Unlike the Magnificent 7 and artificial intelligence stocks, these losers barely make headlines. Because they don’t deserve to. Not in a positive sense, anyway.

The S&P 500 Index ($SPX) contains a small, bruised group of companies that have shed about half their value or more in less than four months to start 2026. For the contrarian investor, a 50% drawdown is a good signal of a sale. But it depends on whether the merchandise is worth the effort.

My own approach to “deep contrarian” investing like this is to think of it very differently than the rest of my portfolio. My core assets are the ETF portfolios I talk about here, the bond ladder I love but few likely wish to mimic (bonds are boring, right?), and the stock, ETF, and option trades I make around that core.

But with the state of the equity market, and so many stocks having not kept up with the S&P 500 and the AI trade, I’m starting to sense there are at least temporary opportunities in the forgotten many. This is my first article on this broad topic of “sifting through the discount bins,” but I suspect it won’t be my last.

Four names — Fiserv (FISV), Gartner (IT), The Trade Desk (TTD), and CoStar Group (CSGP) — are each dealing with a specific break in their narrative that makes them high-risk gambles rather than simple bargains. As I see, that’s actually a much better way to be a contrarian. This is more like venture capital in public equity form.

I’m not looking to fall in love with these, though that could happen. But given how forgiving the stock market can be when it comes to buying the dip, sooner or later, I would be happy just to “date” some of the ones that are down, but not out.

Now, let’s check out this foursome, and see if any of them are worth a look. I’ll include weekly charts for all, since that will provide a bit more room for error. Because let’s face it, this group of stocks has had a lot of errors already!

