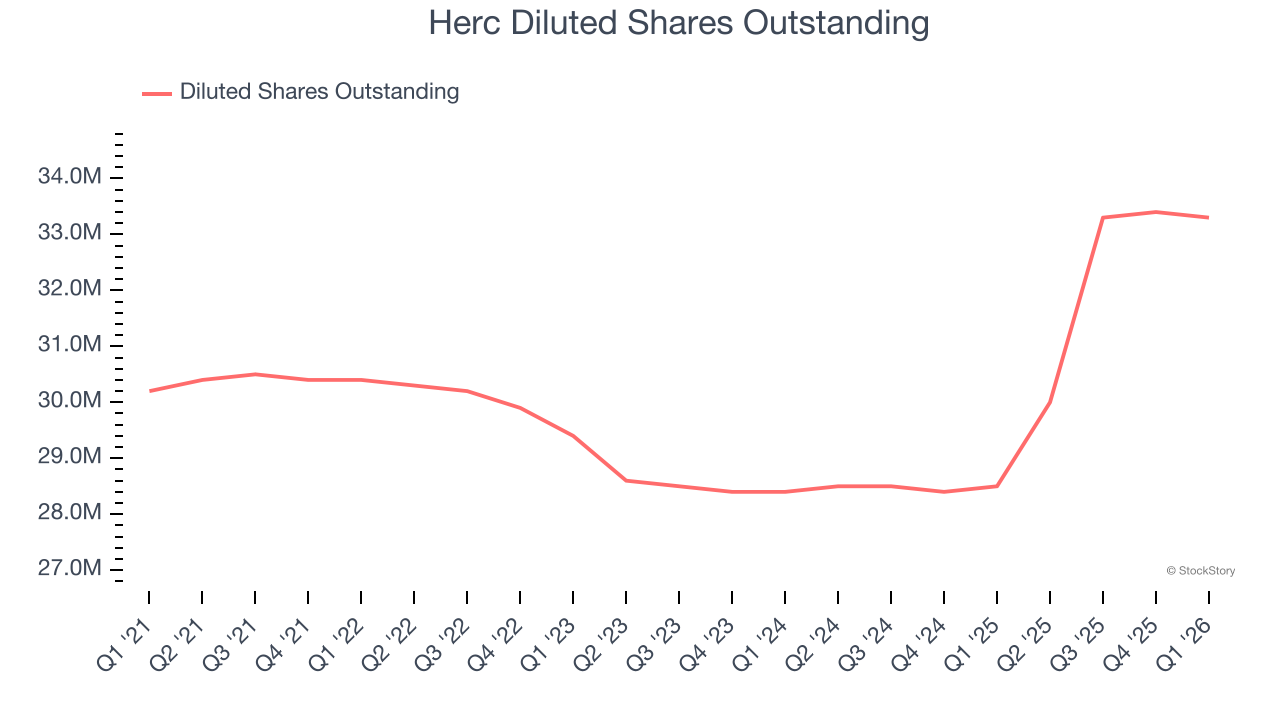

Diving into the nuances of Herc’s earnings can give us a better understanding of its performance. As we mentioned earlier, Herc’s operating margin expanded this quarter but declined by 5.5 percentage points over the last five years. Its share count also grew by 10.3%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Herc, its two-year annual EPS declines of 28% mark a reversal from its five-year trend. We hope Herc can return to earnings growth in the future.

In Q1, Herc reported adjusted EPS of $0.21, down from $1.30 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Herc’s full-year EPS of $6.37 to grow 7.8%.

Key Takeaways from Herc’s Q1 Results

It was good to see Herc beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock remained flat at $124.98 immediately following the results.

Is Herc an attractive investment opportunity at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).