Dell Technologies (DELL) reported strong fourth-quarter results and capped fiscal 2026 with record financial performance, driven by accelerating demand for its artificial intelligence (AI)-optimized servers.

For the full fiscal year, Dell generated revenue of $113.5 billion, up 19% year-over-year (YoY). Earnings per share (EPS) increased 27% to $10.30. It generated $11.5 billion in adjusted free cash flow and returned $7.5 billion to shareholders, including the repurchase of 54 million shares.

Looking ahead, the company sees a substantial $50 billion AI revenue opportunity supported by a growing customer base, a strong backlog, and an expanding pipeline. These factors indicate strong growth ahead for the company as enterprises scale AI workloads and modernize data center infrastructure.

Investors responded positively to the results and outlook. Shares of DELL rose approximately 11.6% in pre-market trading and currently sit about 20% up in this morning's trading, following the earnings release, reflecting optimism around sustained AI-driven momentum and fiscal 2027 growth prospects.

The $50 Billion AI Opportunity

The AI opportunity is meaningfully growing for Dell and will support its growth in the coming quarters. In fiscal 2026, Dell generated $64.1 billion in AI orders and shipped $25.2 billion, reflecting growing demand and operational capacity. In Q4, Dell’s total revenue came in at $33.4 billion, representing 39% YoY growth, while EPS rose 45% to $3.89. The strong double-digit growth was driven by sustained demand for its AI solutions and disciplined execution.

For instance, Dell shipped $9.5 billion in AI servers and exited the period with a record $43 billion AI backlog. Importantly, the company’s sales pipeline continued to expand sequentially even after converting a substantial volume of orders, indicating durable demand rather than one-time purchasing activity.

Looking ahead, Dell booked $34.1 billion in AI orders. This level of order activity signals accelerating customer adoption and strong growth ahead. Customer diversification further strengthens its growth profile. Dell’s AI customer base now exceeds 4,000, with growth spanning neocloud providers, sovereign entities, and traditional enterprise clients. This broad-based adoption suggests that AI infrastructure spending is expanding across multiple end markets.

Looking ahead, management expects AI-driven demand to remain a key catalyst for growth. For fiscal 2027, the company projects approximately $50 billion in AI revenue, implying 100% YoY growth. Overall, Dell’s near-term revenue growth trajectory remains solid, led by significant demand for its AI offerings.

Dell: Looking Beyond the AI Opportunity

Dell continues to show strength across its broader portfolio, primarily in traditional servers, storage, and personal computers. The company is gaining market share in the PC segment and delivering solid performance within its Infrastructure Solutions Group (ISG), supported by healthy margins in its core server and storage businesses.

In the fourth quarter, demand for traditional servers significantly outpaced supply, with strong double-digit growth across all geographic regions. Demand was broad-based, with unit shipments increasing, the active buyer base expanding, and a favorable product mix shift toward higher-density, high-performance configurations. Customers increasingly adopted the company’s new generation server platforms, reflecting an upgrade cycle.

The long-term opportunity remains substantial. Dell’s installed base continues to operate on 14th-generation or older servers, creating a meaningful modernization runway. As enterprises seek improved performance, greater efficiency, and lower operating costs, this aging installed base represents a durable source of demand for the company.

