As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the aerospace industry, including Hexcel (NYSE: HXL) and its peers.

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

The 14 aerospace stocks we track reported a very strong Q1. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 1.4% above.

Thankfully, share prices of the companies have been resilient as they are up 7.2% on average since the latest earnings results.

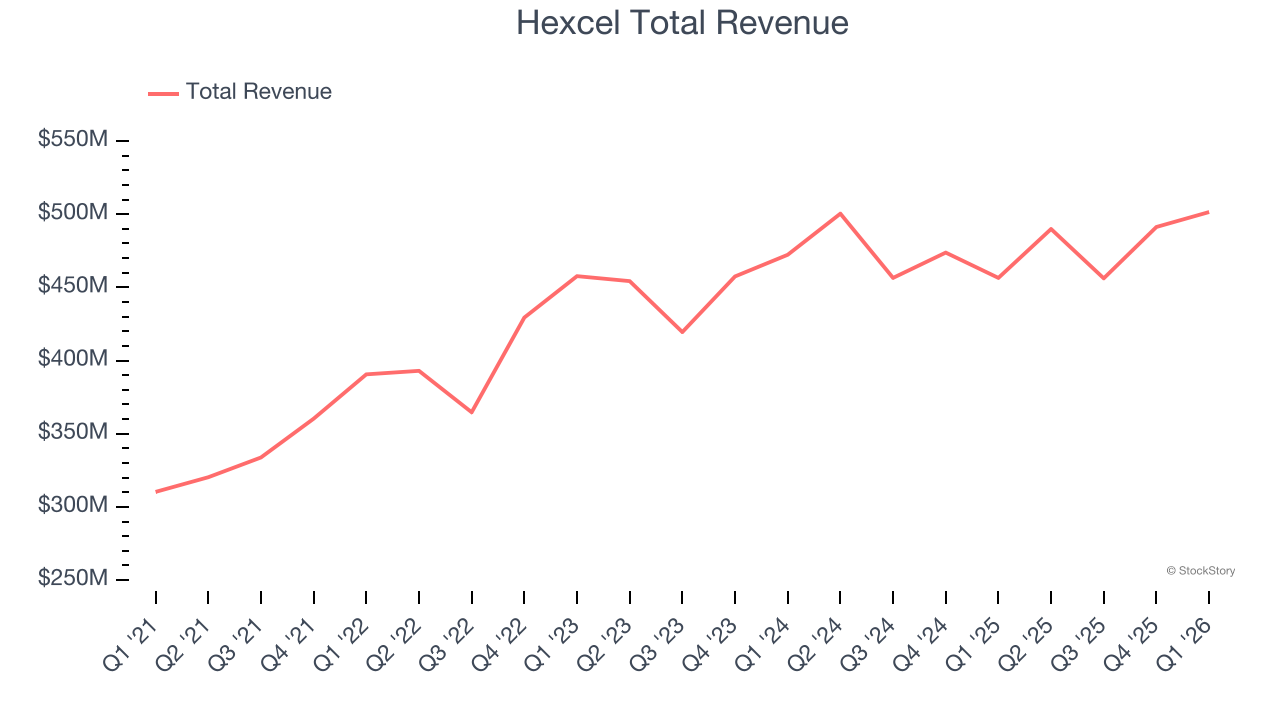

Hexcel (NYSE: HXL)

Founded shortly after World War II by a group of engineers from UC Berkley, Hexcel (NYSE: HXL) manufactures lightweight composite materials primarily for the aerospace and defense sectors.

Hexcel reported revenues of $501.5 million, up 9.9% year on year. This print exceeded analysts’ expectations by 3.4%. Overall, it was a very strong quarter for the company with a beat of analysts’ EPS and EBITDA estimates.

Chairman, CEO and President Tom Gentile said, “The Hexcel team delivered strong first quarter results on rising commercial aerospace build rates supported by the normalization of channel inventory. Our first quarter sales increased ten percent and earnings per share grew at a significantly higher rate, underscoring the benefit from significant operating leverage as we grow back into existing capacity. Our priorities remain centered on execution and operational discipline as we support the rate ramps of our customers.”

Hexcel delivered the weakest full-year guidance update of the whole group. Interestingly, the stock is up 2.4% since reporting and currently trades at $89.27.

Is now the time to buy Hexcel? Access our full analysis of the earnings results here, it’s free.

