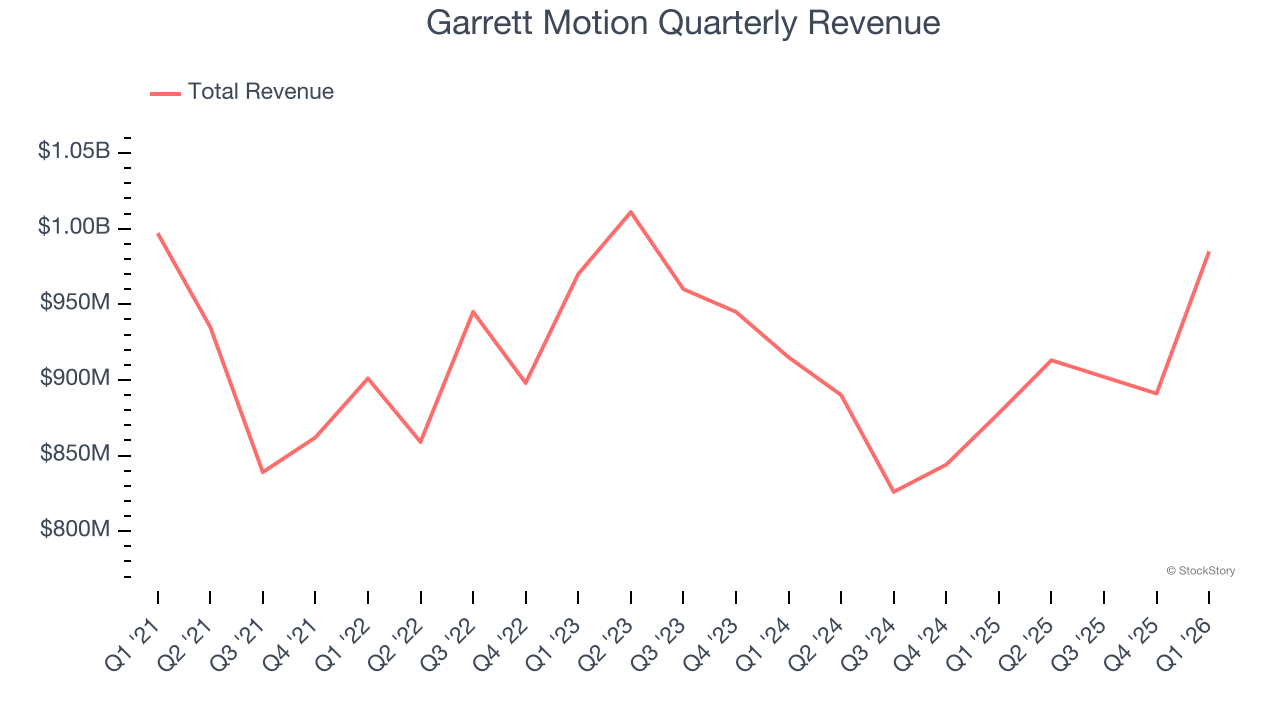

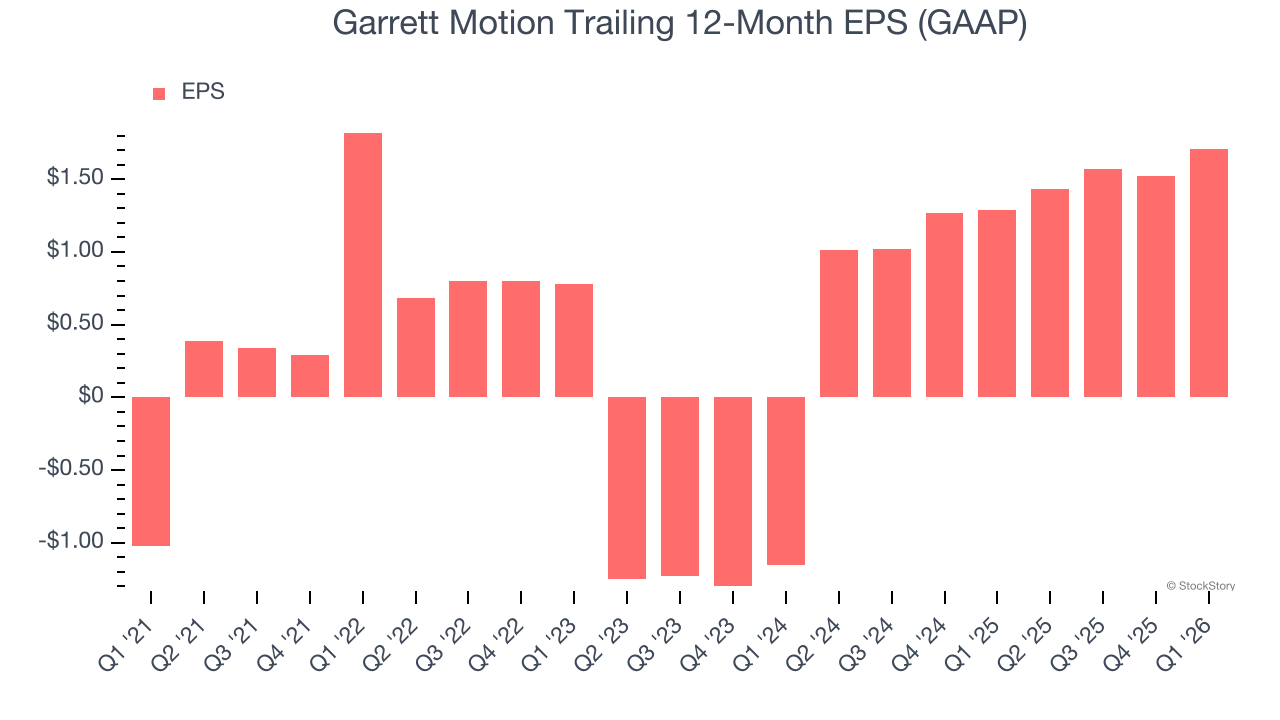

Turbocharger technology company Garrett Motion (NYSE: GTX) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 12.2% year on year to $985 million. The company’s full-year revenue guidance of $3.75 billion at the midpoint came in 1.8% above analysts’ estimates. Its GAAP profit of $0.49 per share was 19.3% above analysts’ consensus estimates.

Is now the time to buy Garrett Motion? Find out by accessing our full research report, it’s free.

Garrett Motion (GTX) Q1 CY2026 Highlights:

- Revenue: $985 million vs analyst estimates of $901.2 million (12.2% year-on-year growth, 9.3% beat)

- EPS (GAAP): $0.49 vs analyst estimates of $0.41 (19.3% beat)

