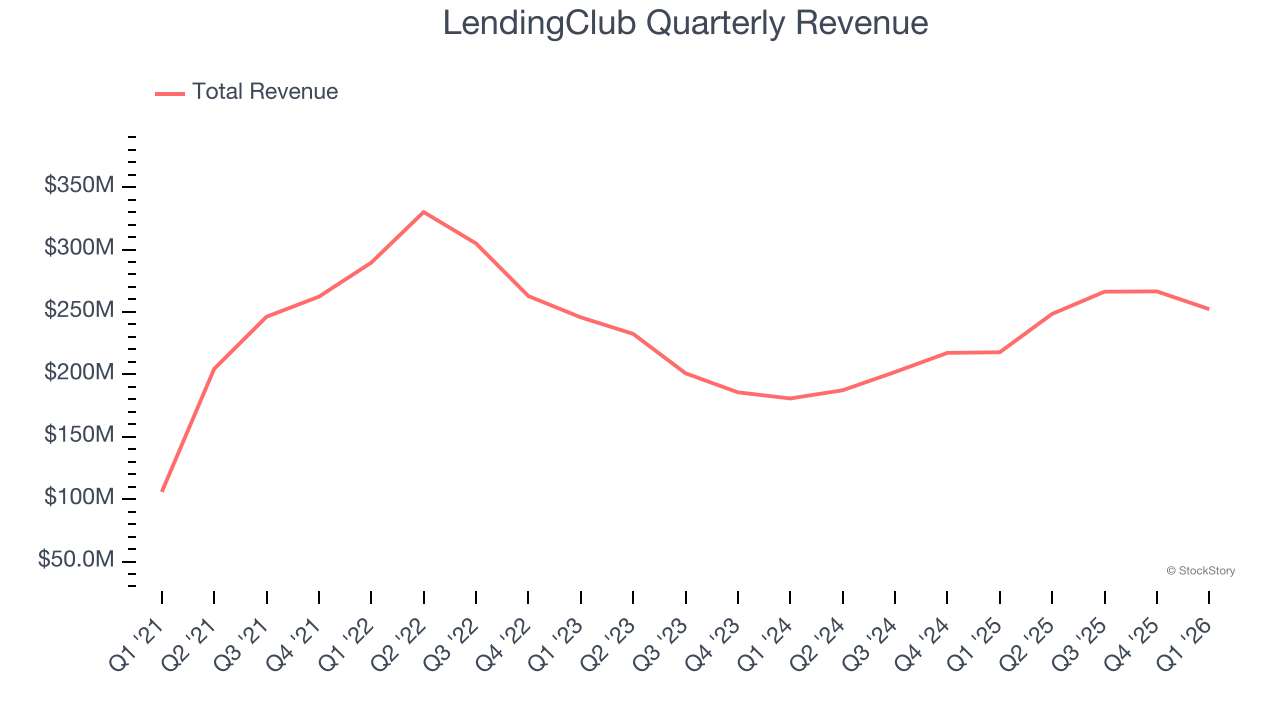

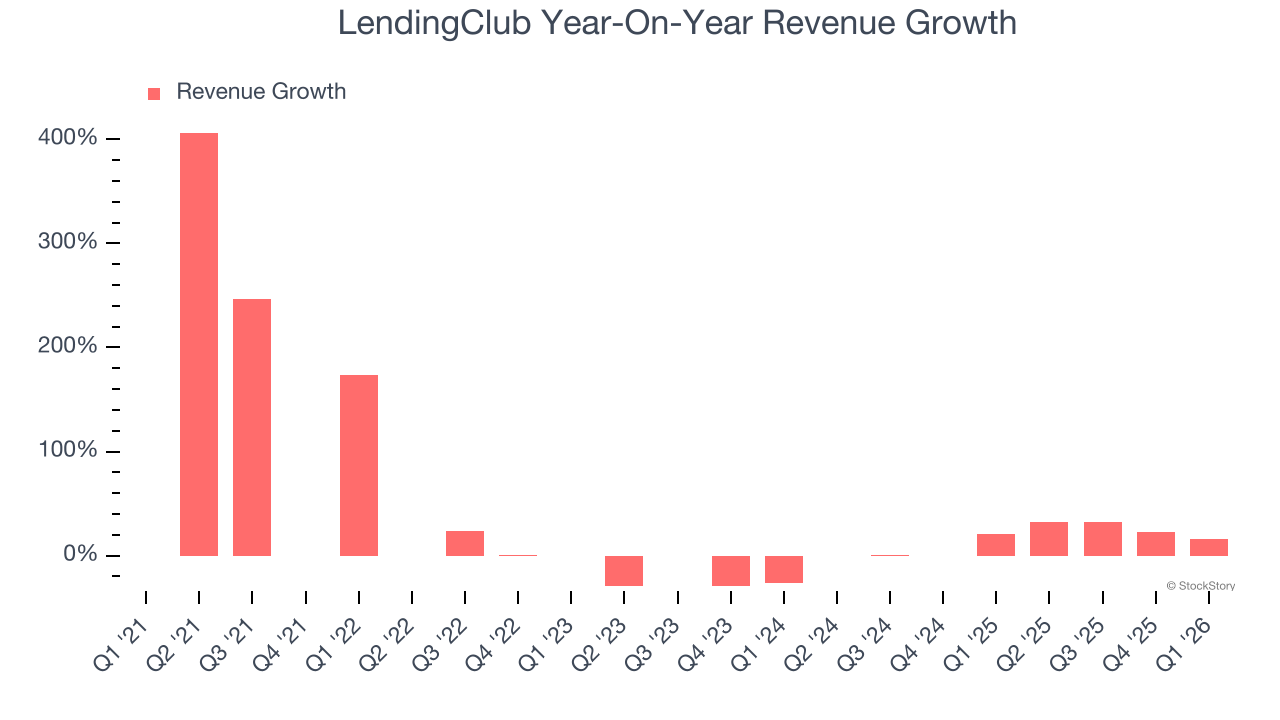

Digital lending platform LendingClub (NYSE: LC) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 15.9% year on year to $252.3 million. Its GAAP profit of $0.44 per share was 21.7% above analysts’ consensus estimates.

Is now the time to buy LendingClub? Find out by accessing our full research report, it’s free.

LendingClub (LC) Q1 CY2026 Highlights:

- Revenue: $252.3 million vs analyst estimates of $249.2 million (15.9% year-on-year growth, 1.2% beat)

- Pre-tax Profit: $67.33 million (26.7% margin)

- EPS (GAAP): $0.44 vs analyst estimates of $0.36 (21.7% beat)

- EPS (GAAP) guidance for the full year is $1.73 at the midpoint, roughly in line with what analysts were expecting

- Market Capitalization: $2.01 billion

"We're starting 2026 with exceptional momentum, delivering 31% year-over-year growth in originations while achieving record pre-tax earnings of $67 million and ROTCE of 14.5%," said Scott Sanborn, LendingClub CEO.

Company Overview

Pioneering peer-to-peer lending in the US before evolving into a digital bank, LendingClub (NYSE: LC) operates a marketplace that connects borrowers with lenders, offering personal loans, auto refinancing, and banking services.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, LendingClub’s revenue grew at an incredible 28.7% compounded annual growth rate over the last five years. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. LendingClub’s annualized revenue growth of 13.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, LendingClub reported year-on-year revenue growth of 15.9%, and its $252.3 million of revenue exceeded Wall Street’s estimates by 1.2%.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Key Takeaways from LendingClub’s Q1 Results

It was good to see LendingClub beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 13% to $19.73 immediately following the results.

LendingClub had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).