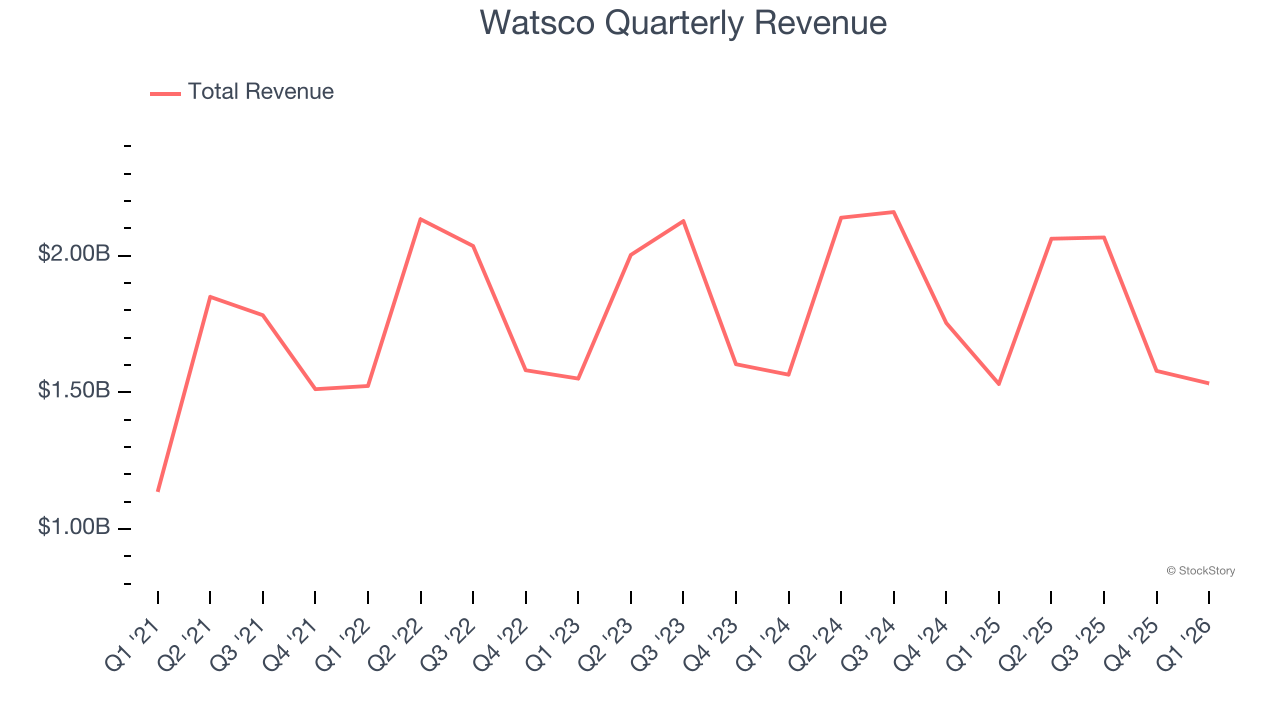

Equipment distributor Watsco (NYSE: WSO) beat Wall Street’s revenue expectations in Q1 CY2026, but sales were flat year on year at $1.53 billion. Its GAAP profit of $1.87 per share was 10.7% above analysts’ consensus estimates.

Is now the time to buy Watsco? Find out by accessing our full research report, it’s free.

Watsco (WSO) Q1 CY2026 Highlights:

- Revenue: $1.53 billion vs analyst estimates of $1.48 billion (flat year on year, 3.4% beat)

- EPS (GAAP): $1.87 vs analyst estimates of $1.69 (10.7% beat)

- Adjusted EBITDA: $129.3 million vs analyst estimates of $113.7 million (8.4% margin, 13.8% beat)

- Operating Margin: 7.2%, in line with the same quarter last year

- Free Cash Flow was -$25.77 million compared to -$185.1 million in the same quarter last year

- Market Capitalization: $17.29 billion

First quarter 2026 results reflect a 9% increase in average selling price for HVAC equipment from a higher sales mix of A2L products and higher-efficiency HVAC equipment, offset by lower unit volumes. SG&A expenses were flat, reflecting improved operating efficiency and a simpler operating environment compared to last year. Albert H. Nahmad, Chairman and CEO said: “We are extremely honored to welcome Jim Durrett and the entire Jackson Supply team to the Watsco family. Our relationship dates back more than 20 years, and we are grateful for the relationship and the commitment to entrust us with the next chapter of its 50-year legacy. This transaction adds meaningful scale and diversification to Watsco’s core Sunbelt markets. The Jackson Supply team possesses a strong track record of organic growth and an entrepreneurial spirit that closely aligns with our own. We look forward to learning from them and supporting their ambitious growth plans for years to come.”

