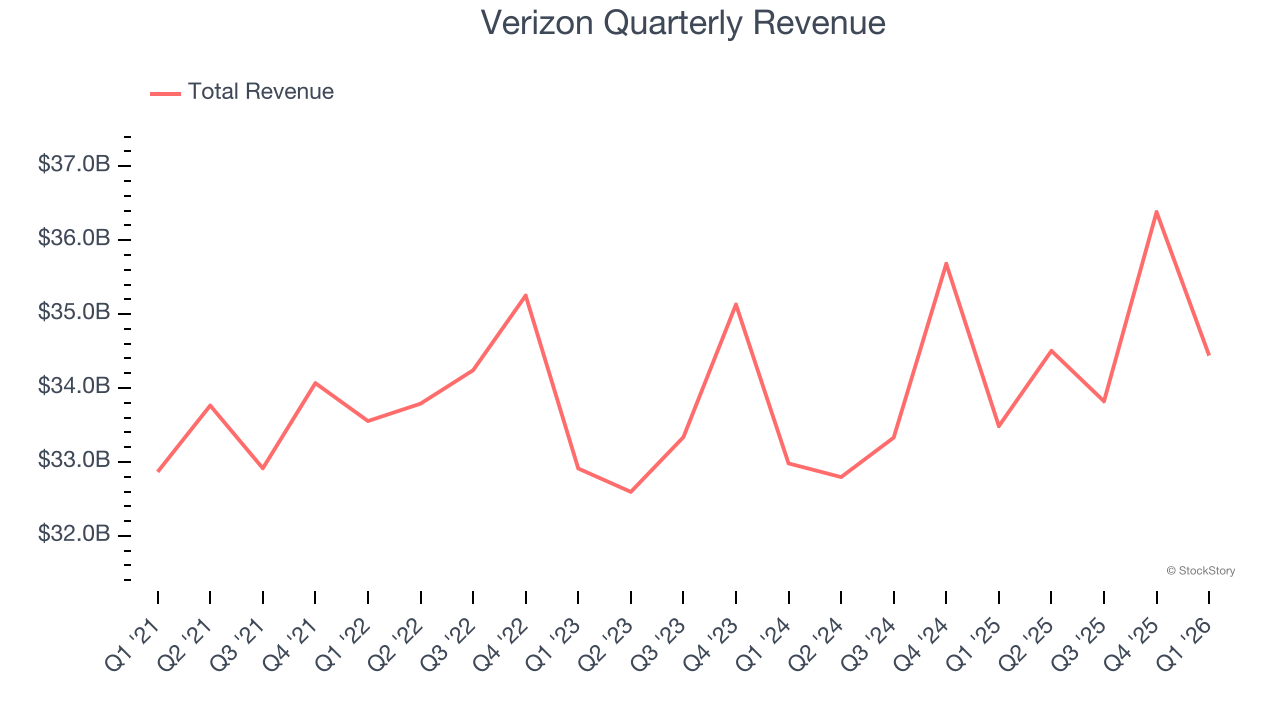

Telecommunications giant Verizon (NYSE: VZ) fell short of the market’s revenue expectations in Q1 CY2026 as sales rose 2.9% year on year to $34.44 billion. Its non-GAAP profit of $1.28 per share was 5.8% above analysts’ consensus estimates.

Is now the time to buy Verizon? Find out by accessing our full research report, it’s free.

Verizon (VZ) Q1 CY2026 Highlights:

- Revenue: $34.44 billion vs analyst estimates of $34.95 billion (2.9% year-on-year growth, 1.5% miss)

- Total postpaid phone net adds of 55,000 vs analyst expectations of a net loss (beat)

- Expects full-year postpaid phone net adds to be top previous range of 750k to 1 million subscribers

