Over the past six months, Ocular Therapeutix’s shares (currently trading at $10.37) have posted a disappointing 18.5% loss, well below the S&P 500’s 7.8% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Ocular Therapeutix, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Ocular Therapeutix Will Underperform?

Even though the stock has become cheaper, we don’t have much confidence in Ocular Therapeutix. Here are three reasons we avoid OCUL, plus one stock we’d rather own.

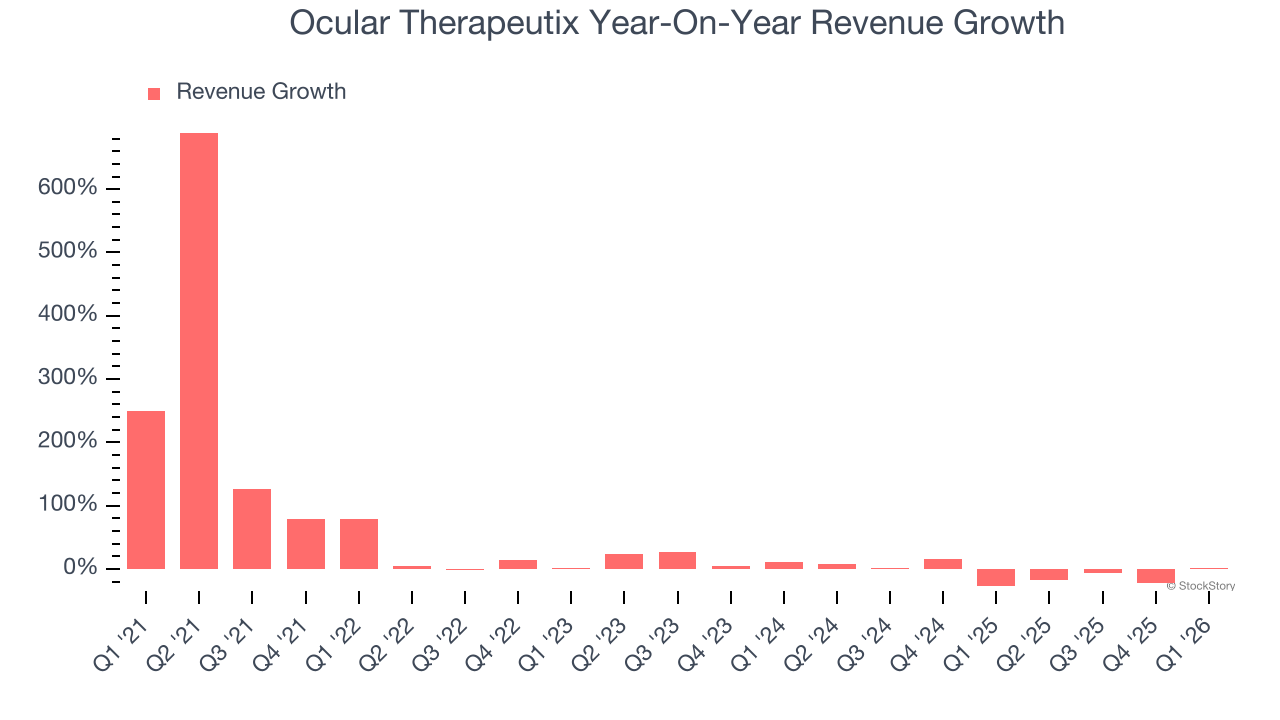

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. Ocular Therapeutix’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.7% over the last two years.