Company Overview

Originally a manufacturing company, Watsco (NYSE: WSO) today only distributes air conditioning, heating, and refrigeration equipment, as well as related parts and supplies.

Revenue Growth

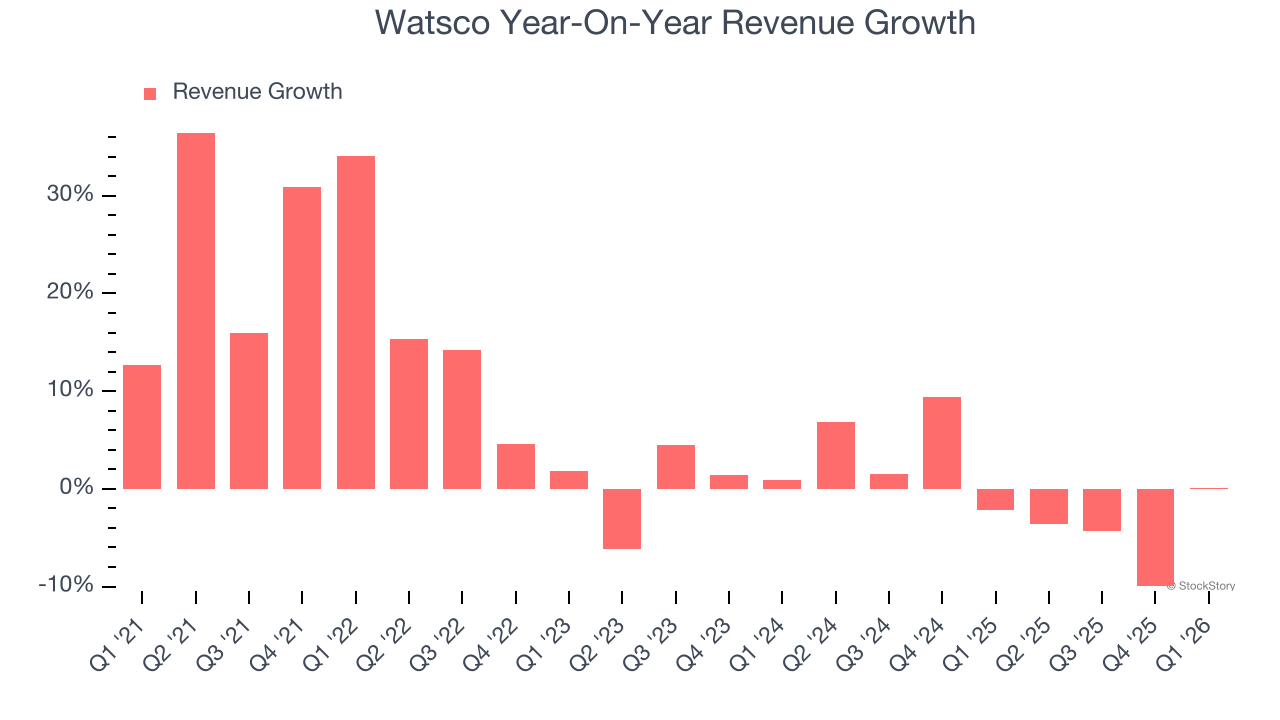

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Watsco grew its sales at a mediocre 6.9% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Watsco’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Watsco’s $1.53 billion of revenue was flat year on year but beat Wall Street’s estimates by 3.4%.

Looking ahead, sell-side analysts expect revenue to grow 2.5% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

