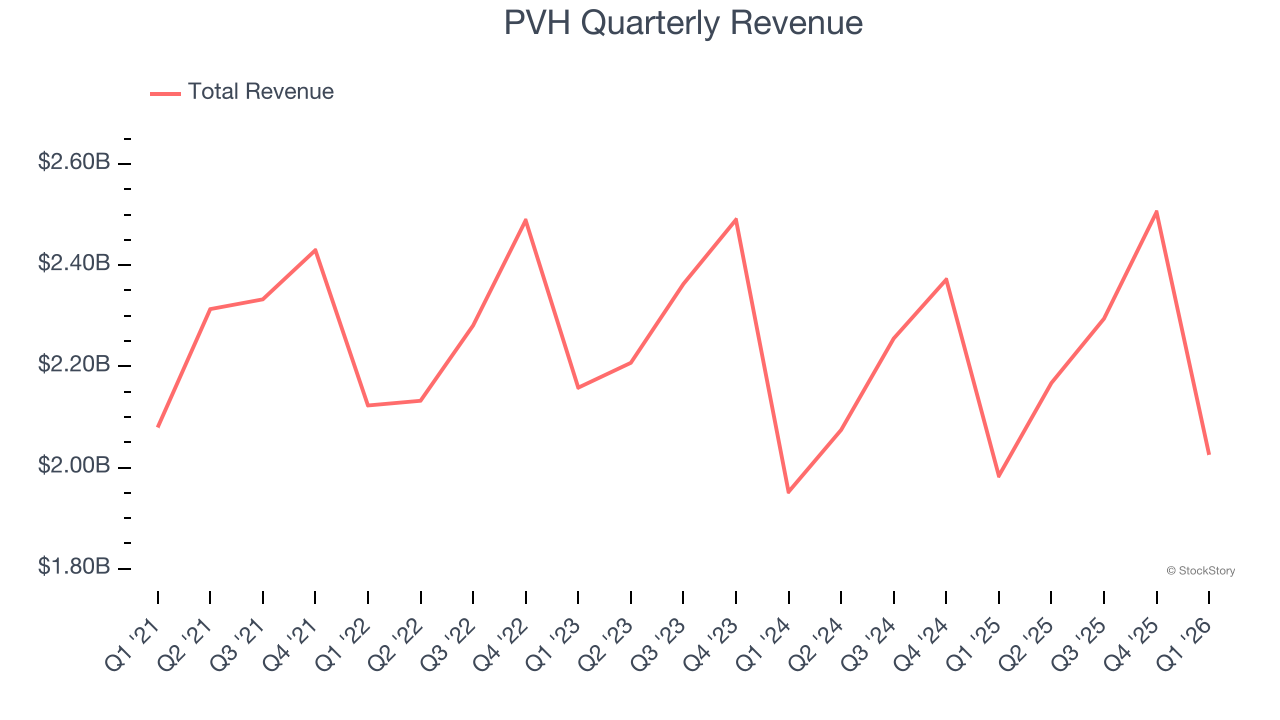

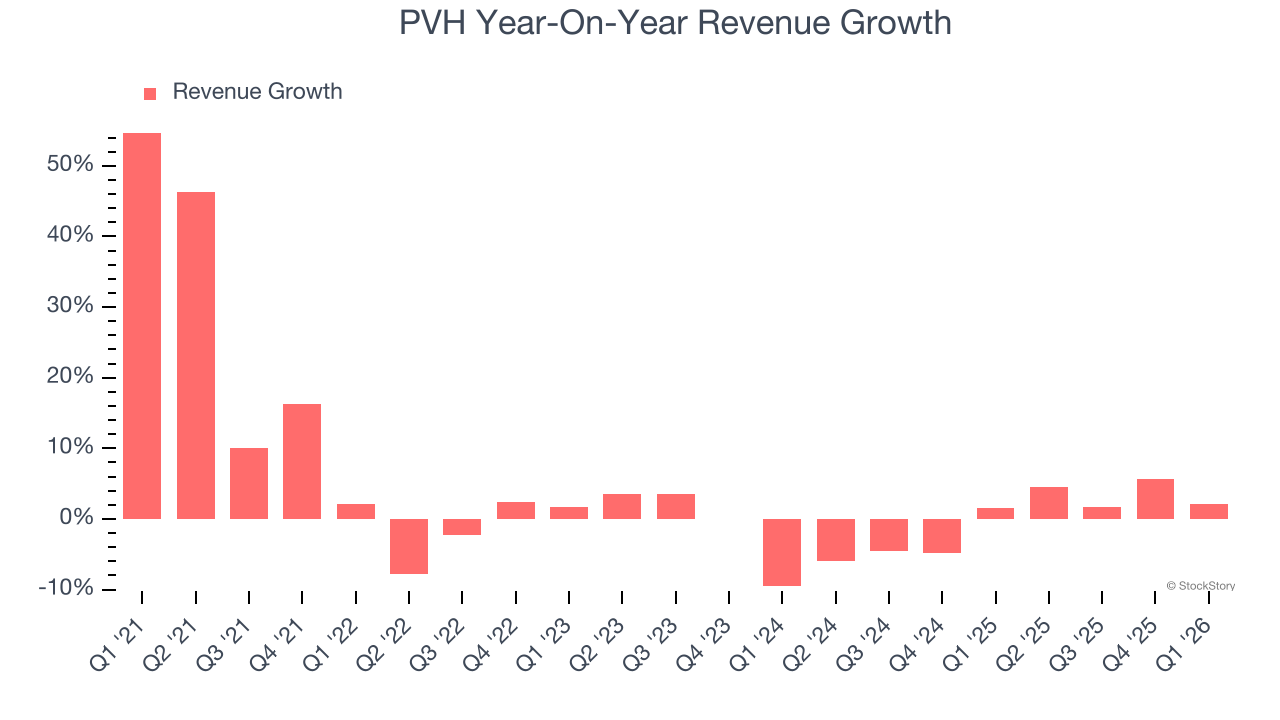

Fashion conglomerate PVH (NYSE: PVH) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 2.1% year on year to $2.03 billion. Its non-GAAP profit of $2.01 per share was 10.5% above analysts’ consensus estimates.

Is now the time to buy PVH? Find out by accessing our full research report, it’s free.

PVH (PVH) Q1 CY2026 Highlights:

- Revenue: $2.03 billion vs analyst estimates of $1.99 billion (2.1% year-on-year growth, 1.5% beat)

- Adjusted EPS: $2.01 vs analyst estimates of $1.82 (10.5% beat)

- Adjusted EPS guidance for the full year is $11.95 at the midpoint, missing analyst estimates by 1.3%

