Since November 2025, The Ensign Group has been in a holding pattern, posting a small return of 1% while floating around $179.25. The stock also fell short of the S&P 500’s 11.5% gain during that period.

Given the weaker price action, is now a good time to buy ENSG? Or should investors expect a bumpy road ahead? Find out in our full research report, it’s free.

Why Does The Ensign Group Spark Debate?

Founded in 1999 and named after a naval term for a flag-bearing ship, The Ensign Group (NASDAQ: ENSG) operates skilled nursing facilities, senior living communities, and rehabilitation services across 15 states, primarily serving high-acuity patients recovering from various medical conditions.

Two Things to Like:

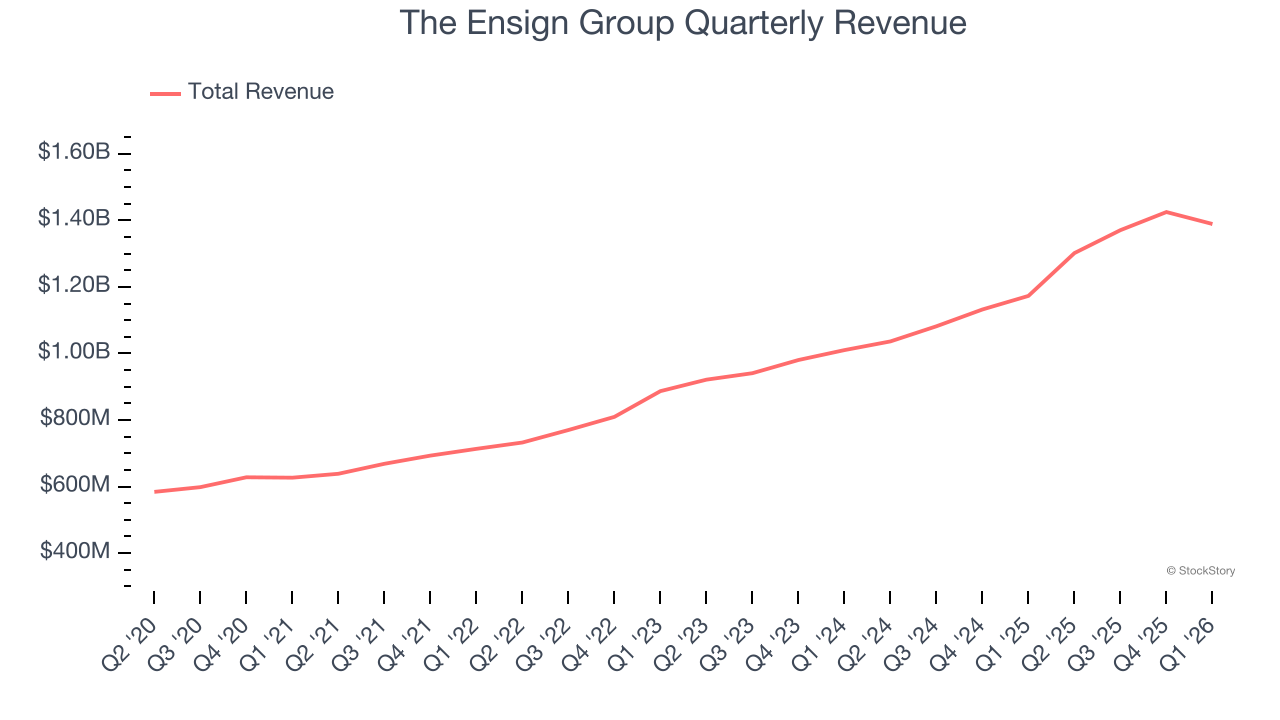

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, The Ensign Group’s sales grew at an impressive 17.6% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

