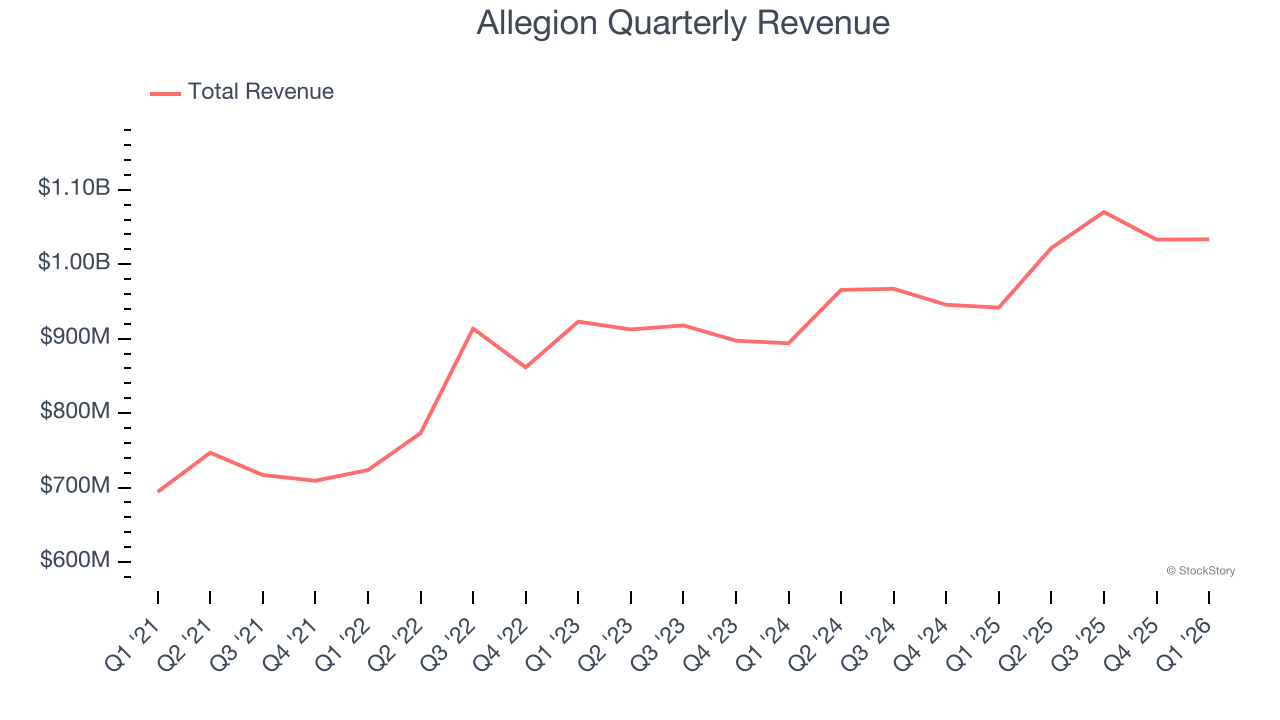

Security hardware provider Allegion (NYSE: ALLE) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 9.7% year on year to $1.03 billion. Its non-GAAP profit of $1.80 per share was 5.1% below analysts’ consensus estimates.

Is now the time to buy Allegion? Find out by accessing our full research report, it’s free.

Allegion (ALLE) Q1 CY2026 Highlights:

- Revenue: $1.03 billion vs analyst estimates of $1.03 billion (9.7% year-on-year growth, 0.8% beat)

- Adjusted EPS: $1.80 vs analyst expectations of $1.90 (5.1% miss)

- Adjusted EBITDA: $236.8 million vs analyst estimates of $242.9 million (22.9% margin, 2.5% miss)

- Management reiterated its full-year Adjusted EPS guidance of $8.80 at the midpoint

