The past six months have been a windfall for Valaris’s shareholders. The company’s stock price has jumped 90.6%, hitting $91.79 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Valaris, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Valaris Will Underperform?

Despite the momentum, we're swiping left on Valaris for now. Here are three reasons there are better opportunities than VAL and a stock we'd rather own.

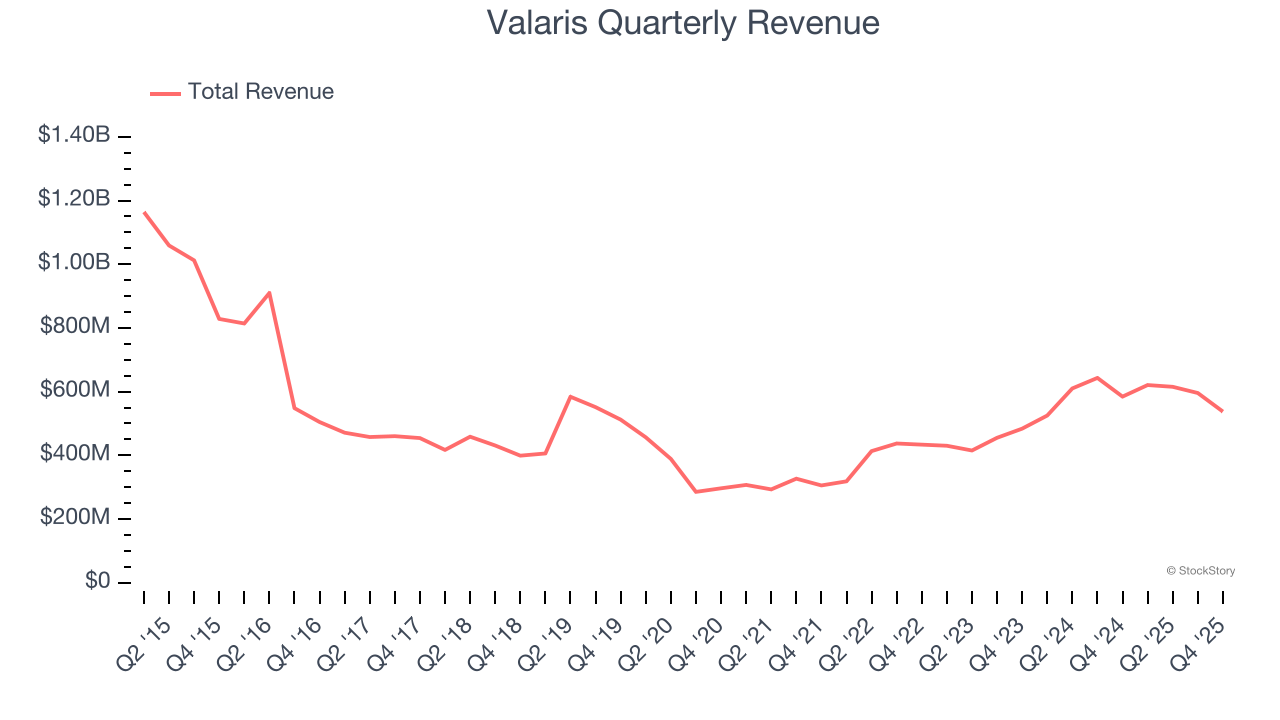

1. Long-Term Revenue Growth Shows Momentum

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Luckily, Valaris’s sales grew at a decent 10.7% compounded annual growth rate over the last five years. Its growth was slightly above the average energy upstream and integrated energy company and shows its offerings resonate with customers.

