Over the last six months, Clorox’s shares have sunk to $90.24, producing a disappointing 15.2% loss - a stark contrast to the S&P 500’s 10.9% gain. This might have investors contemplating their next move.

Is now the time to buy Clorox, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Clorox Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons we avoid CLX, plus one stock we’d rather own.

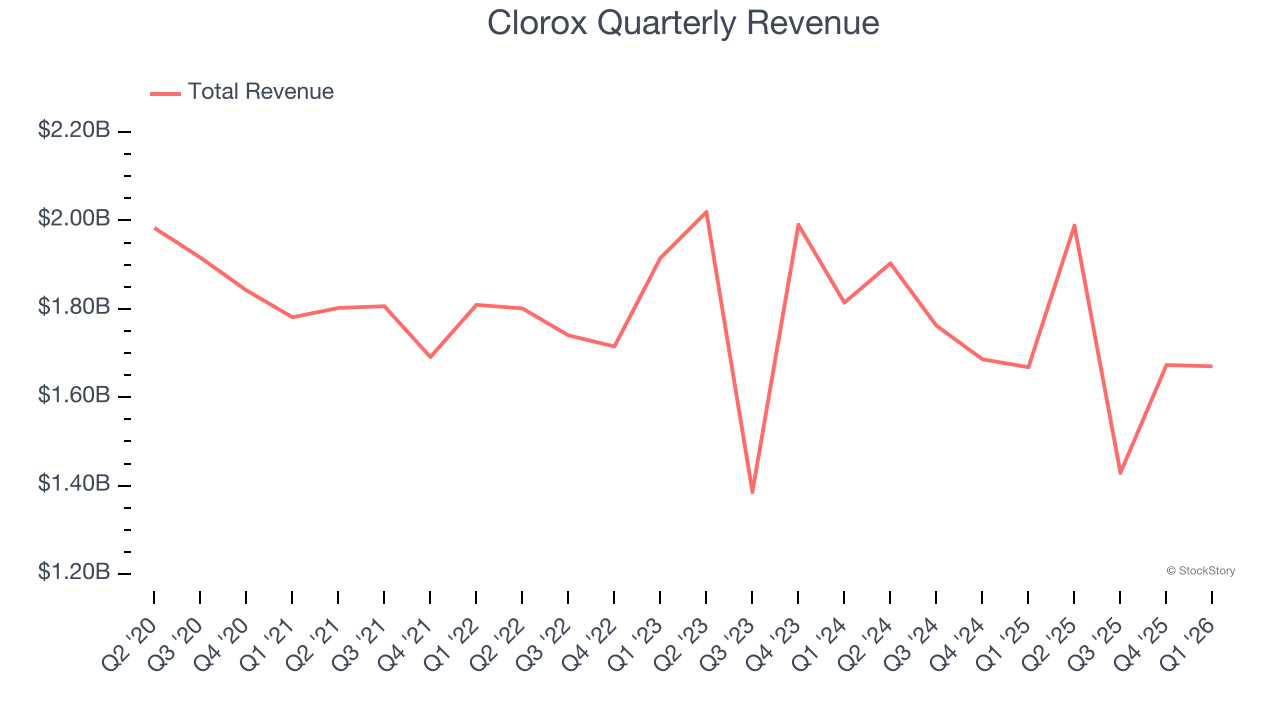

1. Revenue Spiraling Downwards

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Clorox’s demand was weak over the last three years as its sales fell at a 1.9% annual rate. This was below our standards and signals it’s a lower quality business.