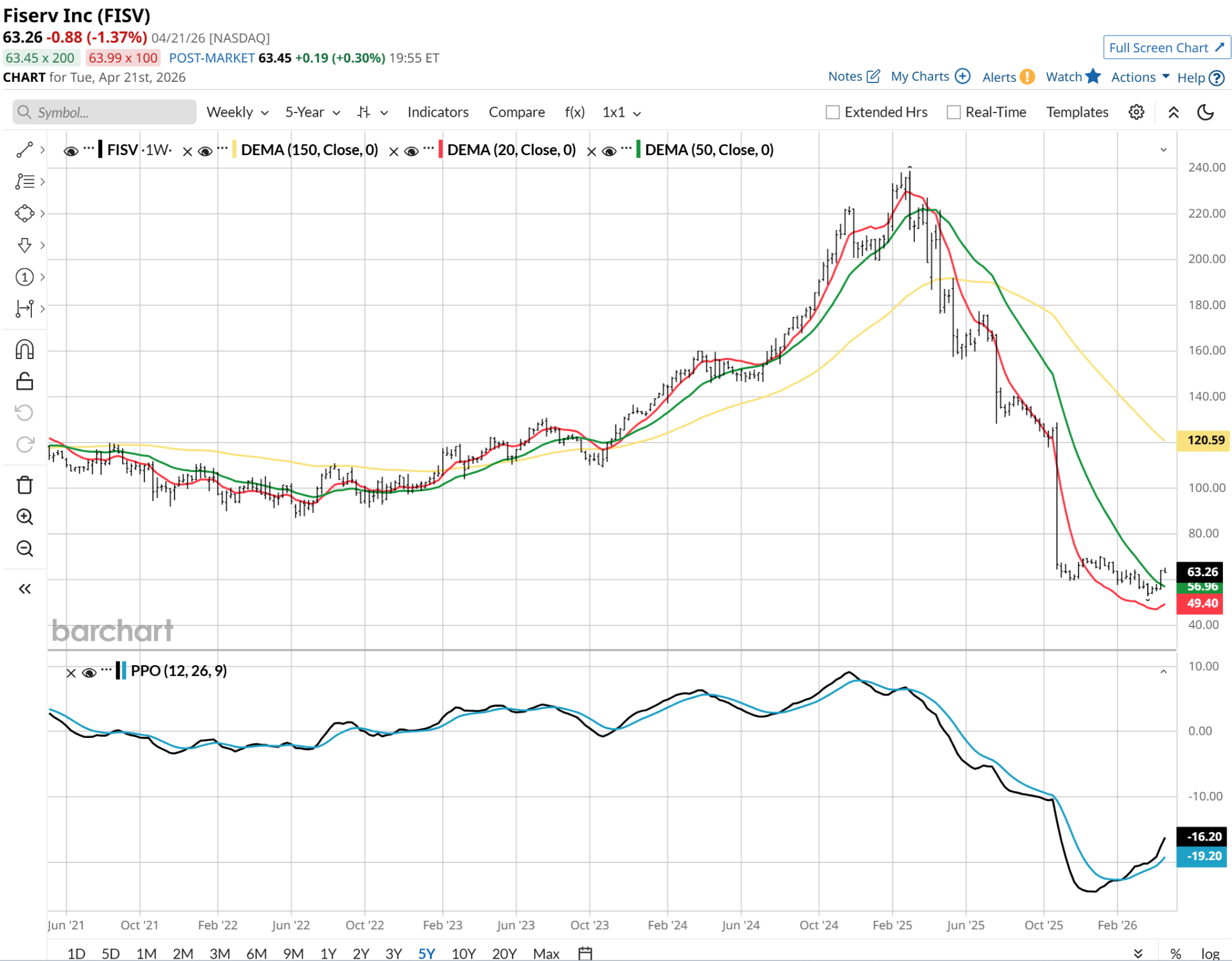

Fiserv

Fiserv is the year’s most dramatic fall from grace, sitting on a year-to-date loss of nearly 69%. The collapse began in earnest in late 2025 when the company slashed its double-digit growth guidance to mid-single digits, erasing years of investor trust in a single afternoon. Management admitted to deferring critical technology investments for years to prop up short-term margins. Now, the company has made 2026 a transition year, spending billions on a catch-up phase to modernize its Clover and payments infrastructure.

Spoiler alert: This is the one chart I like on this weekly basis. The percentage price oscillator (PPO) is at least fighting its way back. And unless this becomes a “going concern” issue, that reset year I alluded to above will eventually work itself out. Beggars can’t be choosers, and this is bottom-fishing. Or dumpster diving, if you prefer. Where “good enough” gets the nod.

