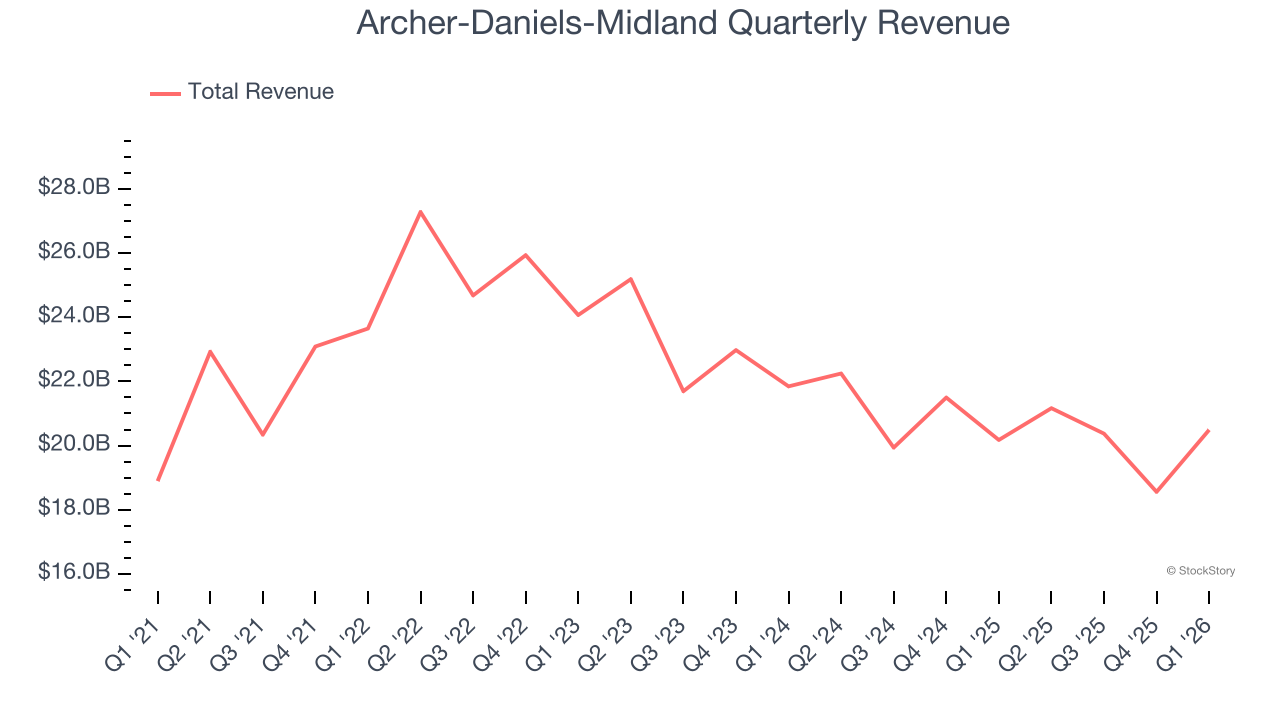

Agricultural supply chain giant Archer-Daniels-Midland (NYSE: ADM) fell short of the market’s revenue expectations in Q1 CY2026 as sales only rose 1.6% year on year to $20.49 billion. Its non-GAAP profit of $0.71 per share was 7.8% above analysts’ consensus estimates.

Is now the time to buy Archer-Daniels-Midland? Find out by accessing our full research report, it’s free.

Archer-Daniels-Midland (ADM) Q1 CY2026 Highlights:

- Revenue: $20.49 billion vs analyst estimates of $20.74 billion (1.6% year-on-year growth, 1.2% miss)

- Adjusted EPS: $0.71 vs analyst estimates of $0.66 (7.8% beat)