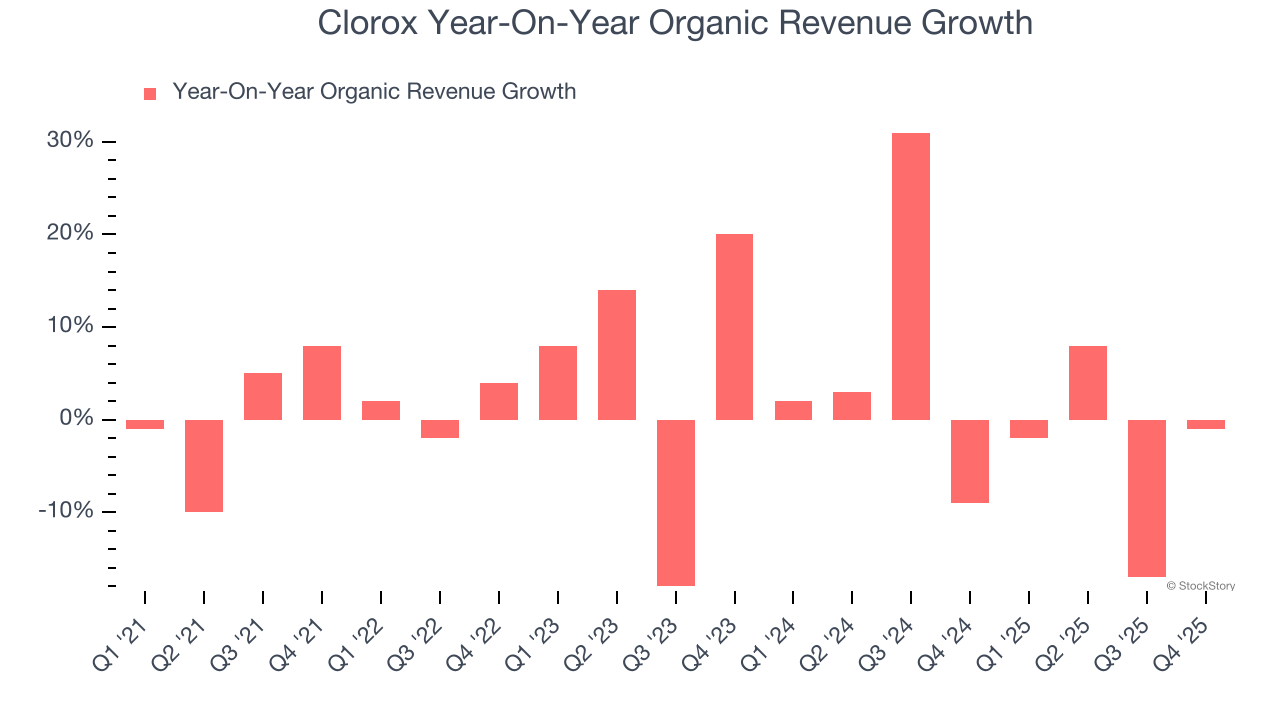

2. Slow Organic Growth Suggests Waning Demand In Core Business

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Clorox’s products has been stable over the last eight quarters but fell behind the broader sector. On average, the company has posted feeble year-on-year organic revenue growth of 1.9%.

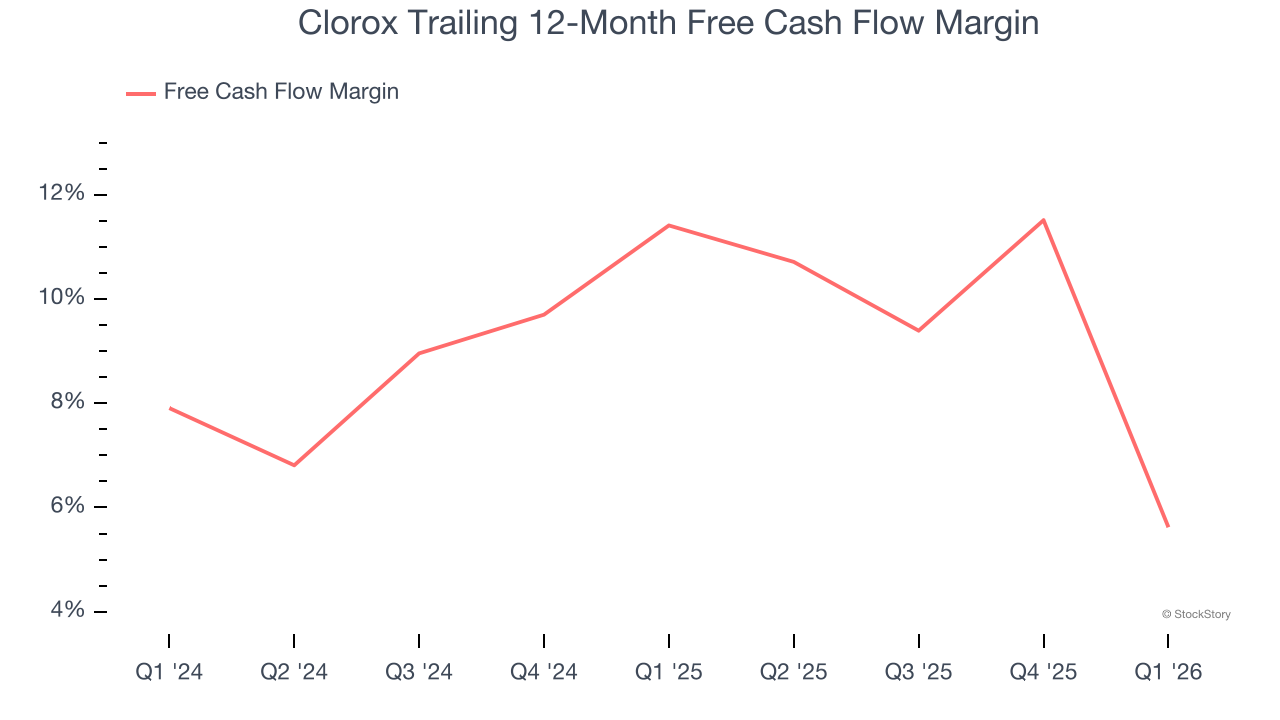

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Clorox’s margin dropped by 5.8 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity. Clorox’s free cash flow margin for the trailing 12 months was 5.6%.

Final Judgment

Clorox’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 15.9× forward P/E (or $90.24 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re pretty confident there are superior stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Clorox

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.