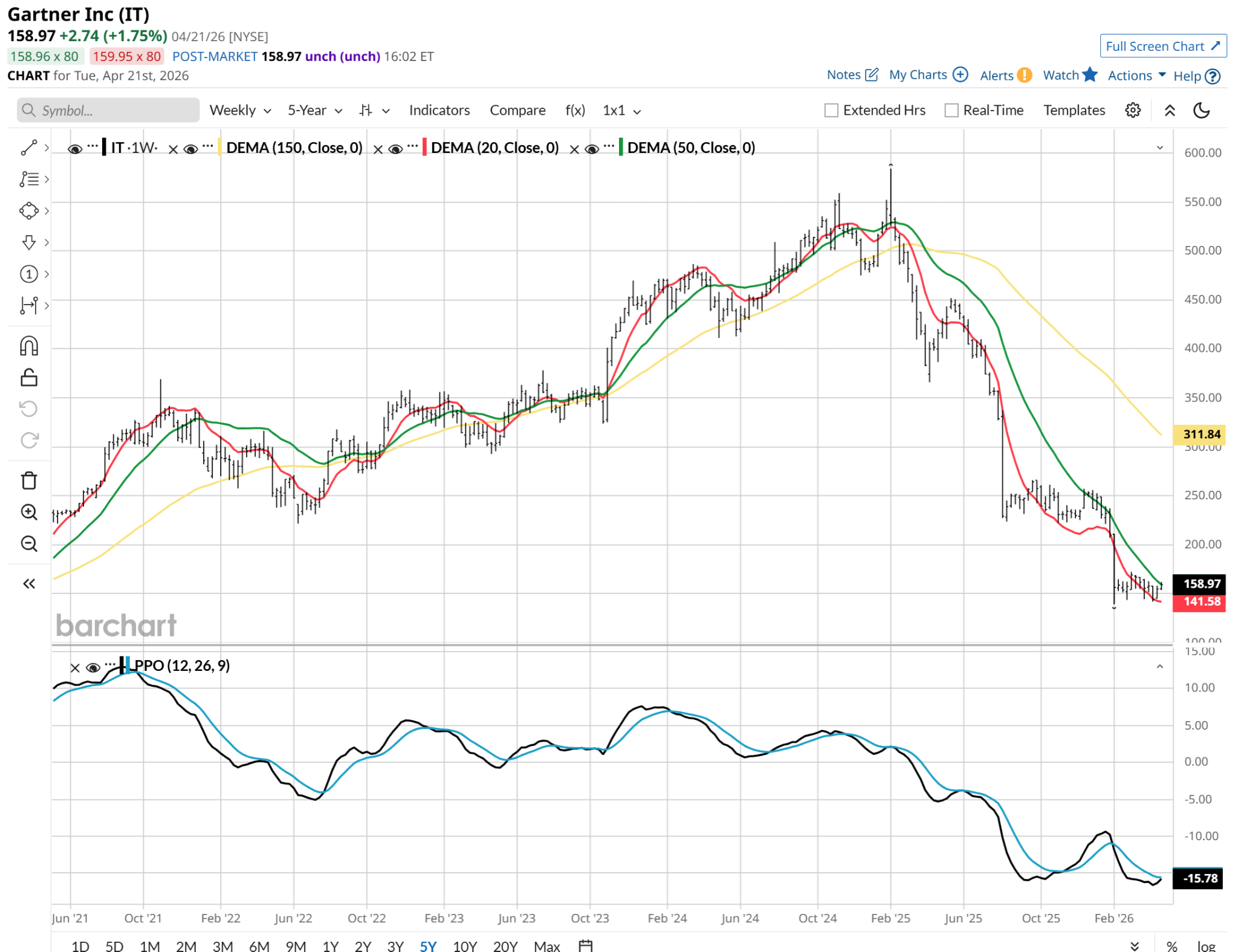

Gartner

Gartner has long been the gold standard for IT research, but it has shed over 60% of its value as the market begins to question the shelf-life of legacy consulting. Gartner recently reported that customers were “slowing and deferring everything possible” as they struggled to understand the AI landscape. Revenue missed expectations, and guidance for 2026 suggests a year-over-year earnings decline.

The chart for IT reflects a regular series of quarterly selloffs. A series of instant ratchet-down price movements. Those have taken too much out of this stock for now. Pass.

The Trade Desk

The Trade Desk was the undisputed king of the “open internet” for advertising, but a 55% six-month slide has called its dominance into question. Revenue growth has decelerated from 18% to a projected 10% for the start of 2026.

TTD is similar in chart appearance to IT. It is selling at a multi-year low now. But before it can be a good contrarian chance, I’d need to see some momentum shift.

CoStar Group

CoStar is down roughly 50% from its highs, largely due to a controversial pivot into the residential real estate market through Homes.com. Activist investors, including D.E. Shaw, have publicly criticized the company for a new reporting structure they claim “obscures” the losses at Homes.com. Management also unexpectedly stopped disclosing net new bookings for the residential business, a key metric for investors.

CSGP has not been public that long. And it is a good reminder that IPOs don’t always become high-fliers. But again, with some time, if the company gets things right internally, and the real estate market bottoms (not soon, eventually, I suspect), this one is right back on the radar screen.

Why All 4 Stocks Are Worth Watching

None of these stocks are failing because of market conditions. They are failing because their core business assumptions have been challenged. I charted these four losers, to see if any are loveable.

For now, only one (Fiserv) clears the bar. However, since these are weekly charts, all merit tracking going forward, as time has a way of healing even the deepest of wounds. And by the time the fundamental crowd is all over these again, the charts will have already signalled the start of the comeback.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Keeps Hitting It Out of the Park: Should You Buy?

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?