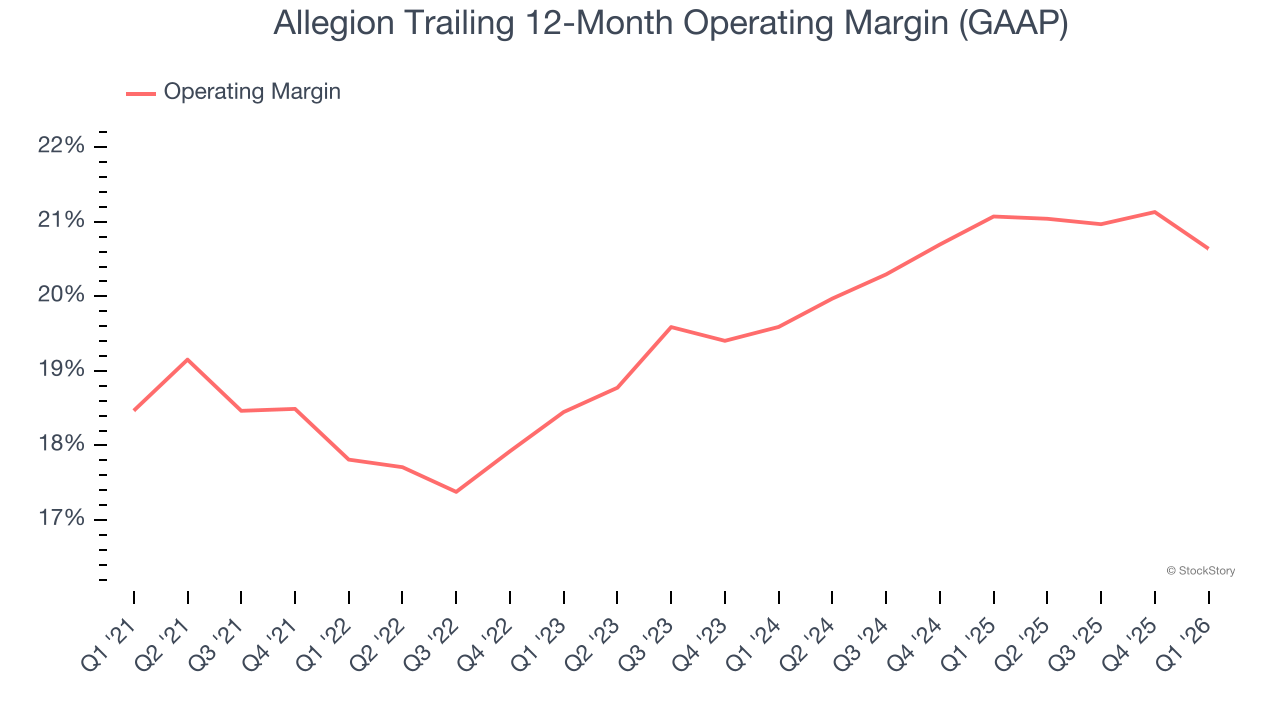

- Operating Margin: 18.9%, down from 20.9% in the same quarter last year

- Free Cash Flow Margin: 7.8%, down from 8.9% in the same quarter last year

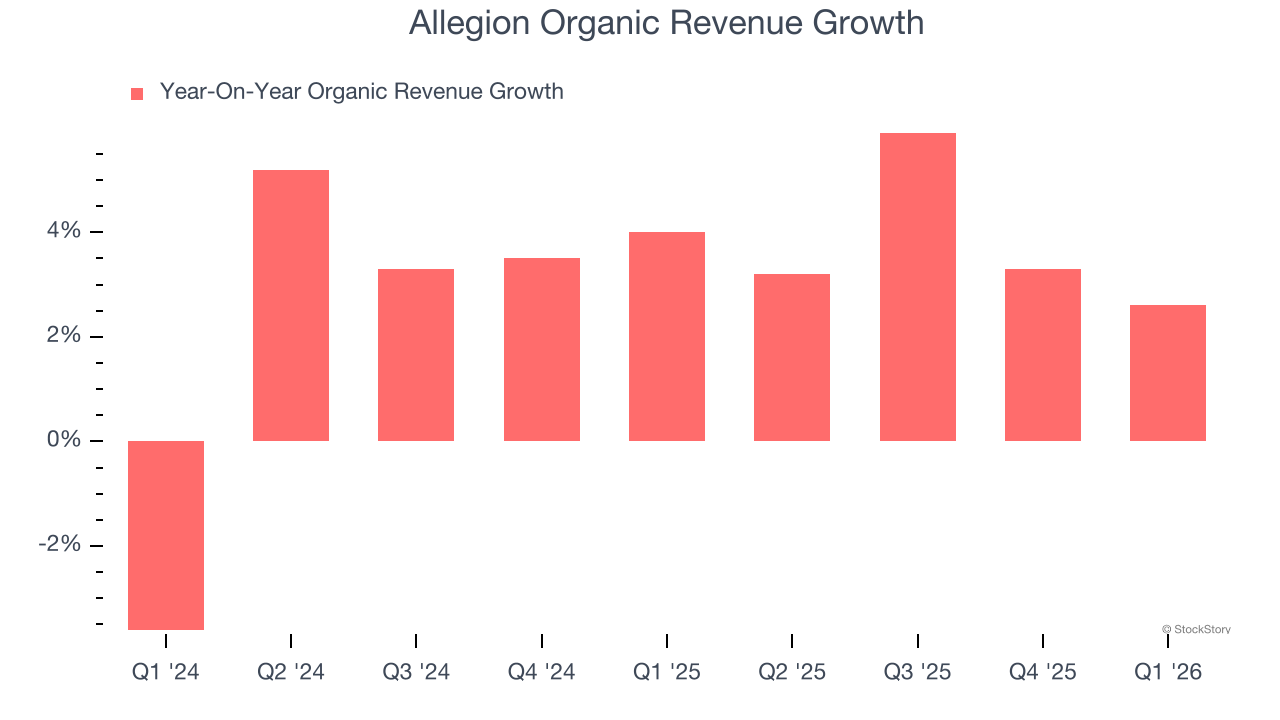

- Organic Revenue rose 2.6% year on year (miss)

- Market Capitalization: $12.75 billion

“Allegion delivered strong Q1 revenue growth led by our Americas non-residential and electronics businesses,” Allegion President and CEO John H. Stone said.

Company Overview

Allegion plc (NYSE: ALLE) is a provider of security products and solutions that keep people and assets safe and secure in various environments.