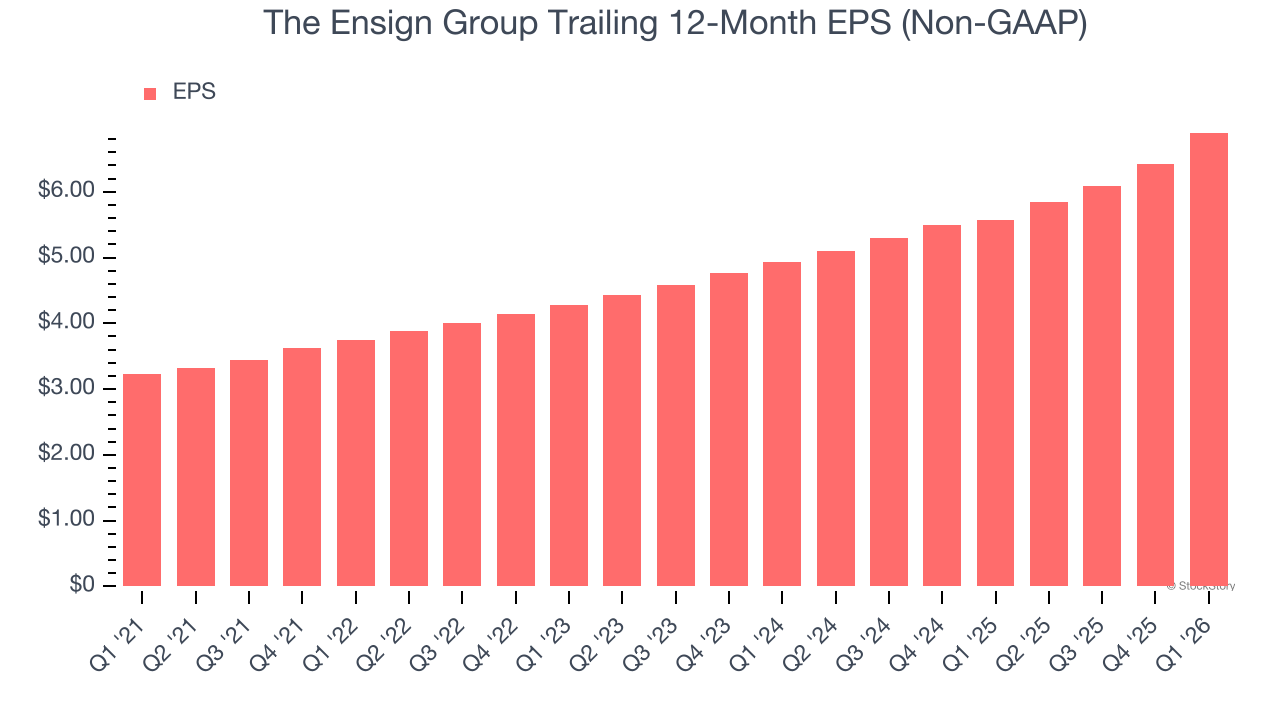

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

The Ensign Group’s astounding 16.4% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

One Reason to be Careful:

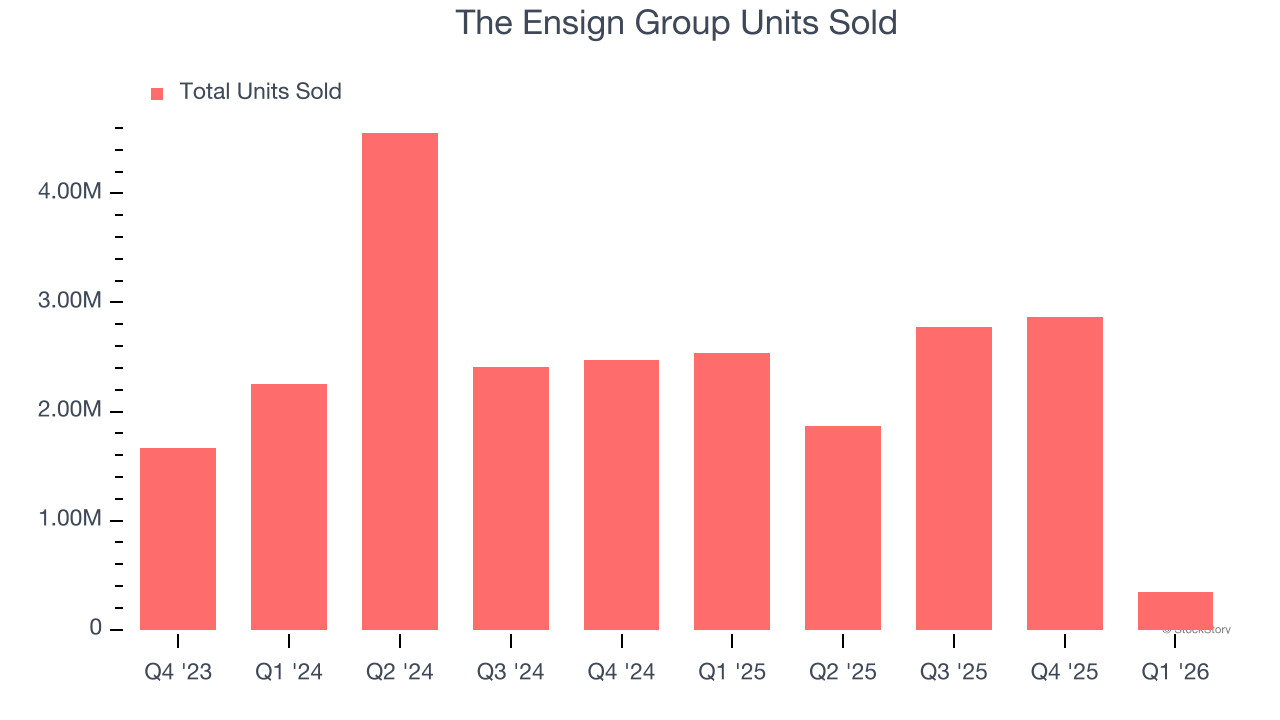

Demand Slips as Sales Volumes Slide

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Specialized Medical & Nursing Services company because there’s a ceiling to what customers will pay.

The Ensign Group’s units sold came in at 348,389 in the latest quarter, and they averaged 8.9% year-on-year declines over the last two years. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests The Ensign Group might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

Final Judgment

The Ensign Group’s merits more than compensate for its flaws. With its shares lagging the market recently, the stock trades at 22.9× forward P/E (or $179.25 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.