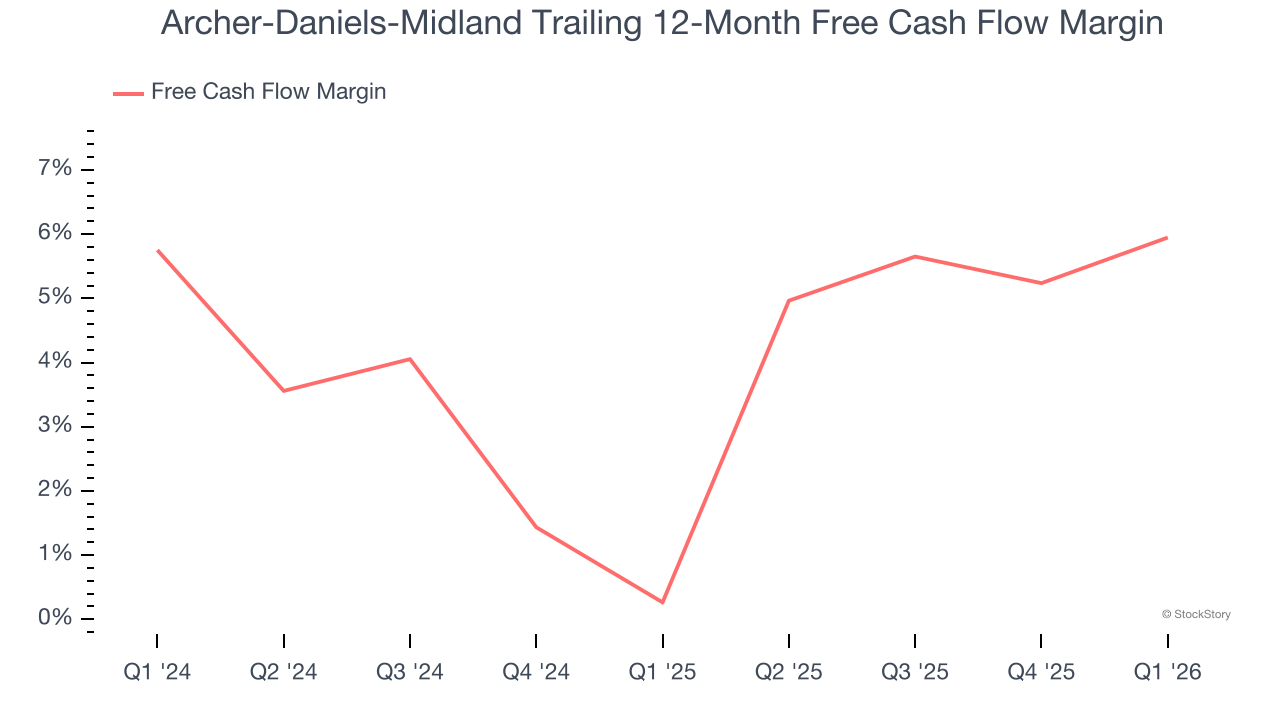

- Free Cash Flow was -$44 million compared to -$633 million in the same quarter last year

- Market Capitalization: $36.75 billion

"Within a dynamic global landscape, ADM delivered robust operating performance in the first quarter, with our crushing and ethanol businesses capitalizing on a constructive biofuels environment and our Nutrition business benefiting from higher Flavors sales, the ongoing Decatur East plant recovery, and continued improvements in Animal Nutrition. With U.S. biofuels policy clarity now providing a stable regulatory framework, combined with our team’s solid execution, we are raising our earnings expectations for 2026," said Juan Luciano, Chair of the Board and CEO.

Company Overview

Transforming crops from the world's most productive agricultural regions into everyday essentials, Archer-Daniels-Midland (NYSE: ADM) processes and transports agricultural commodities like grains and oilseeds while manufacturing ingredients for food, beverages, feed, and industrial applications.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $80.58 billion in revenue over the past 12 months, Archer-Daniels-Midland is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To expand meaningfully, Archer-Daniels-Midland likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Archer-Daniels-Midland struggled to generate demand over the last three years. Its sales dropped by 7.5% annually, a tough starting point for our analysis.

This quarter, Archer-Daniels-Midland’s revenue grew by 1.6% year on year to $20.49 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, an acceleration versus the last three years. This projection is above average for the sector and suggests its newer products will catalyze better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Archer-Daniels-Midland has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3%, below what we’d expect for a consumer staples business.

Taking a step back, an encouraging sign is that Archer-Daniels-Midland’s margin expanded by 5.7 percentage points over the last year. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Archer-Daniels-Midland broke even from a free cash flow perspective in Q1. This result was good as its margin was 2.9 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Archer-Daniels-Midland’s Q1 Results

It was good to see Archer-Daniels-Midland beat analysts’ EPS expectations this quarter. On the other hand, its gross margin missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter was mixed. The stock traded up 1.6% to $77.49 immediately after reporting.

Big picture, is Archer-Daniels-Midland a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).