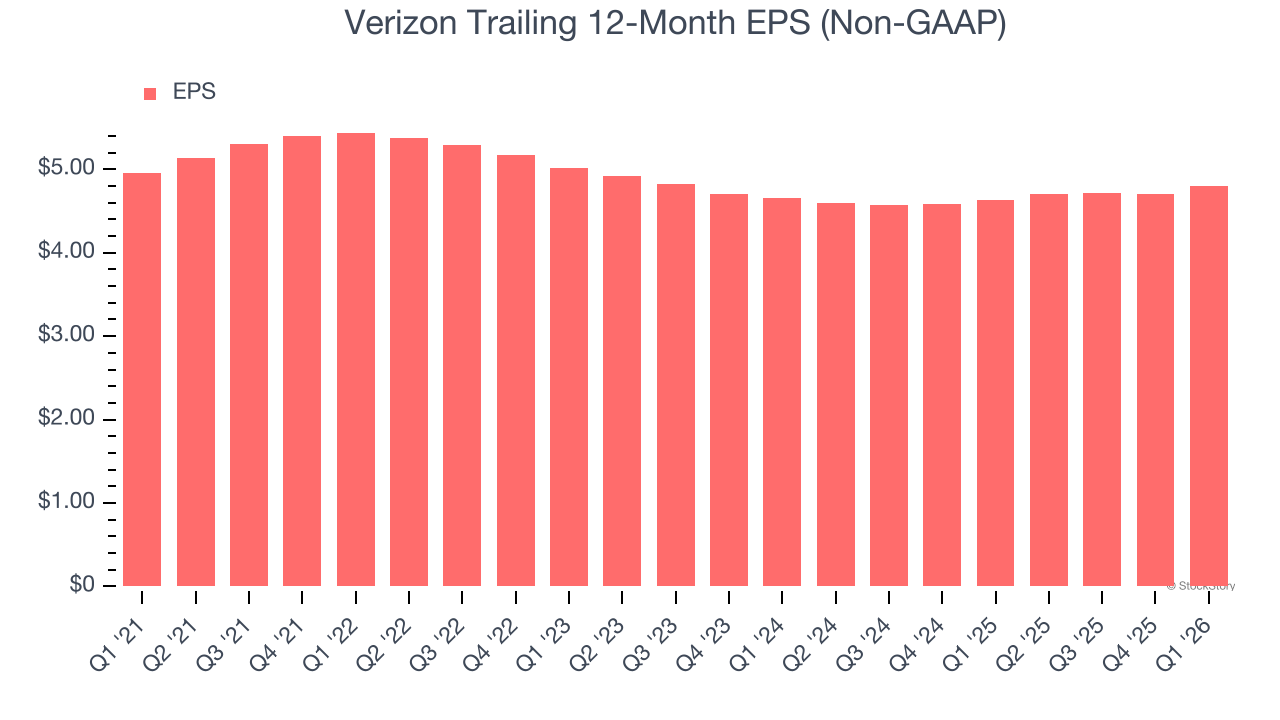

- Adjusted EPS: $1.28 vs analyst estimates of $1.21 (5.8% beat)

- Adjusted EBITDA: $13.4 billion vs analyst estimates of $13.14 billion (38.9% margin, 1.9% beat)

