Simply Good Foods’s stock price has taken a beating over the past six months, shedding 38.8% of its value and falling to $11.86 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Simply Good Foods, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Simply Good Foods Will Underperform?

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why SMPL doesn't excite us and a stock we'd rather own.

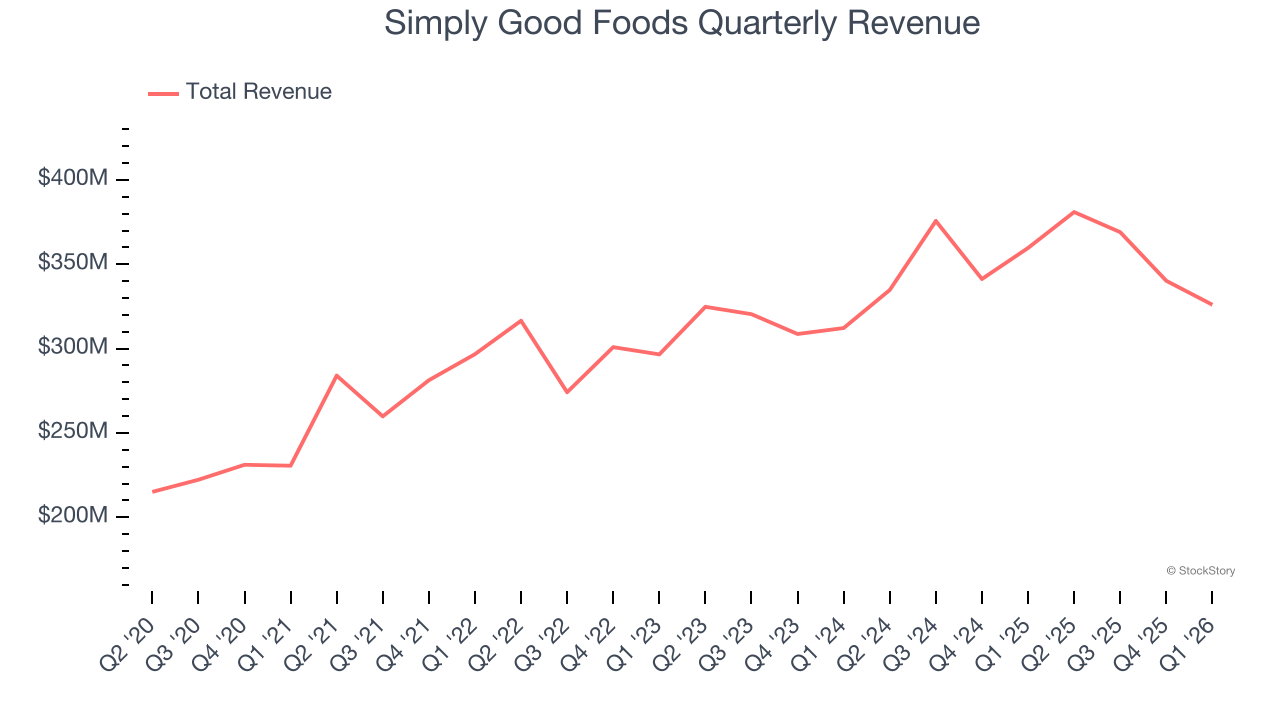

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Simply Good Foods’s sales grew at a mediocre 6% compounded annual growth rate over the last three years. This fell short of our benchmark for the consumer staples sector.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Simply Good Foods’s revenue to drop by 4.9%. This projection is underwhelming and indicates its products will face some demand challenges.

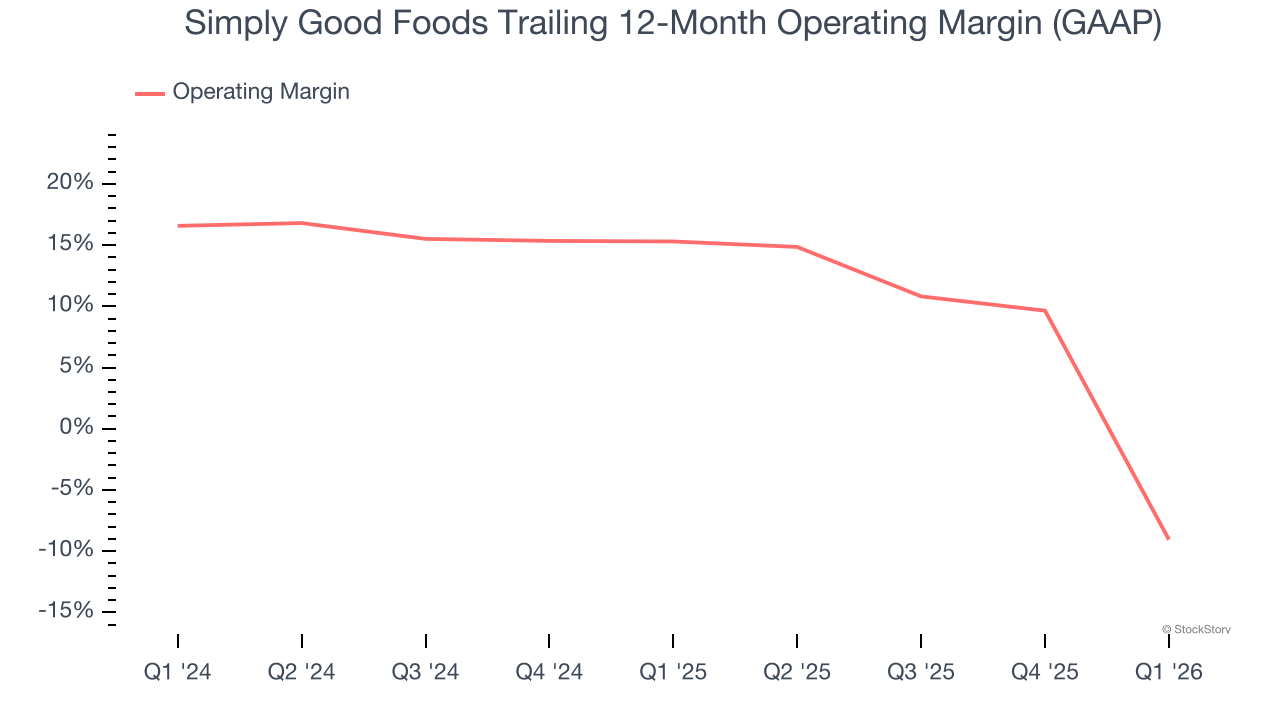

3. Shrinking Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, Simply Good Foods’s operating margin decreased by 24.4 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Simply Good Foods’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 9.1%.

Final Judgment

We see the value of companies helping consumers, but in the case of Simply Good Foods, we’re out. After the recent drawdown, the stock trades at 7.2× forward P/E (or $11.86 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Like More Than Simply Good Foods

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.