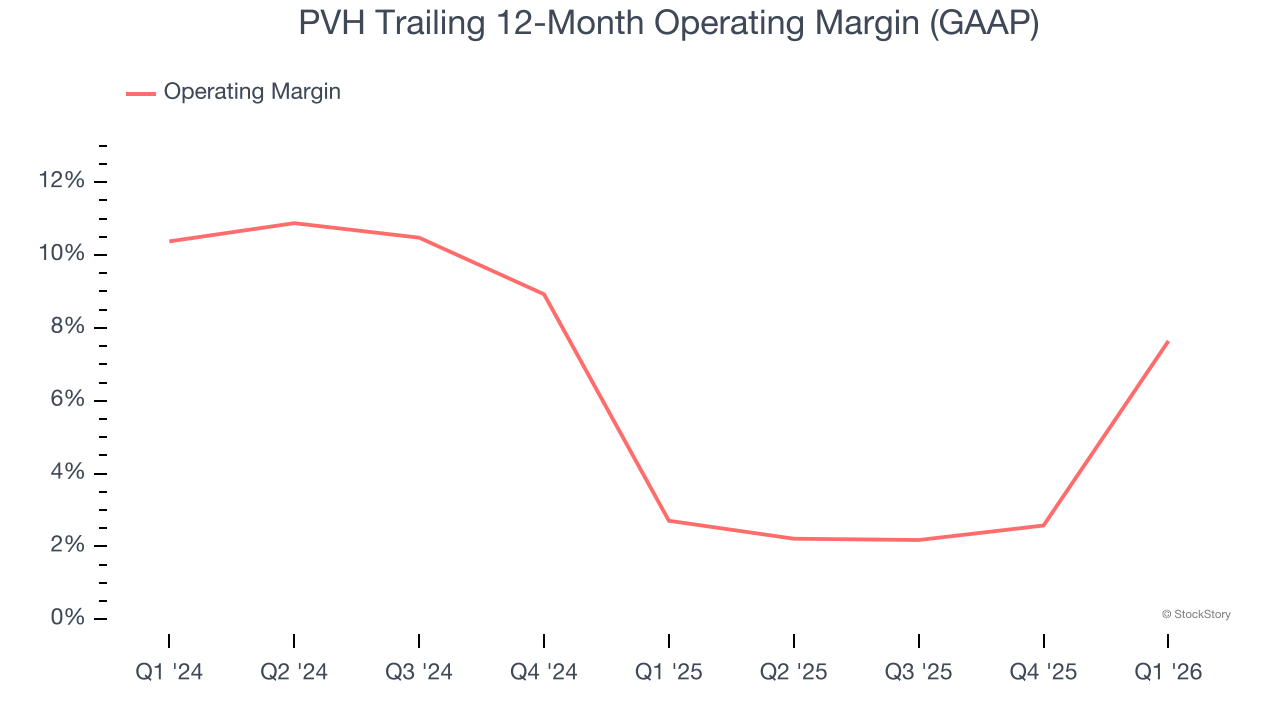

- Operating Margin: 6.1%, up from -16.7% in the same quarter last year

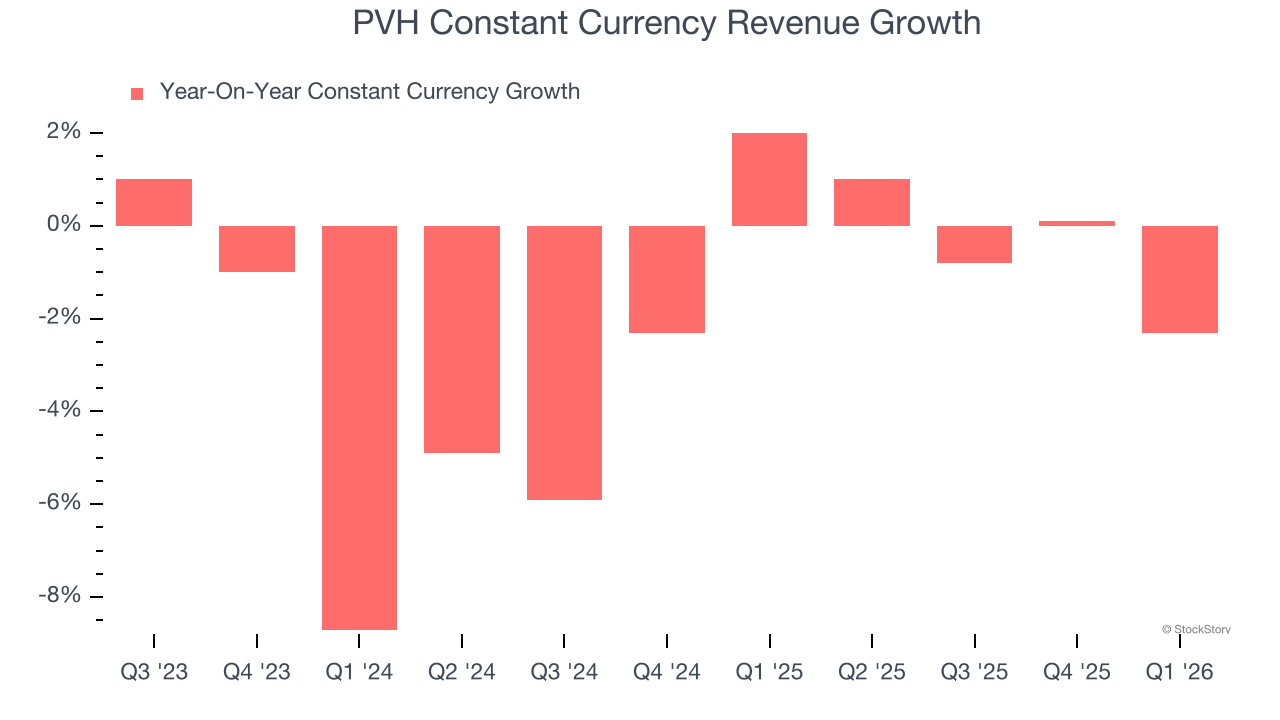

- Constant Currency Revenue fell 2.3% year on year (2% in the same quarter last year)

- Market Capitalization: $4.48 billion

Company Overview

Founded in 1881 by a husband and wife duo, PVH (NYSE: PVH) is a global fashion conglomerate with iconic brands like Calvin Klein and Tommy Hilfiger.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, PVH grew its sales at a weak 2.7% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. PVH’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 1.6% year-on-year declines. Because this number is lower than its normal revenue growth, we can see that foreign exchange rates have boosted PVH’s performance.

