Over the past six months, Cars.com’s shares (currently trading at $9.09) have posted a disappointing 14.9% loss while the S&P 500 was down 1.8%. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Cars.com, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Cars.com Not Exciting?

Even though the stock has become cheaper, we're cautious about Cars.com. Here are three reasons we avoid CARS and a stock we'd rather own.

1. Change in Dealer Customers Points to Soft Demand

As an online marketplace, Cars.com generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, Cars.com’s dealer customers, a key performance metric for the company, increased by 1% annually to 19,544 in the latest quarter. This growth rate is one of the lowest in the consumer internet sector. If Cars.com wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Cars.com’s revenue to rise by 1.1%. This projection doesn't excite us and suggests its products and services will face some demand challenges.

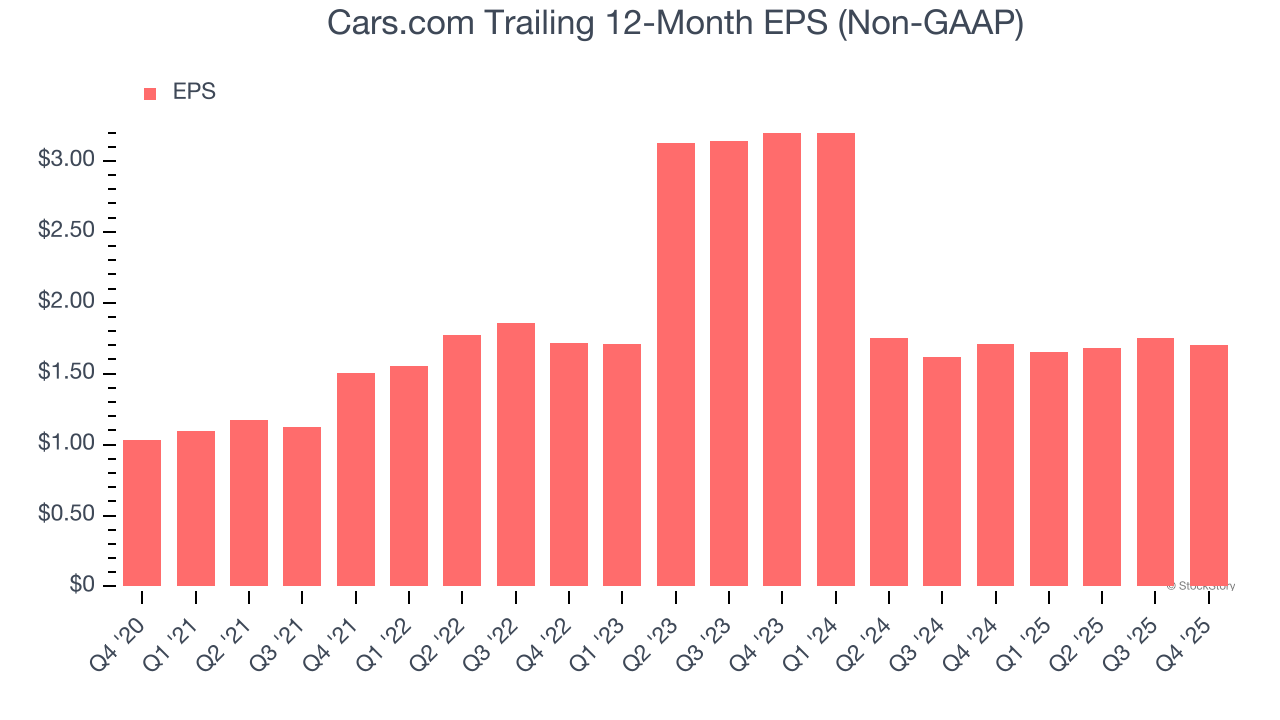

3. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Cars.com’s flat EPS over the last three years was below its 3.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Cars.com’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 4.6× forward EV/EBITDA (or $9.09 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d suggest looking at one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.