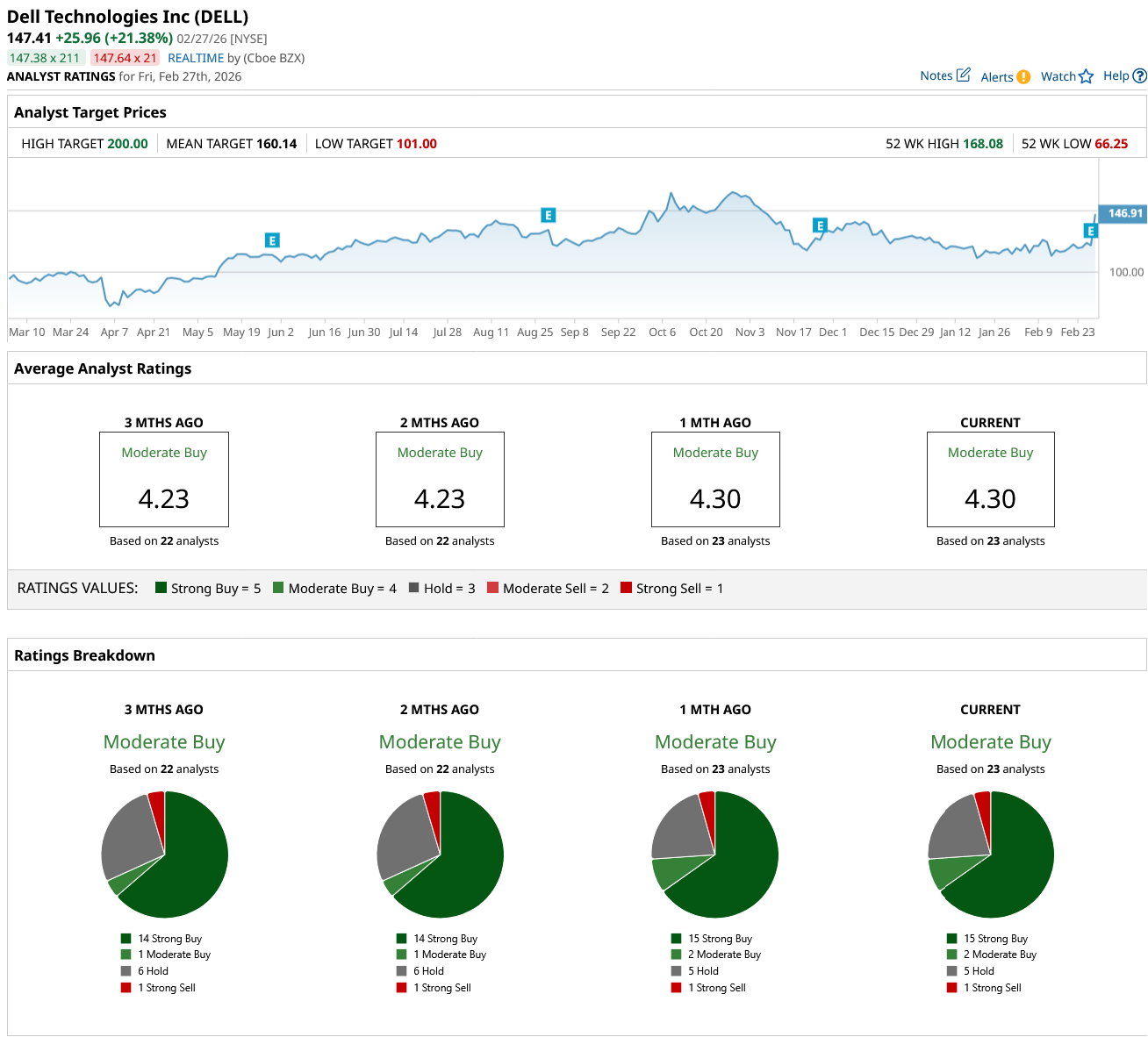

Is DELL Stock Still a Buy?

Wall Street maintains a “Moderate Buy” consensus rating on DELL stock. However, Dell is well-positioned to deliver strong growth in fiscal 2027. Dell expects revenue in the range of $138 billion to $142 billion, representing approximately 23% growth at the midpoint of $140 billion in fiscal 2027.

ISG revenue is projected to expand in the mid-40% range, driven primarily by significant growth in AI-related revenue. Within the broader infrastructure portfolio, traditional servers and storage are anticipated to increase in the mid-single digits, with growth more concentrated in traditional servers.

Dell’s adjusted EPS is projected to reach $12.90, marking an estimated 25% YoY increase despite ongoing margin considerations. Dell’s operating model remains solid. EPS growth is expected to be driven by the rapid expansion of its AI business, steady revenue growth, improving profitability across the broader portfolio, disciplined operating expense management, and incremental benefits from its share repurchase program. Overall, these factors support management’s confidence in sustained earnings expansion.

In the first quarter, revenue is forecasted between $34.7 billion and $35.7 billion, implying 51% growth at the midpoint of $35.2 billion. ISG revenue is expected to double, supported by approximately $13 billion in AI server revenue. Its adjusted EPS for the quarter is projected at $2.90, representing 87% YoY growth.

From a valuation perspective, Dell appears attractively priced relative to its projected growth trajectory. DELL stock trades at a forward price-to-earnings (P/E) multiple of 11.7, which looks compelling considering a projected EPS growth of approximately 25% in fiscal 2027. In summary, accelerating AI-driven revenue, disciplined cost management, and a compelling valuation multiple support a constructive investment outlook.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 52 Massive Vol/OI Spikes Expire March 20—Profit Plays on Top 3

- Uber Air Is Officially Here. Does That Make Uber Stock a Buy on Flying Car Dreams?

- ‘This is Not Business as Usual. This is Risk’: Michael Burry Warns Nvidia Looks Strikingly Similar to Cisco Just Prior to Dot Com Bubble Crash

- Warren Buffett Warns, ‘You Do Not Adequately Protect Yourself by Being Half Awake While Others Are Sleeping’