This quarter, PVH reported modest year-on-year revenue growth of 2.1% but beat Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and suggests its newer products and services will not accelerate its top-line performance yet.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

PVH’s operating margin has been trending up over the last 12 months and averaged 5.2% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, PVH generated an operating margin profit margin of 6.1%, up 22.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

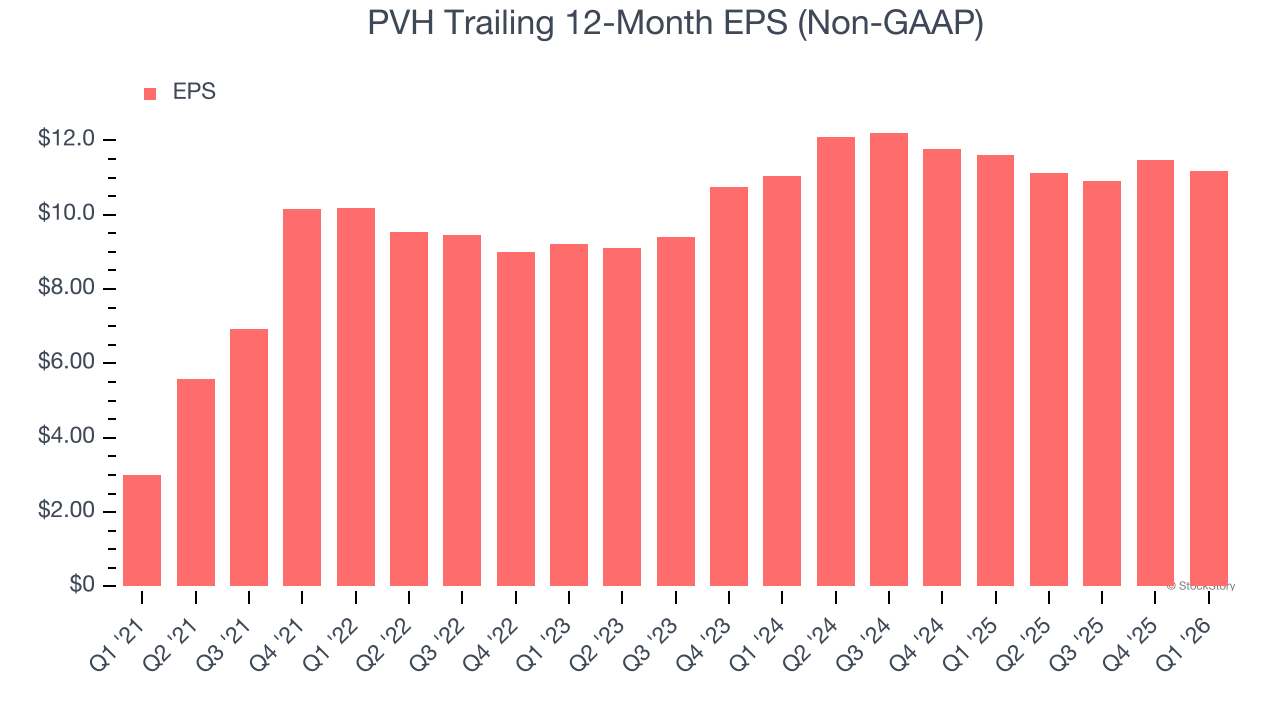

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

PVH’s EPS grew at 30.2% compounded annual growth rate over the last five years, higher than its 2.7% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q1, PVH reported adjusted EPS of $2.01, down from $2.30 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects PVH’s full-year EPS to grow 12.3% from $11.18 to $12.55.

Key Takeaways from PVH’s Q1 Results

We were impressed by PVH’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its EBITDA missed and its full-year EPS guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The market seemed to be hoping for more, and the stock traded down 19.7% to $78.67 immediately following the results.

Big picture, is PVH a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).