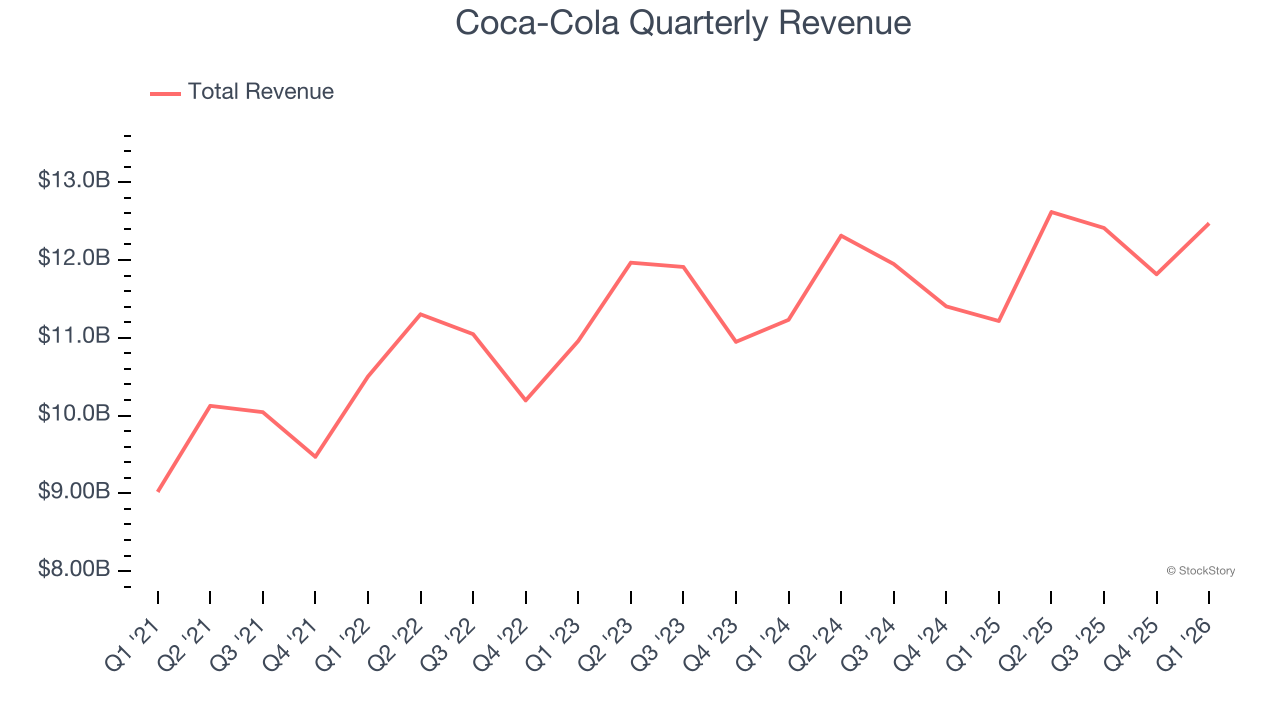

Beverage company Coca-Cola (NYSE: KO) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 11.2% year on year to $12.47 billion. Its non-GAAP profit of $0.86 per share was 5.9% above analysts’ consensus estimates.

Is now the time to buy Coca-Cola? Find out by accessing our full research report, it’s free.

Coca-Cola (KO) Q1 CY2026 Highlights:

- Revenue: $12.47 billion vs analyst estimates of $12.17 billion (11.2% year-on-year growth, 2.5% beat)

- Adjusted EPS: $0.86 vs analyst estimates of $0.81 (5.9% beat)

- Full-year EPS guide: raised EPS growth to 8-9%, up from its prior of 7-8%

- Operating Margin: 35%, up from 32.6% in the same quarter last year

- Free Cash Flow was $1.76 billion, up from -$5.51 billion in the same quarter last year

- Organic Revenue rose 10% year on year (beat)

