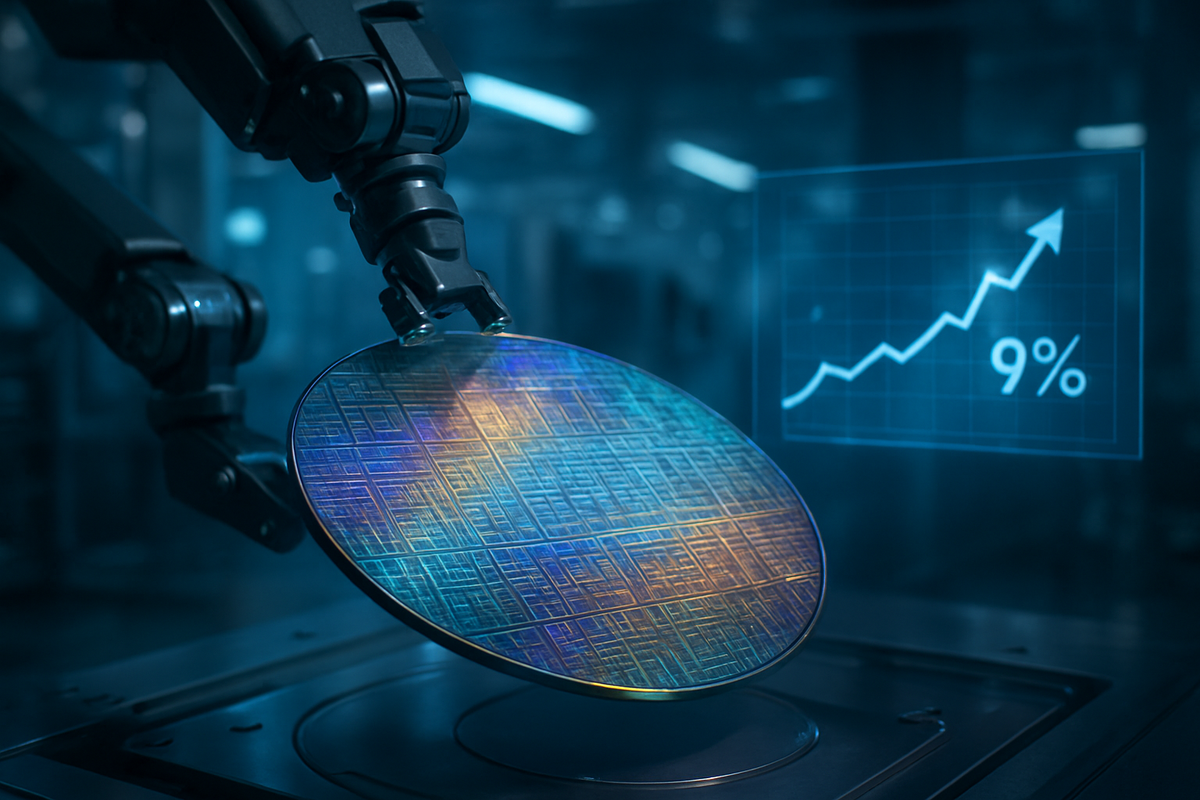

As of mid-January 2026, the semiconductor landscape has undergone a seismic shift, with Intel Corporation (NASDAQ: INTC) reclaiming its status as a cornerstone of the global technology market. Shares of the Santa Clara-based giant surged over 9% on Wednesday, January 14, 2026, pushing the stock to a two-year high of approximately $47.27. This rally follows a cascade of bullish news, most notably a landmark design win with Apple Inc. (NASDAQ: AAPL) and an aggressive upgrade from KeyBanc Capital Markets, which signals that Intel’s multi-year "IDM 2.0" turnaround strategy has finally reached its inflection point.

The market's renewed enthusiasm stems from a combination of technical mastery and geopolitical positioning. Intel’s proprietary 18A (1.8nm-class) manufacturing process has officially transitioned into high-volume production, boasting yields that have surpassed the critical 60% threshold. For investors, the most significant catalyst is the confirmation that Apple has qualified Intel’s 18A process for its future M-series chips, which power the MacBook and iPad lineups. This move marks the first time in nearly two decades that Apple has turned to Intel for primary silicon fabrication, effectively ending Taiwan Semiconductor Manufacturing Company's (NYSE: TSM) absolute monopoly over Apple’s high-end chip production.

The KeyBanc Catalyst and the 18A Manufacturing Milestone

The immediate trigger for the January 14th surge was a comprehensive research note from KeyBanc Capital Markets. Analyst John Vinh upgraded Intel to "Overweight" with a $60 price target, suggesting a potential 35% upside from current levels. Vinh’s report highlighted that Intel’s server CPU capacity for the fiscal year 2026 is already "largely sold out" as hyperscalers such as Meta Platforms (NASDAQ: META) and Alphabet Inc. (NASDAQ: GOOGL) scramble to secure silicon for AI inference workloads. The report further suggested that Intel is positioned to raise average selling prices (ASPs) by as much as 15% in the coming quarters due to this unprecedented demand.