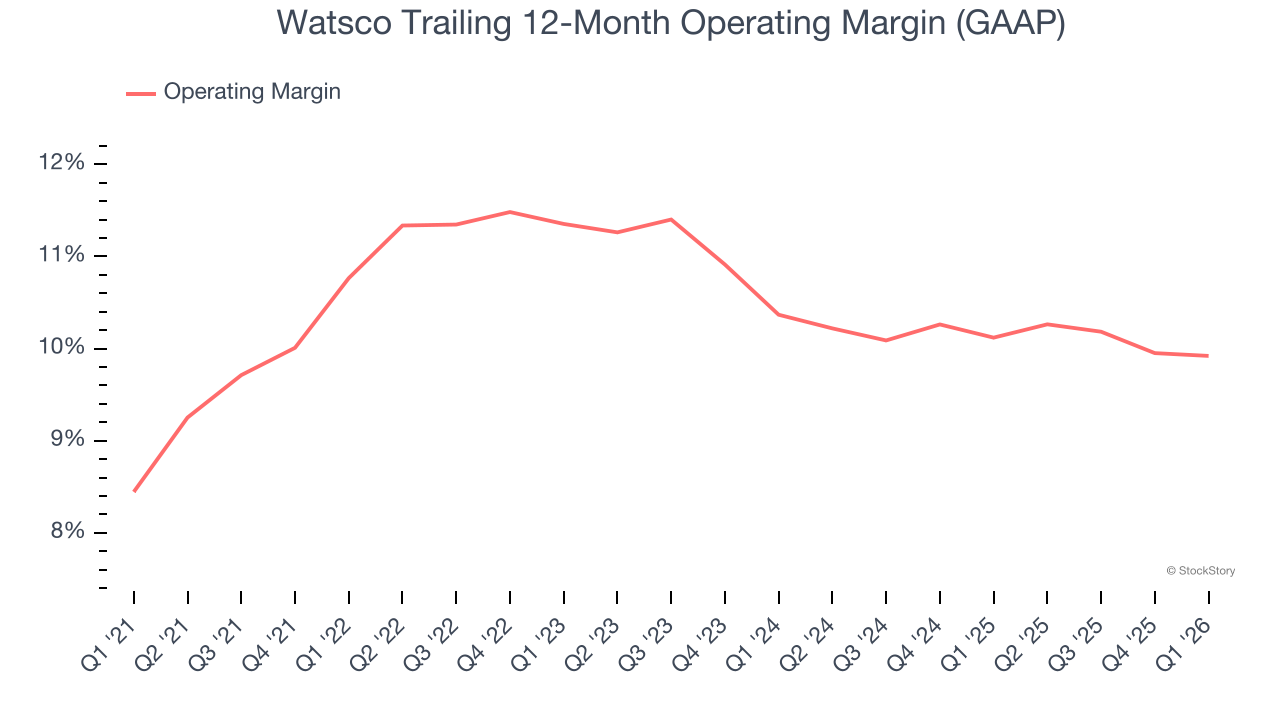

Operating Margin

Watsco’s operating margin has generally stayed the same over the last 12 months, averaging 10.5% over the last five years. This profitability was solid for an industrials business and shows it’s an efficient company that manages its expenses well. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Watsco’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but we’re still happy with Watsco’s performance considering most Infrastructure Distributors companies saw their margins plummet.

In Q1, Watsco generated an operating margin profit margin of 7.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