- Adjusted EBITDA: $183 million vs analyst estimates of $164.7 million (18.6% margin, 11.1% beat)

- The company lifted its revenue guidance for the full year to $3.75 billion at the midpoint from $3.7 billion, a 1.4% increase

- EBITDA guidance for the full year is $687 million at the midpoint, above analyst estimates of $669.8 million

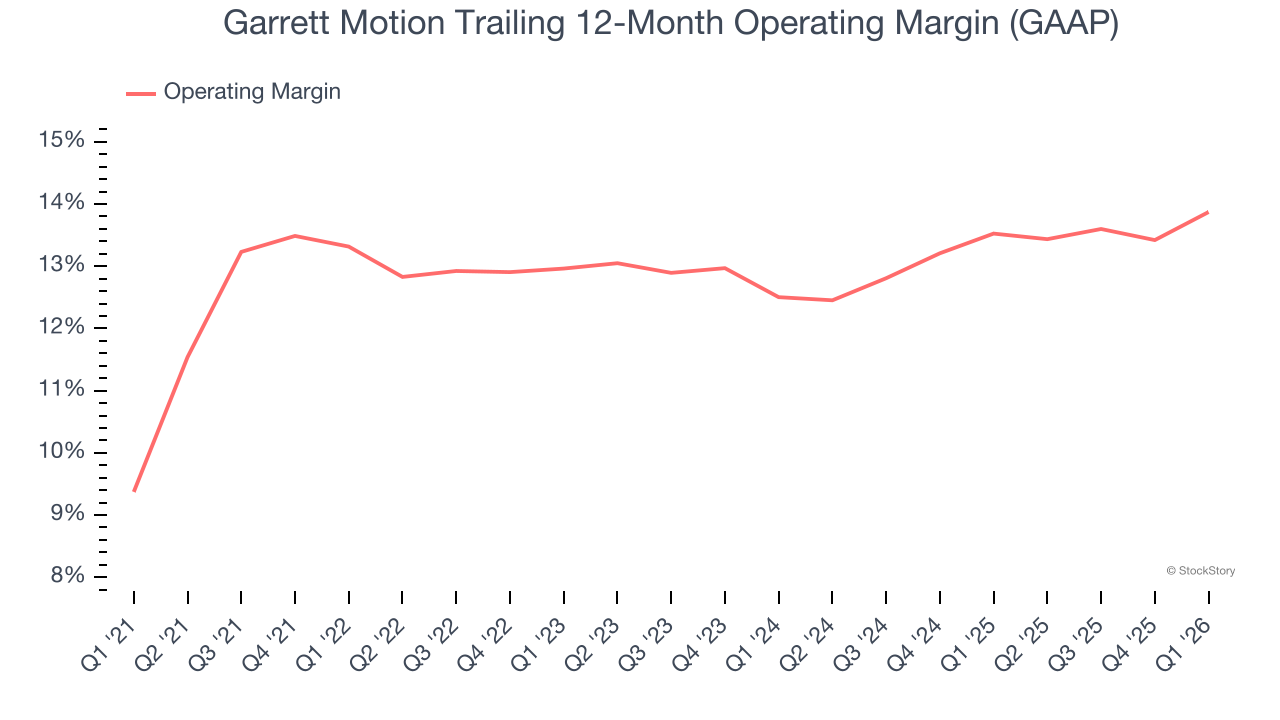

- Operating Margin: 14.6%, up from 12.9% in the same quarter last year

- Free Cash Flow Margin: 7%, up from 4.1% in the same quarter last year

- Market Capitalization: $3.85 billion

“Garrett had a strong start to 2026, delivering 6% organic growth,” said Olivier Rabiller, President and CEO of Garrett.