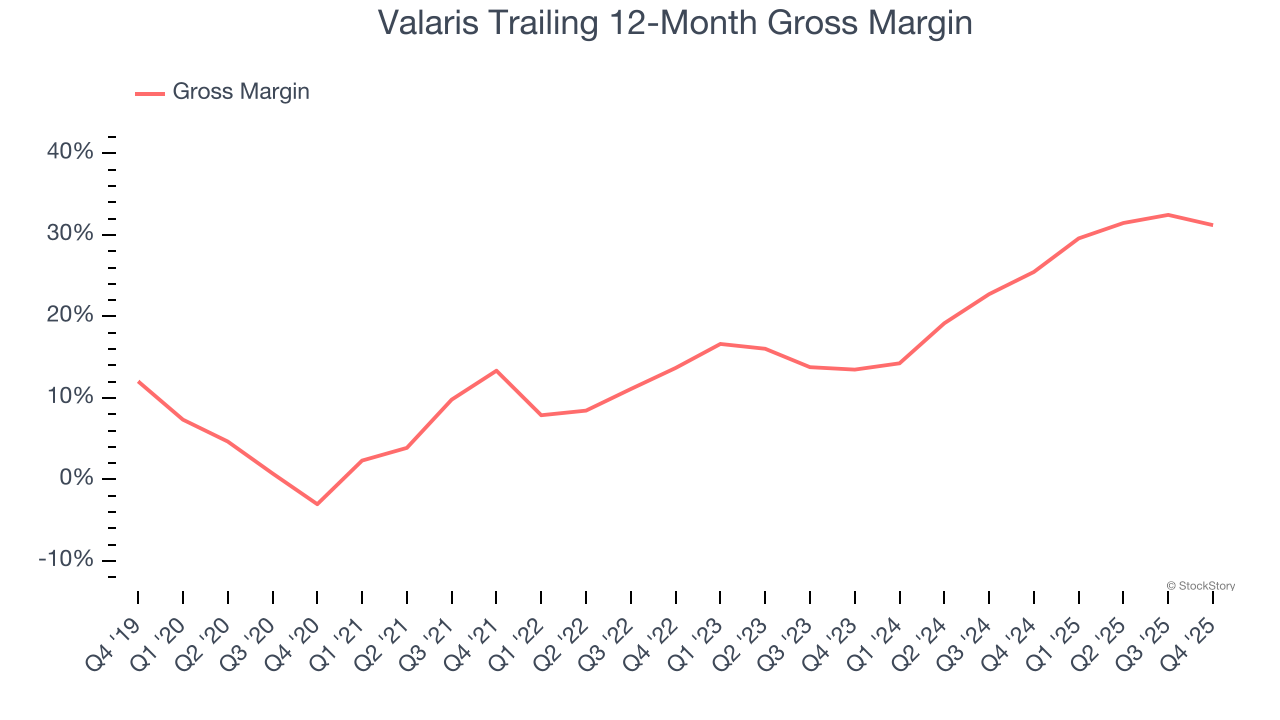

2. Low Gross Margin Reveals Weak Structural Profitability

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Valaris, which averaged 21% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

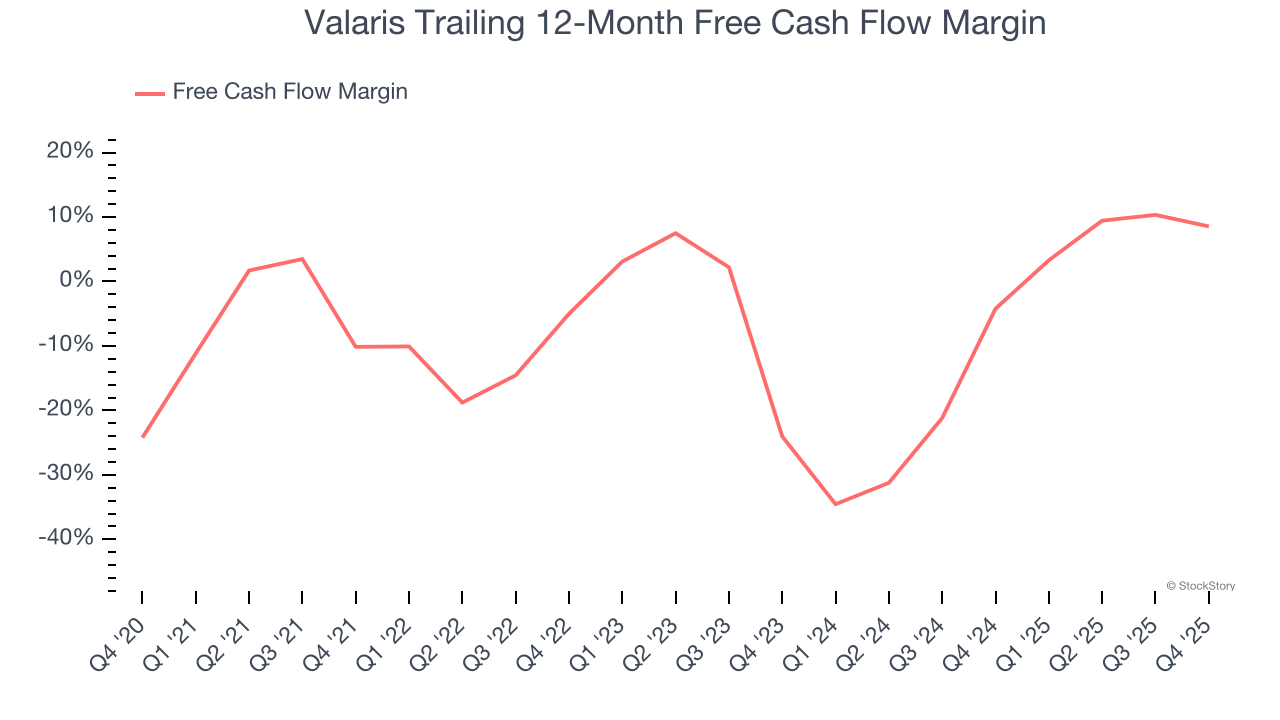

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Valaris’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 5.7%, meaning it lit $5.68 of cash on fire for every $100 in revenue.

Final Judgment

We see the value of companies helping consumers, but in the case of Valaris, we’re out. Following the recent surge, the stock trades at 29.3× forward P/E (or $91.79 per share). This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Valaris

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.