This pricing power is a direct result of the success of the 18A node. At the Consumer Electronics Show (CES) earlier this month, Intel showcased its "Panther Lake" processors, the first consumer chips built on the 18A process. These chips utilize "RibbonFET" gate-all-around transistors and "PowerVia" backside power delivery—technologies that have allowed Intel to leapfrog competitors in power efficiency. While Samsung Electronics (OTC:SSNLF) has struggled to stabilize its 2nm yields, Intel’s 18A is now operational at scale in its state-of-the-art Fab 52 facility in Arizona, providing a stable, high-yield alternative for fabless semiconductor firms.

Winners, Losers, and the 'Whale' Win Strategy

The Apple design win is being characterized by industry insiders as the "foundry win of the decade." While the partnership will initially focus on lower-end M-series processors for Macs and iPads starting in 2027, the move signals a strategic shift for Apple. By diversifying away from TSMC, Apple is creating a "geopolitical hedge" against supply chain disruptions in the Pacific. Intel stands as the primary beneficiary, gaining a "whale" customer that validates its foundry business model and provides a multi-billion dollar revenue stream through the end of the decade.

Conversely, the news has cast a shadow over TSMC. While TSMC remains the leader in absolute volume and cutting-edge 2nm nodes, the loss of exclusivity with its largest customer, Apple, is a psychological and financial blow. Other potential "losers" include Advanced Micro Devices (NASDAQ: AMD) and NVIDIA Corporation (NASDAQ: NVDA), who now face a rejuvenated Intel that is not only designing competitive chips but also controlling the manufacturing means to produce them. However, Intel’s success as a US-based foundry could eventually benefit these rivals if they choose to utilize Intel's domestic capacity to meet "Made in America" regulatory requirements.

A New Era of US-Based Manufacturing and Geopolitical Strategy

Intel’s resurgence is deeply intertwined with broader industry trends toward localized supply chains. As the premier "national champion" for US semiconductor manufacturing, Intel has utilized billions in funding from the CHIPS and Science Act to build out its domestic infrastructure. This event marks a departure from the historical precedent of the last 20 years, where manufacturing was increasingly outsourced to East Asia. The 2026 landscape is one where "geopolitical safety" is priced at a premium, and Intel is the only company capable of offering leading-edge logic manufacturing on American soil.

The ripple effects are already being felt across the industry. Intel’s separation of its "Intel Foundry" and "Intel Products" divisions has successfully convinced external customers that their intellectual property will be protected. This structural change was essential for landing Apple and is now attracting interest from other tech giants who are eager to reduce their reliance on a single geographic point of failure. The technical success of the 18A node essentially proves that Intel can still innovate at the bleeding edge, a feat that many analysts doubted just three years ago.

What Lies Ahead: The Roadmap to 14A and Beyond

Looking forward, the short-term focus for Intel will be the seamless execution of the 18A ramp-up. Any manufacturing hiccups could jeopardize the Apple contract, making yield consistency the most watched metric for the remainder of 2026. Long-term, Intel is already pivoting toward its 14A node, which is expected to enter pilot production by 2028. Negotiations are reportedly underway for Intel to manufacture entry-level A-series chips for the iPhone by 2029, a move that would represent a total realignment of the mobile processor market.

The primary challenge for Intel will be managing the capital expenditures required to maintain this momentum. While the $60 price target from KeyBanc reflects optimism, Intel must continue to balance its massive infrastructure investments with the need for margin expansion. If Intel can successfully transition from being a legacy CPU manufacturer to a dominant global foundry, it will likely see its valuation multiples move closer to those of high-growth technology platforms rather than traditional hardware firms.

Closing Thoughts for Investors

Intel's 9% stock surge in January 2026 is more than a mere price fluctuation; it is a signal that the "Silicon Renaissance" is well underway. The combination of a major design win with Apple and the high-volume success of the 18A node has effectively silenced critics who argued that Intel’s best days were behind it. As the company cements its role as the lead US-based foundry, it is positioning itself as an indispensable utility for the AI era and a critical asset for national security.

Investors should closely monitor Intel’s quarterly yield reports and any further announcements regarding "whale" customers for its 18A and 14A nodes. While the semiconductor industry remains notoriously cyclical, Intel’s shift toward a foundry model provides a more diversified revenue base that could offer stability in volatile markets. The next six months will be a test of Intel’s operational discipline, but for now, the company has reclaimed its position as a vanguard of American innovation.

This content is intended for informational purposes only and is not financial advice.