Company Overview

A key player in the transition to cleaner vehicles, Garrett Motion (NYSE: GTX) designs and manufactures turbochargers, air compressors, and electric motor technologies for vehicle manufacturers and industrial applications.

Revenue Growth

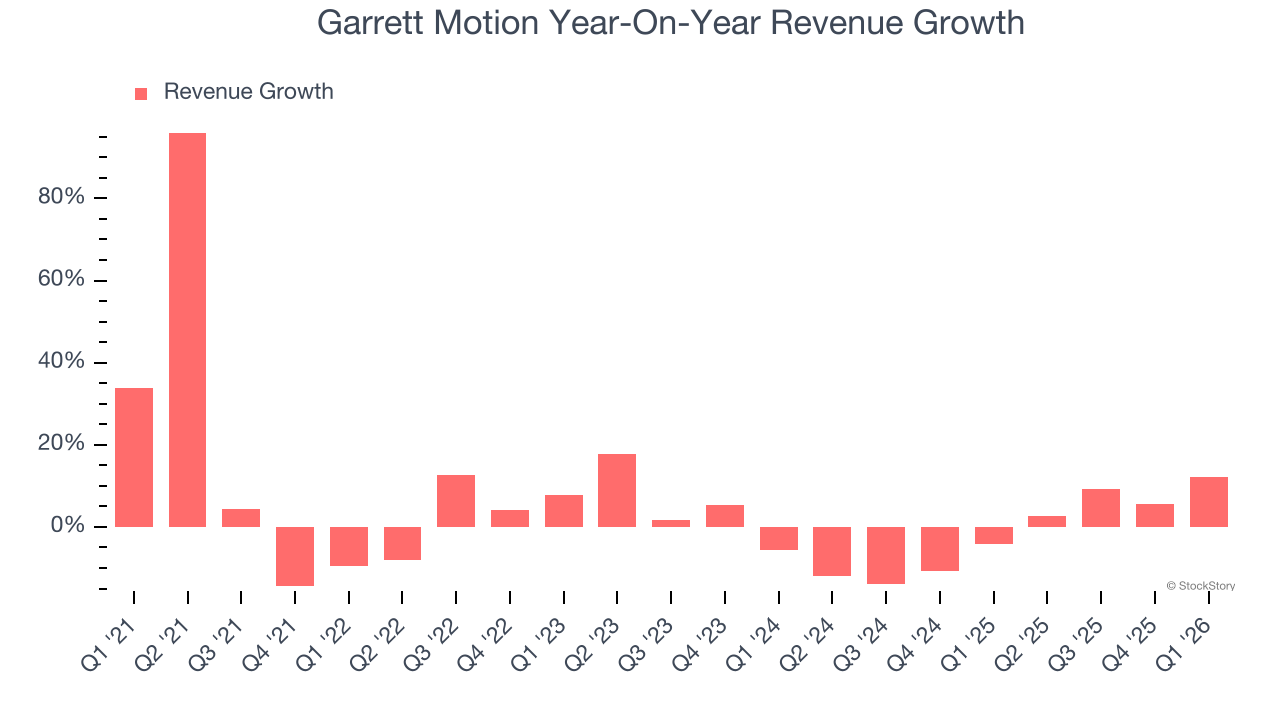

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Garrett Motion’s sales grew at a sluggish 2.4% compounded annual growth rate over the last five years. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Garrett Motion’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.8% annually.

This quarter, Garrett Motion reported year-on-year revenue growth of 12.2%, and its $985 million of revenue exceeded Wall Street’s estimates by 9.3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Garrett Motion’s operating margin has more or less stayed the same over the last 12 months , averaging 13.2% over the last five years. This profitability was top-notch for an industrials business, showing it’s an well-run company with an efficient cost structure. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Garrett Motion’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Garrett Motion generated an operating margin profit margin of 14.6%, up 1.7 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Garrett Motion’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Garrett Motion, its two-year annual EPS growth of 86.7% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Garrett Motion reported EPS of $0.49, up from $0.30 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Garrett Motion’s Q1 Results

We were impressed that Garrett Motion beat analysts’ revenue, EBITDA, and EPS expectations this quarter. We were also excited its EBITDA guidance outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 5.6% to $21.64 immediately following the results.

Garrett Motion had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).