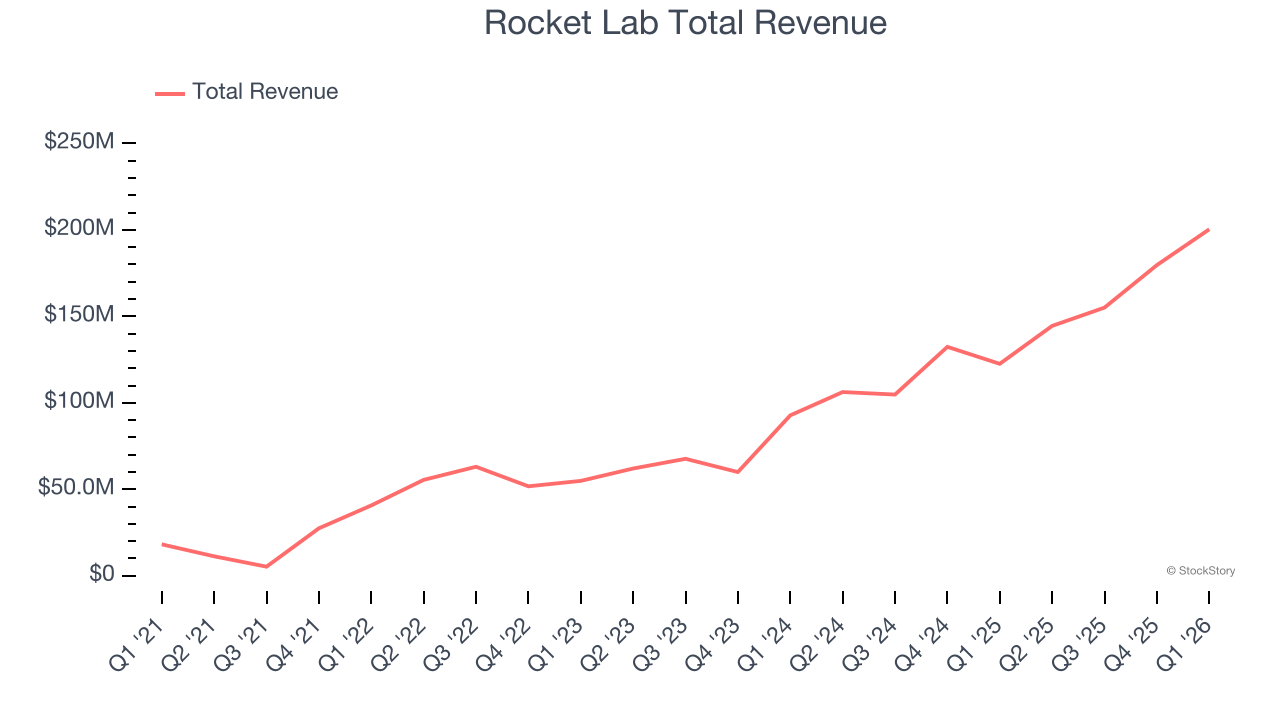

Best Q1: Rocket Lab (NASDAQ: RKLB)

Becoming the first private company in the Southern Hemisphere to reach space, Rocket Lab (NASDAQ: RKLB) offers rockets designed for launching small satellites.

Rocket Lab reported revenues of $200.3 million, up 63.5% year on year, outperforming analysts’ expectations by 4.9%. The business had an incredible quarter with EBITDA guidance for next quarter exceeding analysts’ expectations and a beat of analysts’ EPS estimates.

Rocket Lab delivered the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 65.9% since reporting. It currently trades at $130.33.

Is now the time to buy Rocket Lab? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: AerSale (NASDAQ: ASLE)

Providing a one-stop shop that integrates multiple services and product offerings, AerSale (NASDAQ: ASLE) delivers full-service support to mid-life commercial aircraft.

AerSale reported revenues of $70.61 million, up 7.4% year on year, falling short of analysts’ expectations by 31.1%. It was a softer quarter as it posted a significant miss of analysts’ revenue and adjusted operating income estimates.

AerSale delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 13.3% since the results and currently trades at $6.35.

Read our full analysis of AerSale’s results here.

TransDigm (NYSE: TDG)

Supplying parts for nearly all aircraft currently in service, TransDigm (NYSE: TDG) develops and manufactures components and systems for military and commercial aviation.

TransDigm reported revenues of $2.54 billion, up 18.3% year on year. This print beat analysts’ expectations by 3.1%. Overall, it was an exceptional quarter as it also recorded a solid beat of analysts’ adjusted operating income and revenue estimates.

The stock is up 2.5% since reporting and currently trades at $1,179.

Read our full, actionable report on TransDigm here, it’s free.

Curtiss-Wright (NYSE: CW)

Formed from a merger of 12 companies, Curtiss-Wright (NYSE: CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

Curtiss-Wright reported revenues of $913.7 million, up 13.4% year on year. This result topped analysts’ expectations by 5.1%. It was a very strong quarter as it also produced an impressive beat of analysts’ revenue and adjusted operating income estimates.

The stock is down 4.4% since reporting and currently trades at $710.49.

Read our full, actionable report on Curtiss-Wright here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.