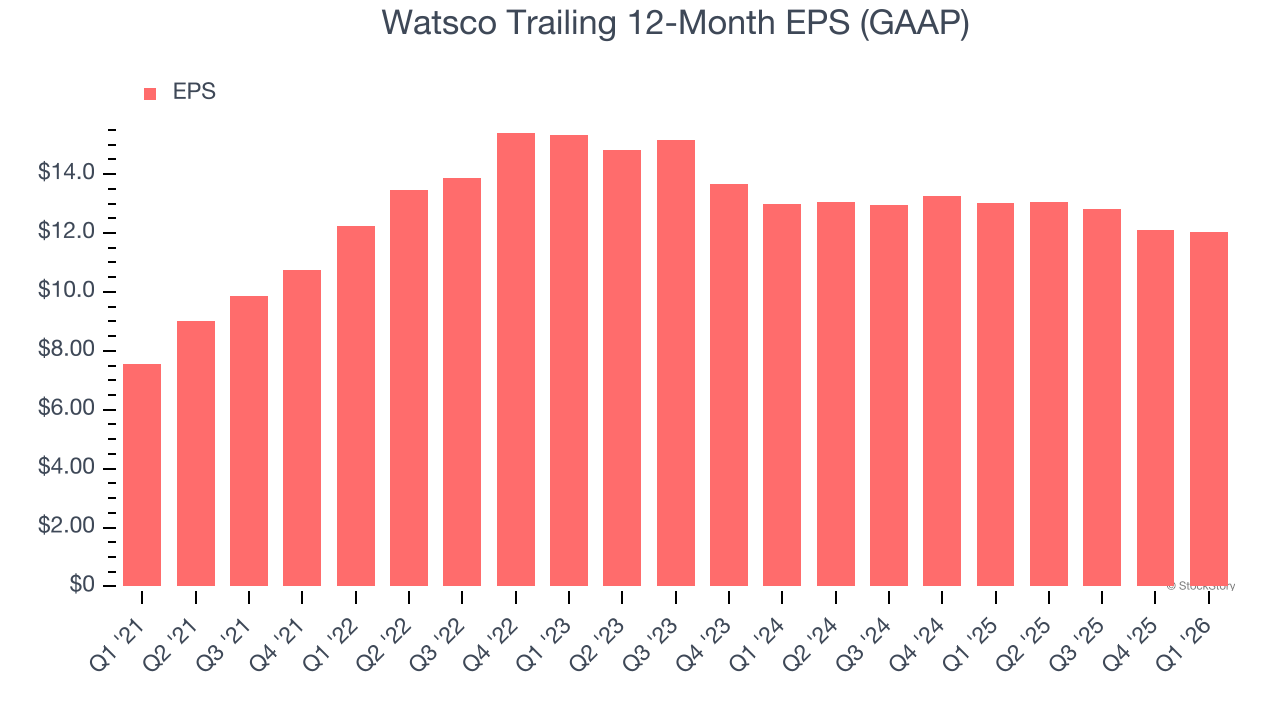

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

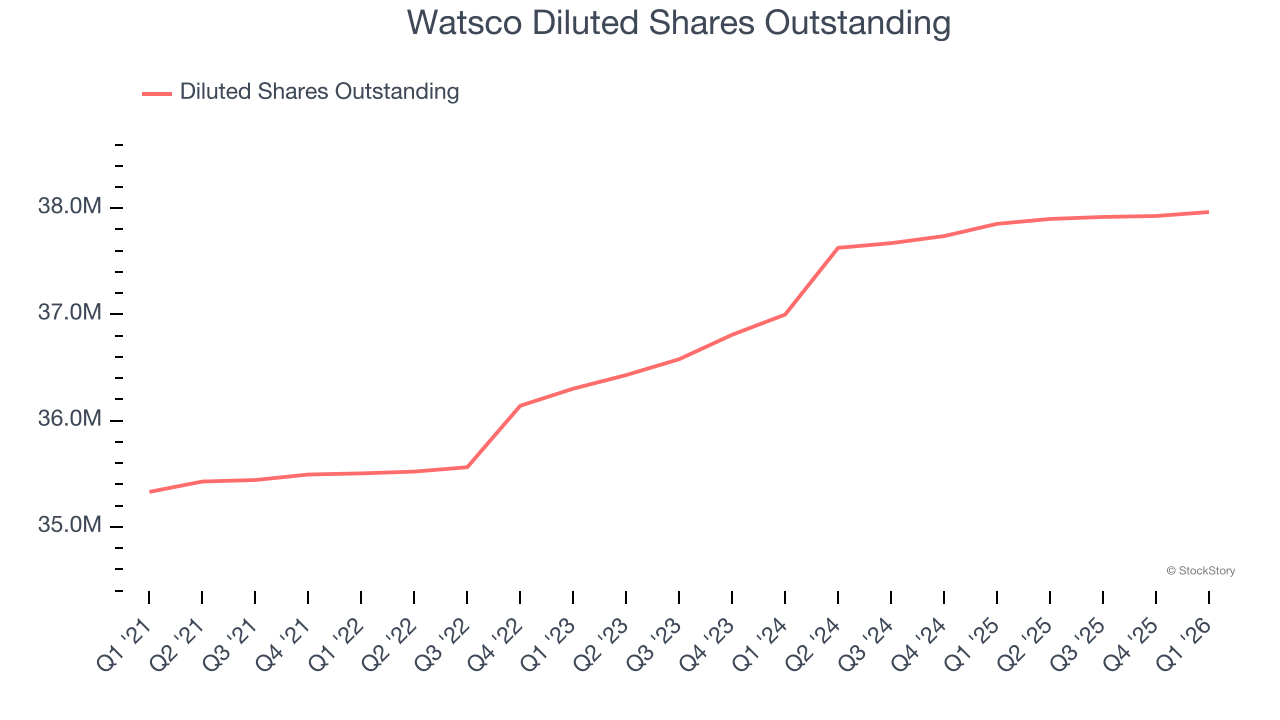

Watsco’s EPS grew at 9.8% compounded annual growth rate over the last five years, higher than its 6.9% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Watsco’s two-year annual EPS declines of 3.7% were bad and lower than its flat revenue.

Diving into the nuances of Watsco’s earnings can give us a better understanding of its performance. A two-year view shows Watsco has diluted its shareholders, growing its share count by 2.6%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Watsco reported EPS of $1.87, down from $1.93 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Watsco’s full-year EPS of $12.05 to grow 5.6%.

Key Takeaways from Watsco’s Q1 Results

We were impressed by how significantly Watsco blew past analysts’ EBITDA expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $460.28 immediately after reporting.

Indeed, Watsco had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).