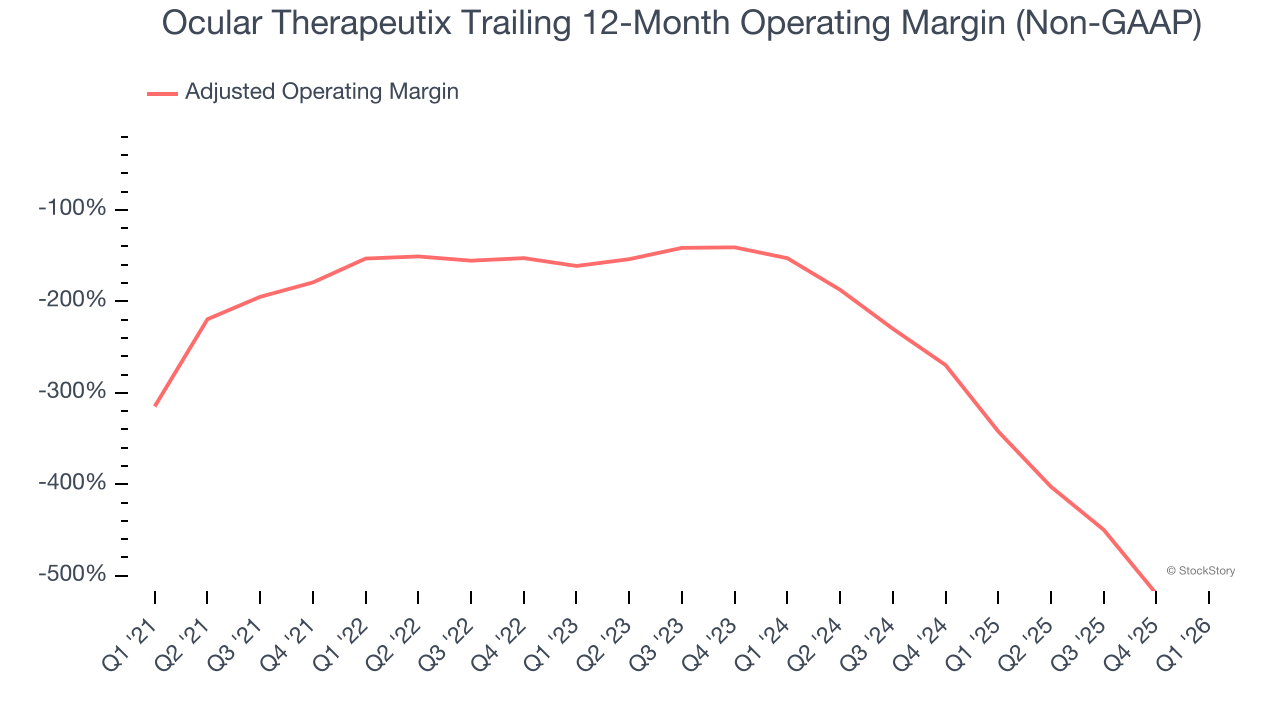

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Analyzing the trend in its profitability, Ocular Therapeutix’s adjusted operating margin decreased significantly over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Ocular Therapeutix’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its adjusted operating margin for the trailing 12 months was negative 575%.

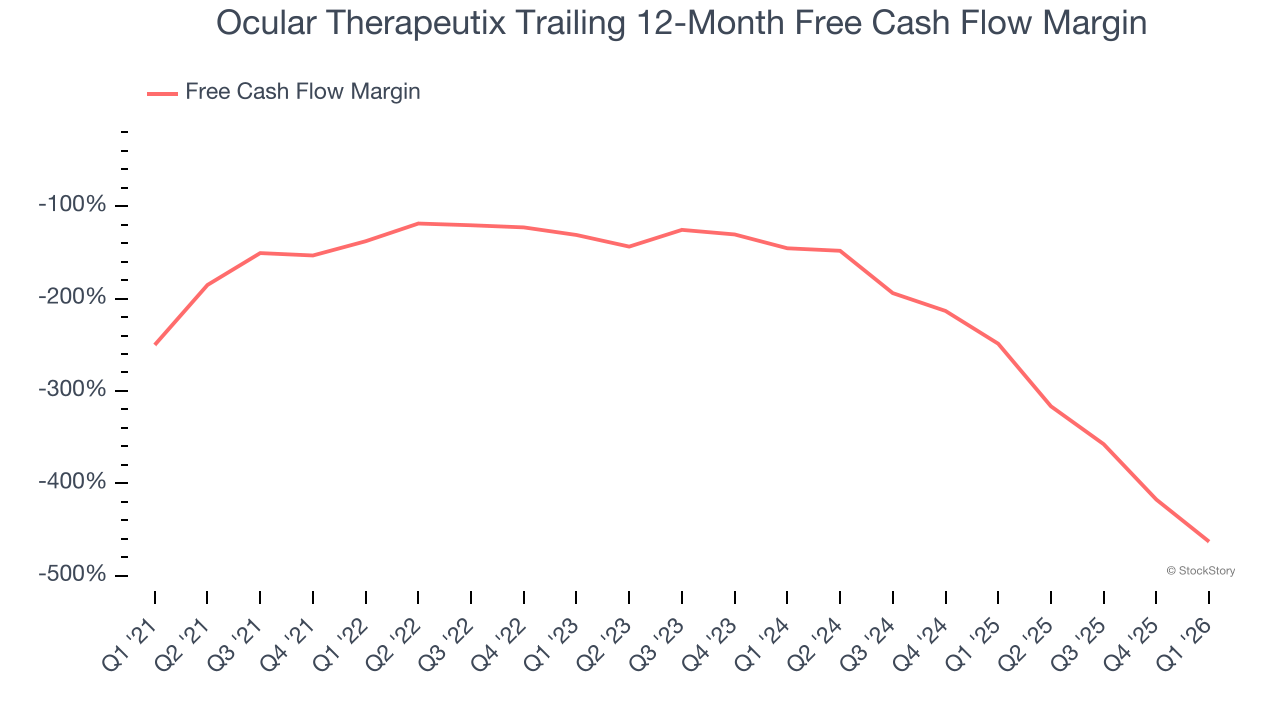

3. Free Cash Flow Margin Dropping

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Ocular Therapeutix’s margin dropped meaningfully over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s in the middle of a big investment cycle. Ocular Therapeutix’s free cash flow margin for the trailing 12 months was negative 463%.

Final Judgment

Ocular Therapeutix falls short of our quality standards. Following the recent decline, the stock trades at $10.37 per share (or a forward price-to-sales ratio of 42.4×). The market typically values companies like Ocular Therapeutix based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.