Shareholders of Enphase would probably like to forget the past six months even happened. The stock dropped 48.1% and now trades at $37.90. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Enphase, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Enphase Not Exciting?

Despite the more favorable entry price, we're swiping left on Enphase for now. Here are three reasons why ENPH doesn't excite us and a stock we'd rather own.

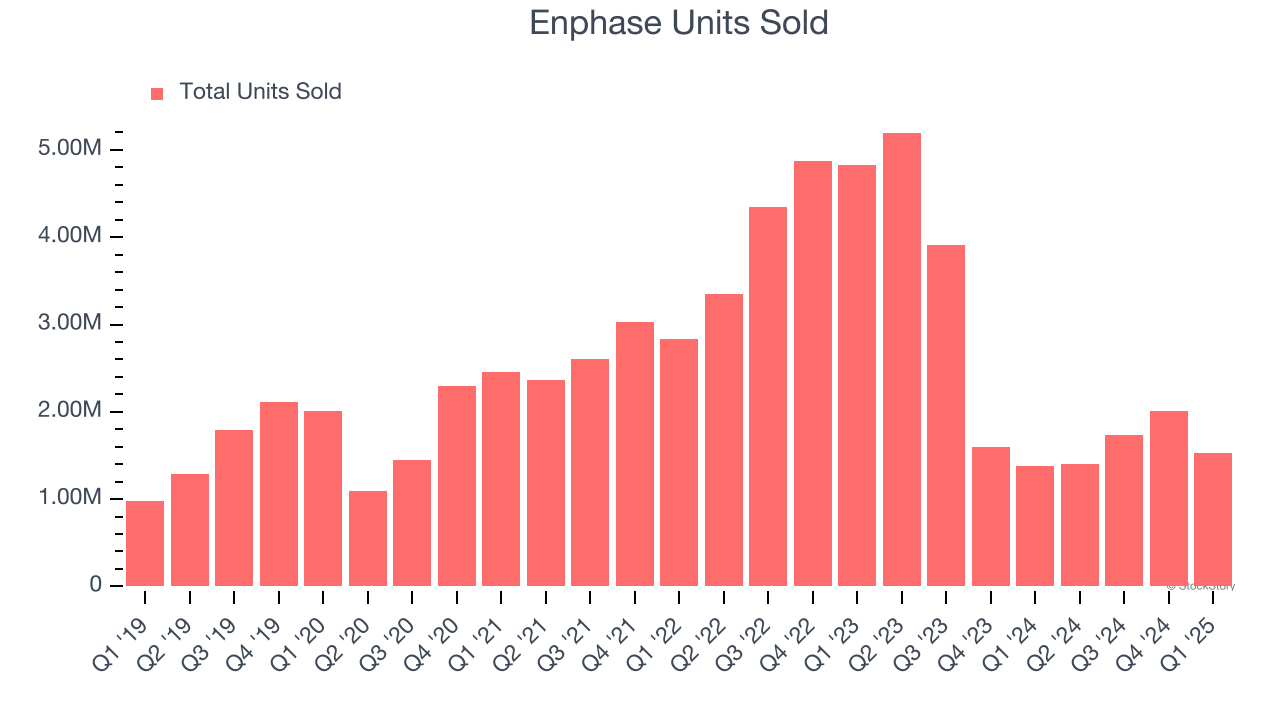

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Renewable Energy company because there’s a ceiling to what customers will pay.

Enphase’s units sold came in at 1.53 million in the latest quarter, and they averaged 23.2% year-on-year declines over the last two years. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Enphase might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