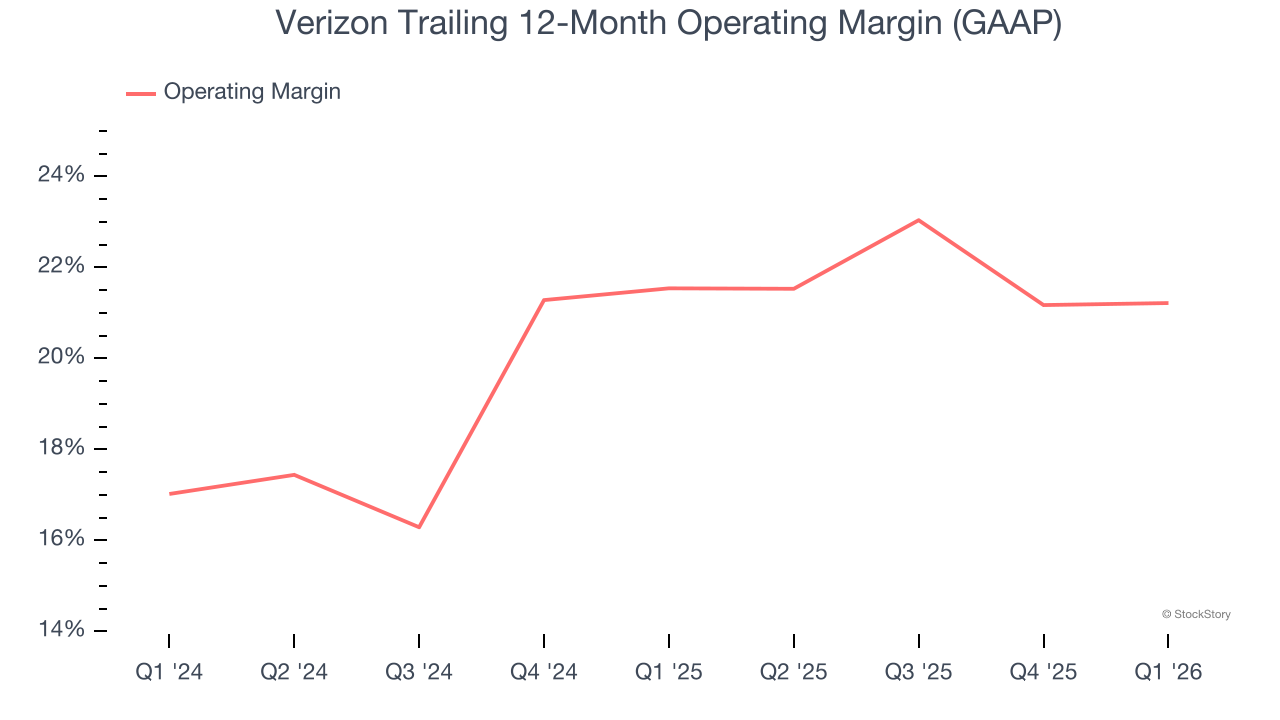

- Operating Margin: 23.9%, in line with the same quarter last year

- Free Cash Flow Margin: 11%, similar to the same quarter last year

- Market Capitalization: $193.9 billion

Company Overview

Formed in 1984 as Bell Atlantic after the breakup of Bell System into seven companies, Verizon (NYSE: VZ) is a telecom giant providing a range of communications and internet services.

Revenue Growth

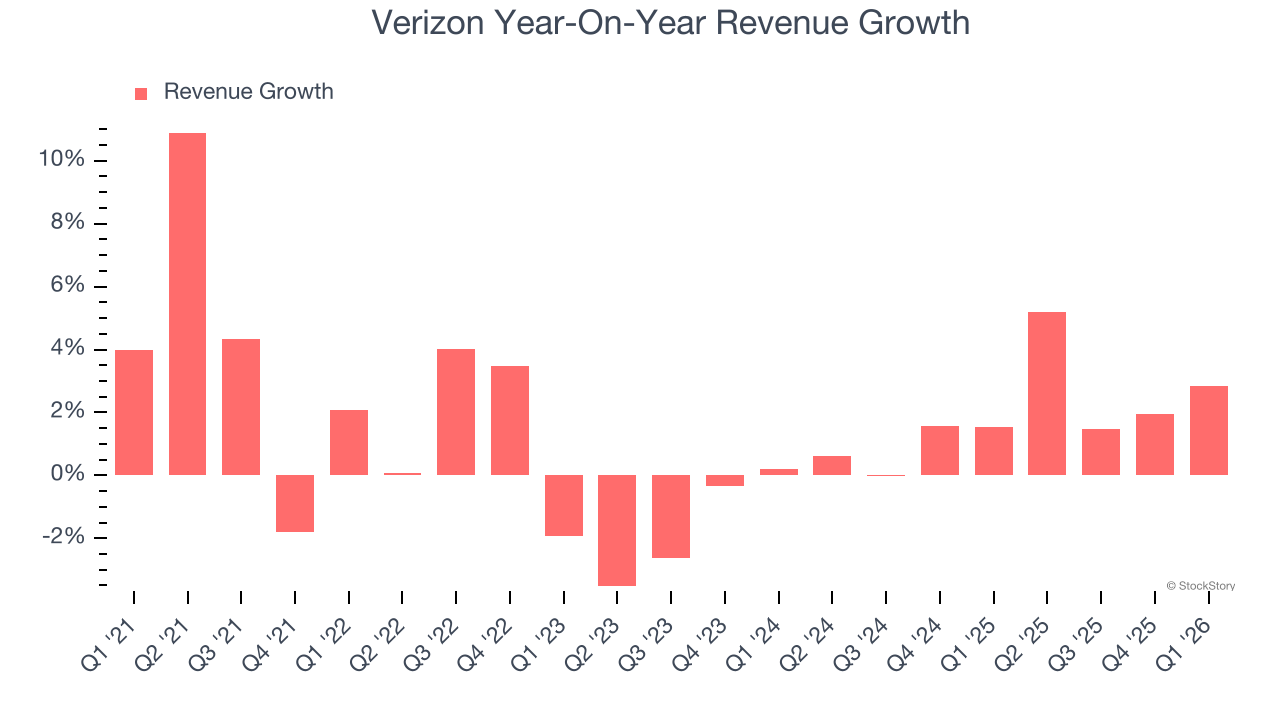

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Verizon’s 1.4% annualized revenue growth over the last five years was weak. This fell short of our benchmarks and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Verizon’s annualized revenue growth of 1.9% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Verizon’s revenue grew by 2.9% year on year to $34.44 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Verizon’s operating margin has more or less stayed the same over the last 12 months , and we generally like to see margin increases due to economies of scale and cost efficiency over time.

In Q1, Verizon generated an operating margin profit margin of 23.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Verizon’s flat EPS over the last five years was below its 1.4% annualized revenue growth. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

In Q1, Verizon reported adjusted EPS of $1.28, up from $1.19 in the same quarter last year. This print beat analysts’ estimates by 5.8%. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Verizon’s Q1 Results

This was the first reported quarter under a new CEO, and the company delivered with positive postpaid phone net additions versus expectations of a loss. Full-year guidance for the same metric was also raised. This led to an EPS beat. Overall, this was a solid quarter. The stock traded up 3.4% to $47.98 immediately following the results.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).