Revenue Growth

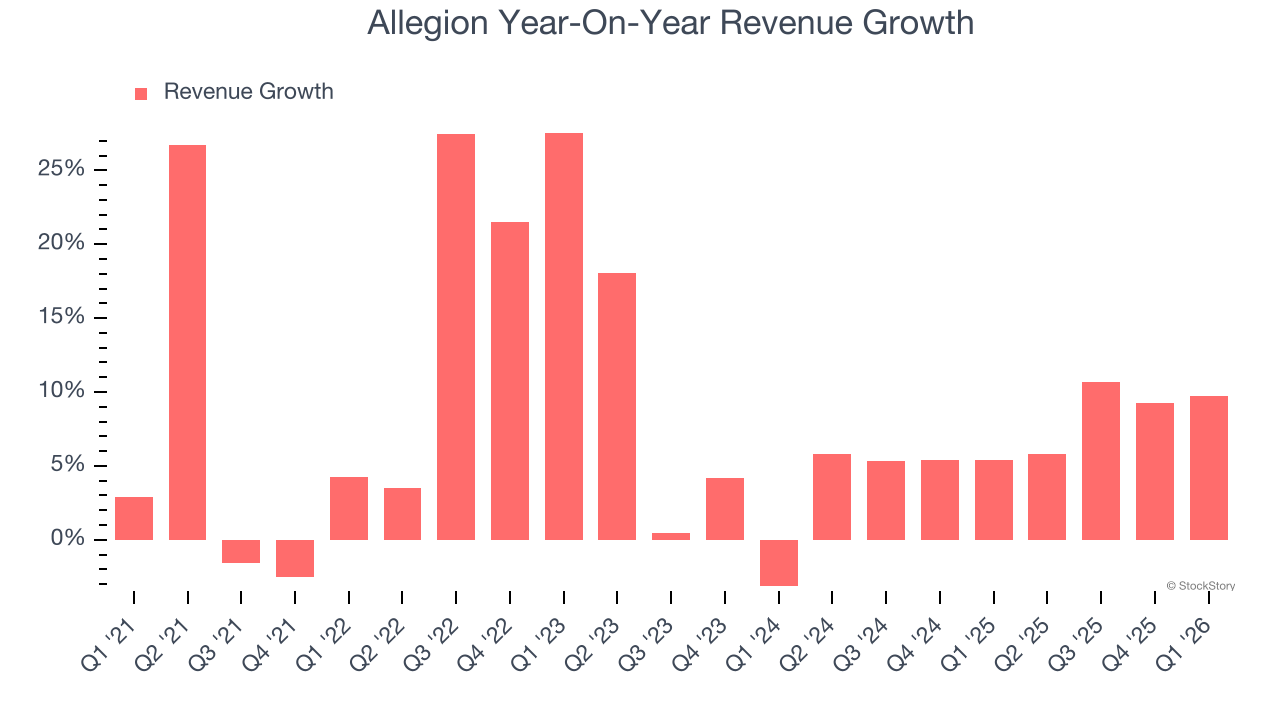

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Allegion’s 8.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Allegion’s recent performance shows its demand has slowed as its annualized revenue growth of 7.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Allegion’s organic revenue averaged 3.9% year-on-year growth. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Allegion reported year-on-year revenue growth of 9.7%, and its $1.03 billion of revenue exceeded Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Allegion has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 19.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Allegion’s operating margin rose by 2.8 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Allegion generated an operating margin profit margin of 18.9%, down 2 percentage points year on year. Since Allegion’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