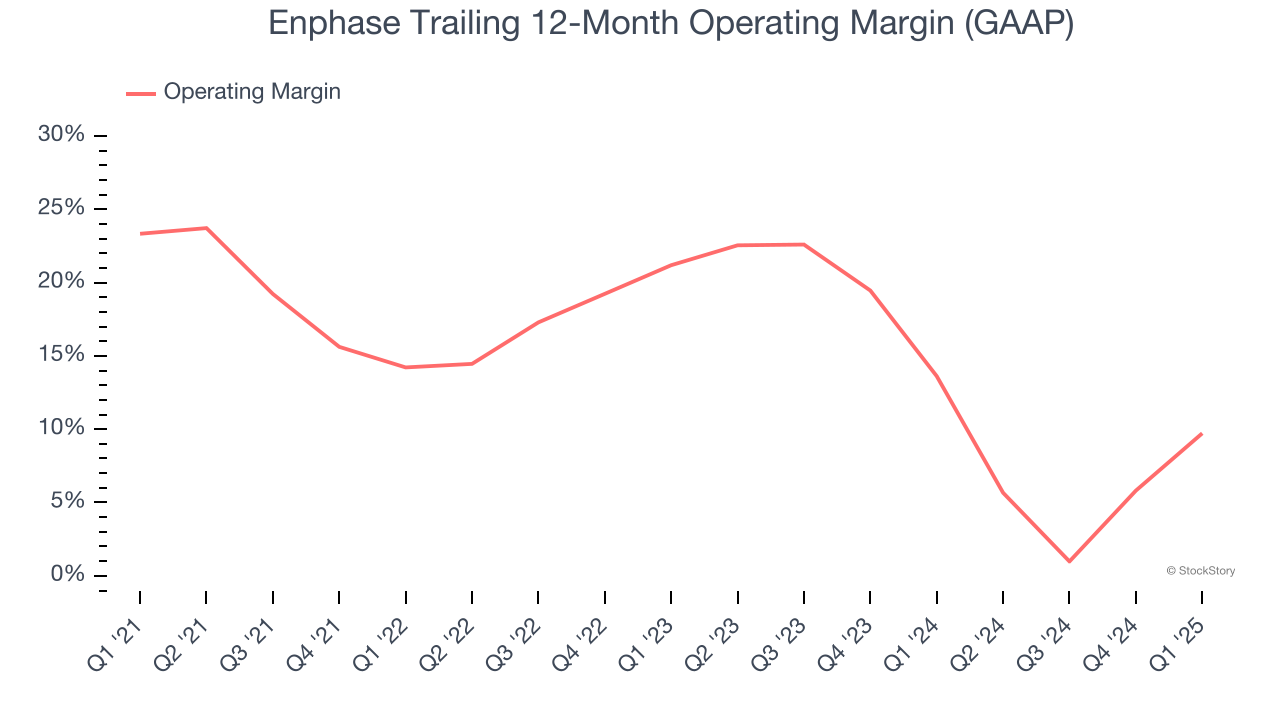

2. Shrinking Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, Enphase’s operating margin decreased by 13.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its operating margin for the trailing 12 months was 9.7%.

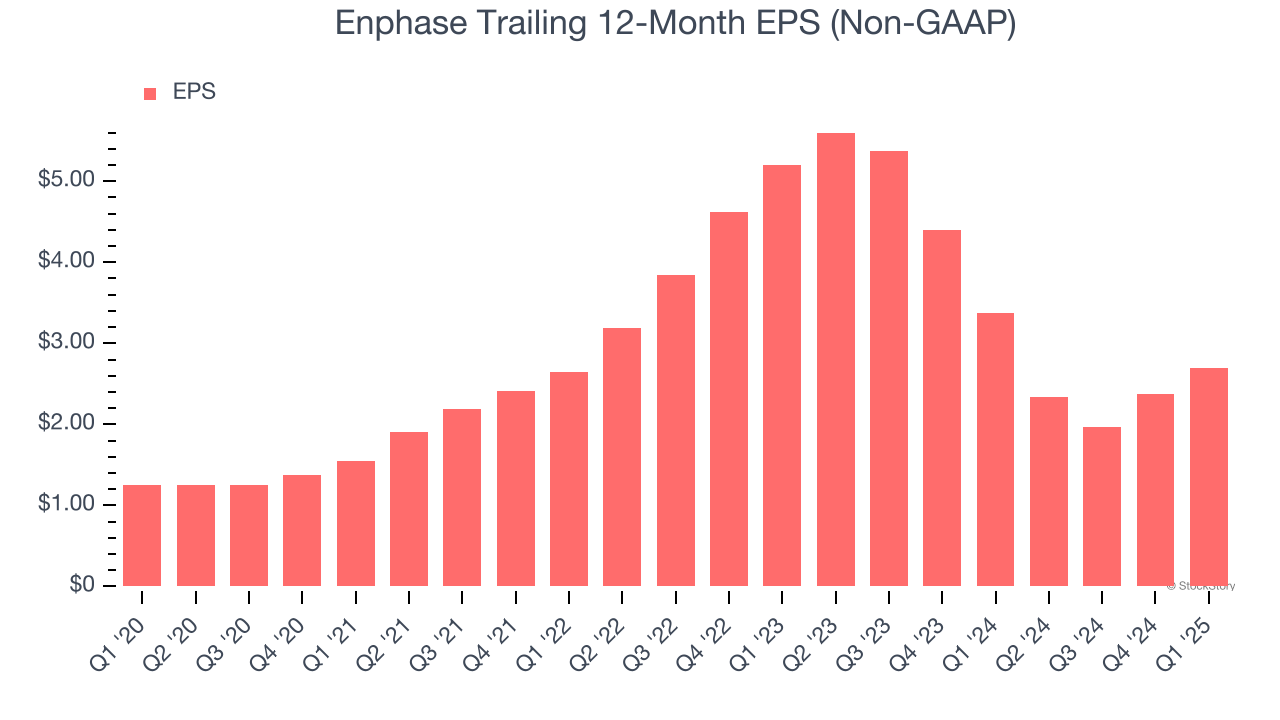

3. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Enphase, its EPS and revenue declined by 27.9% and 26.2% annually over the last two years. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Enphase’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

Enphase’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 11.5× forward P/E (or $37.90 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Would Buy Instead of Enphase

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.