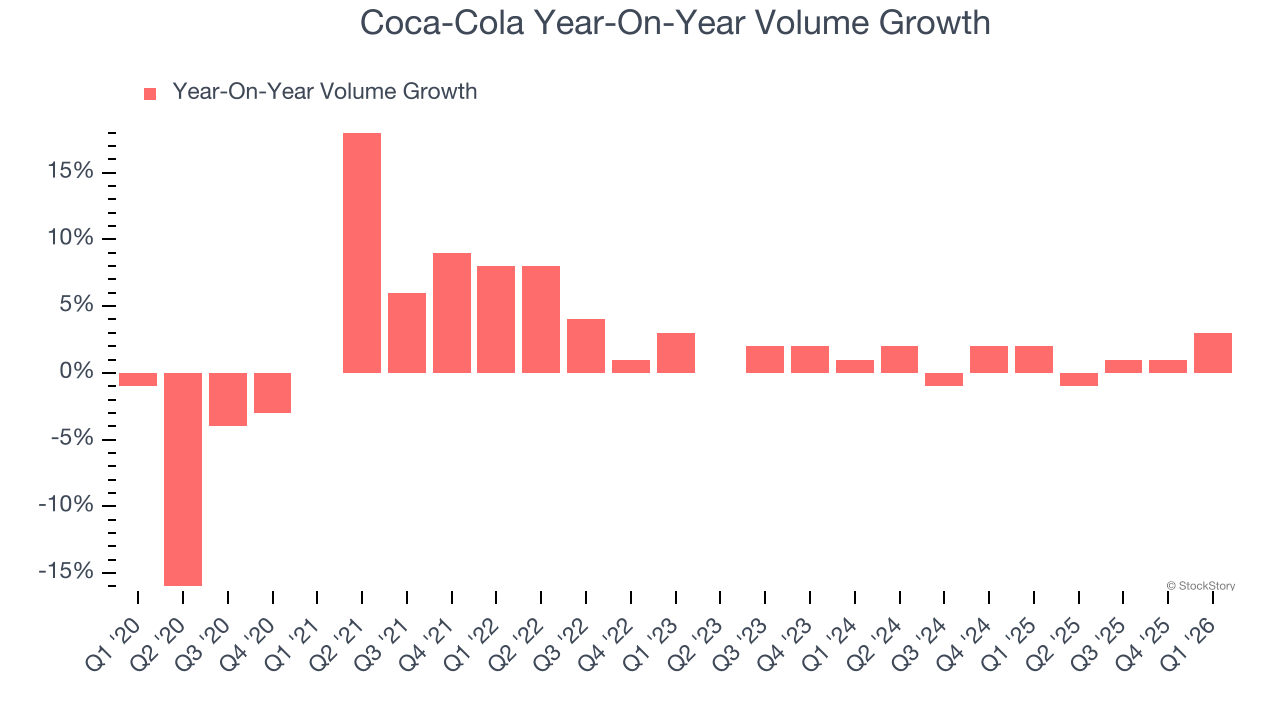

- Sales Volumes rose 3% year on year (2% in the same quarter last year)

- Market Capitalization: $324.7 billion

Company Overview

A pioneer and behemoth in carbonated soft drinks, Coca-Cola (NYSE: KO) is a storied beverage company best known for its flagship soda.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $49.32 billion in revenue over the past 12 months, Coca-Cola is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because there are only so many big store chains to sell into, making it harder to find incremental growth. To expand meaningfully, Coca-Cola likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Coca-Cola’s sales grew at a tepid 4.3% compounded annual growth rate over the last three years, but to its credit, consumers bought more of its products.

This quarter, Coca-Cola reported year-on-year revenue growth of 11.2%, and its $12.47 billion of revenue exceeded Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to decline by 1.1% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and implies its products will see some demand headwinds. At least the company is tracking well in other measures of financial health.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

To analyze whether Coca-Cola generated its growth from changes in price or volume, we can compare its volume growth to its organic revenue growth, which excludes non-fundamental impacts on company financials like mergers and currency fluctuations.

Over the last two years, Coca-Cola’s average quarterly volume growth was a healthy 1.1%. Even with this good performance, we can see that most of the company’s gains have come from price increases by looking at its 8.8% average organic revenue growth. The ability to sell more products while raising prices indicates that Coca-Cola enjoys some degree of inelastic demand.

In Coca-Cola’s Q1 2026, sales volumes jumped 3% year on year. This result was an acceleration from its historical levels, certainly a positive signal.

Key Takeaways from Coca-Cola’s Q1 Results

We enjoyed seeing Coca-Cola beat analysts’ organic revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. Looking ahead, the company raised full-year EPS guide. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 2.6% to $77.49 immediately after reporting.

Coca-Cola put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).