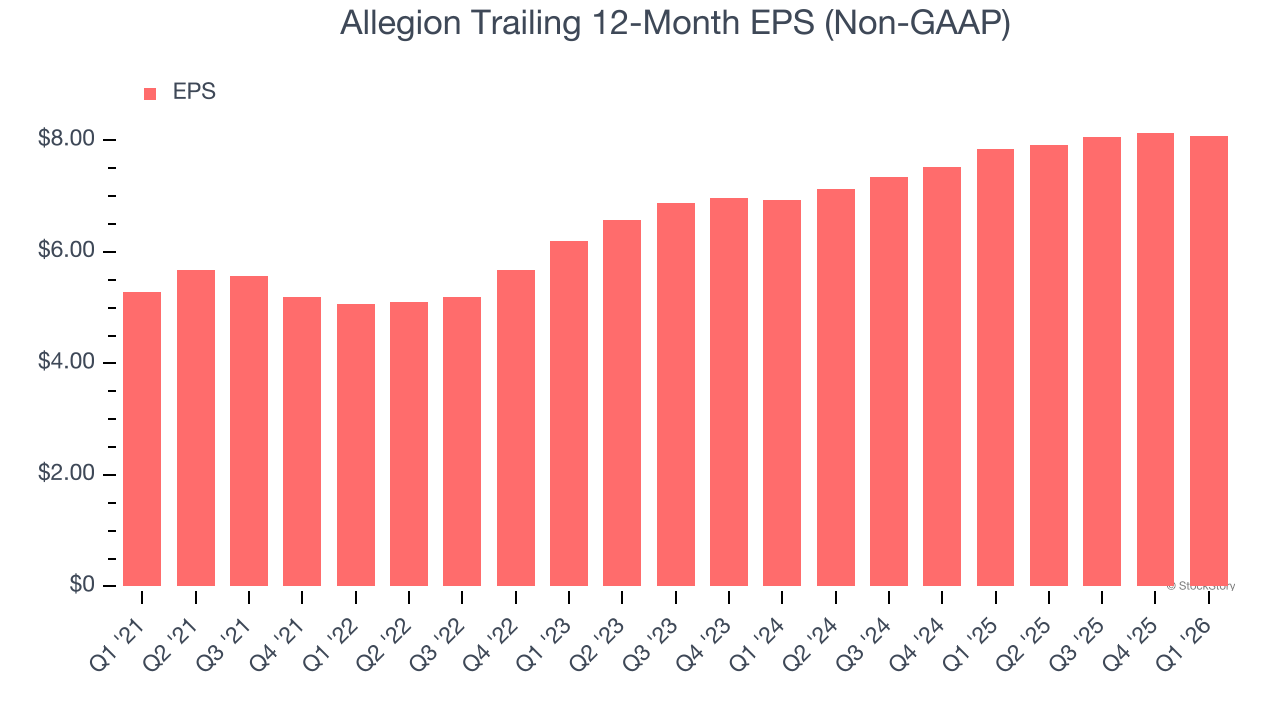

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Allegion’s decent 8.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Allegion, its two-year annual EPS growth of 8% is similar to its five-year trend, implying stable earnings.

In Q1, Allegion reported adjusted EPS of $1.80, down from $1.86 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Allegion’s full-year EPS of $8.08 to grow 12.2%.

Key Takeaways from Allegion’s Q1 Results

It was good to see Allegion narrowly top analysts’ revenue expectations this quarter. On the other hand, its adjusted operating income missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $148.37 immediately following the results.

Allegion didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).