What a brutal six months it’s been for Paylocity. The stock has dropped 32.5% and now trades at $100.30, rattling many shareholders. This might have investors contemplating their next move.

Is now the time to buy Paylocity, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Paylocity Not Exciting?

Even though the stock has become cheaper, we don't have much confidence in Paylocity. Here are three reasons you should be careful with PCTY and a stock we'd rather own.

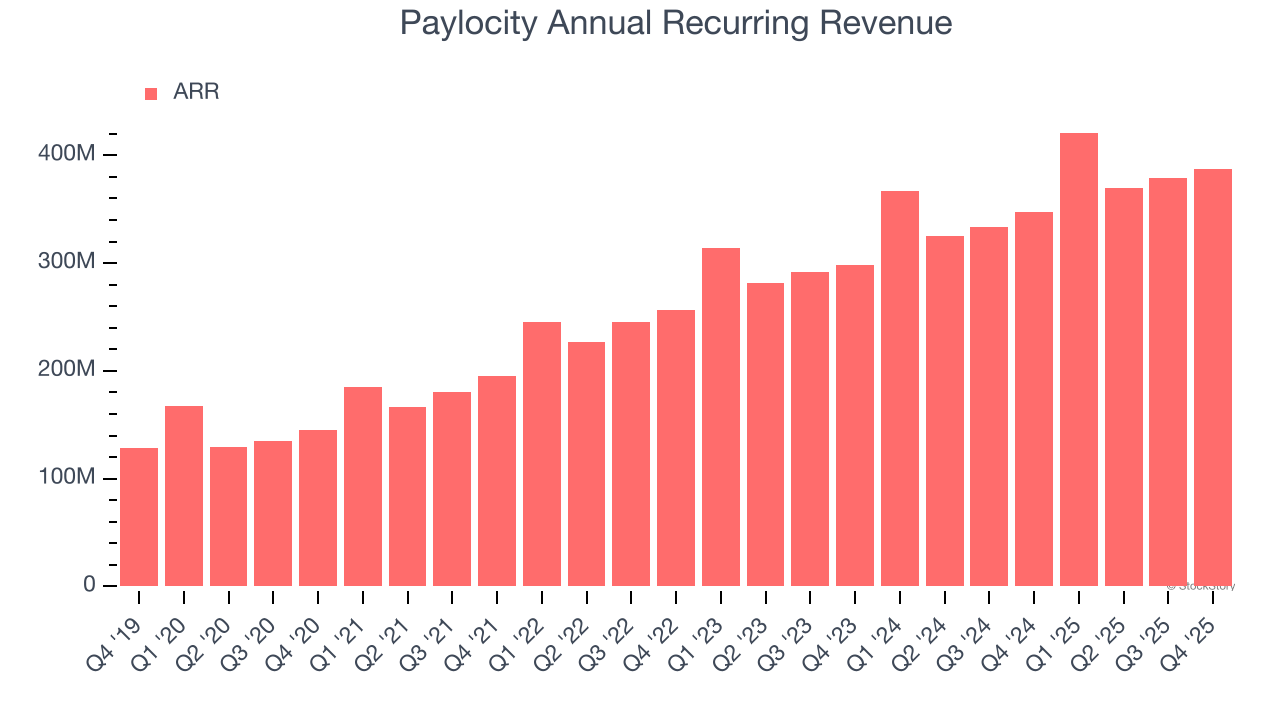

1. Weak ARR Points to Soft Demand

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Paylocity’s ARR came in at $387 million in Q4, and over the last four quarters, its year-on-year growth averaged 13.4%. This performance slightly lagged the sector and suggests that increasing competition is causing challenges in securing longer-term commitments.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Paylocity’s revenue to rise by 7%, a deceleration versus its 23.5% annualized growth for the past five years. This projection doesn't excite us and implies its products and services will face some demand challenges.

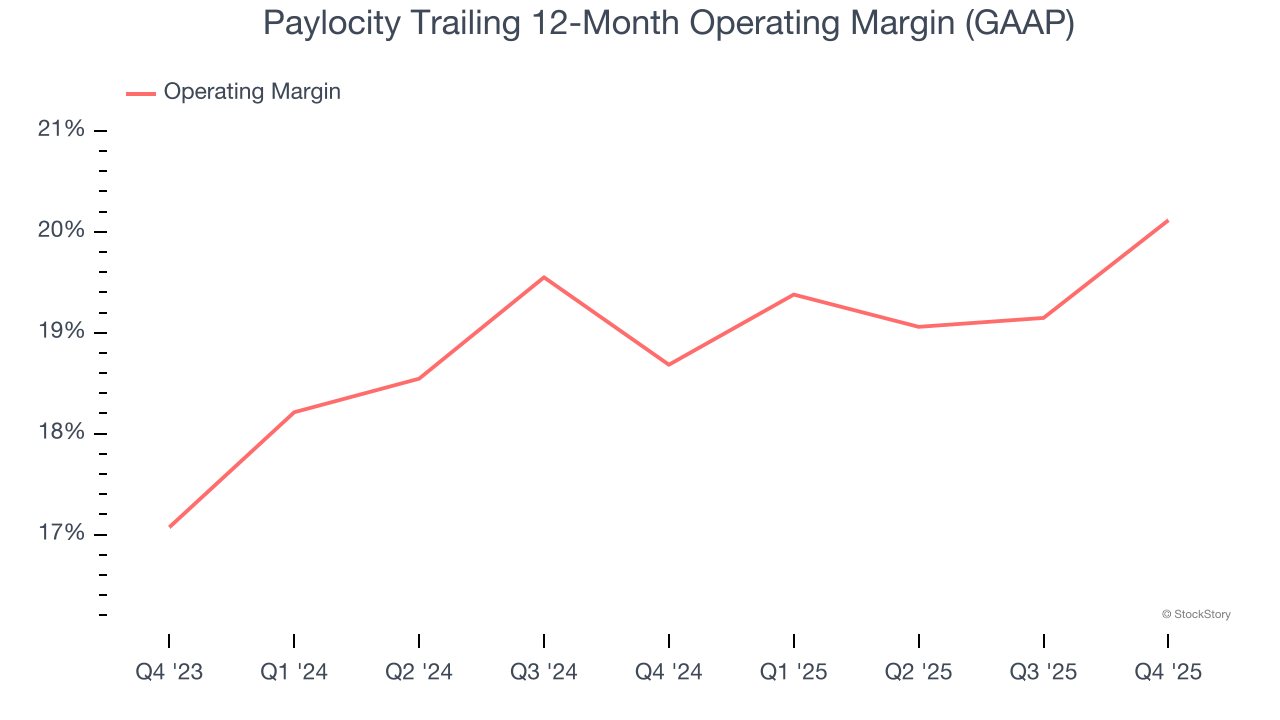

3. Operating Margin Rising, Profits Up

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Looking at the trend in its profitability, Paylocity’s operating margin rose by 1.4 percentage points over the last two years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 20.1%.

Final Judgment

Paylocity’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 3× forward price-to-sales (or $100.30 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.