Over the last six months, Take-Two’s shares have sunk to $211.24, producing a disappointing 16.9% loss - a stark contrast to the S&P 500’s 4.2% gain. This may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for TTWO? Find out in our full research report, it’s free.

Why Does Take-Two Spark Debate?

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ: TTWO) is one of the world’s largest video game publishers.

Two Positive Attributes:

1. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Take-Two’s revenue to rise by 28%, an improvement versus This projection is eye-popping and suggests its newer products and services will fuel better top-line performance.

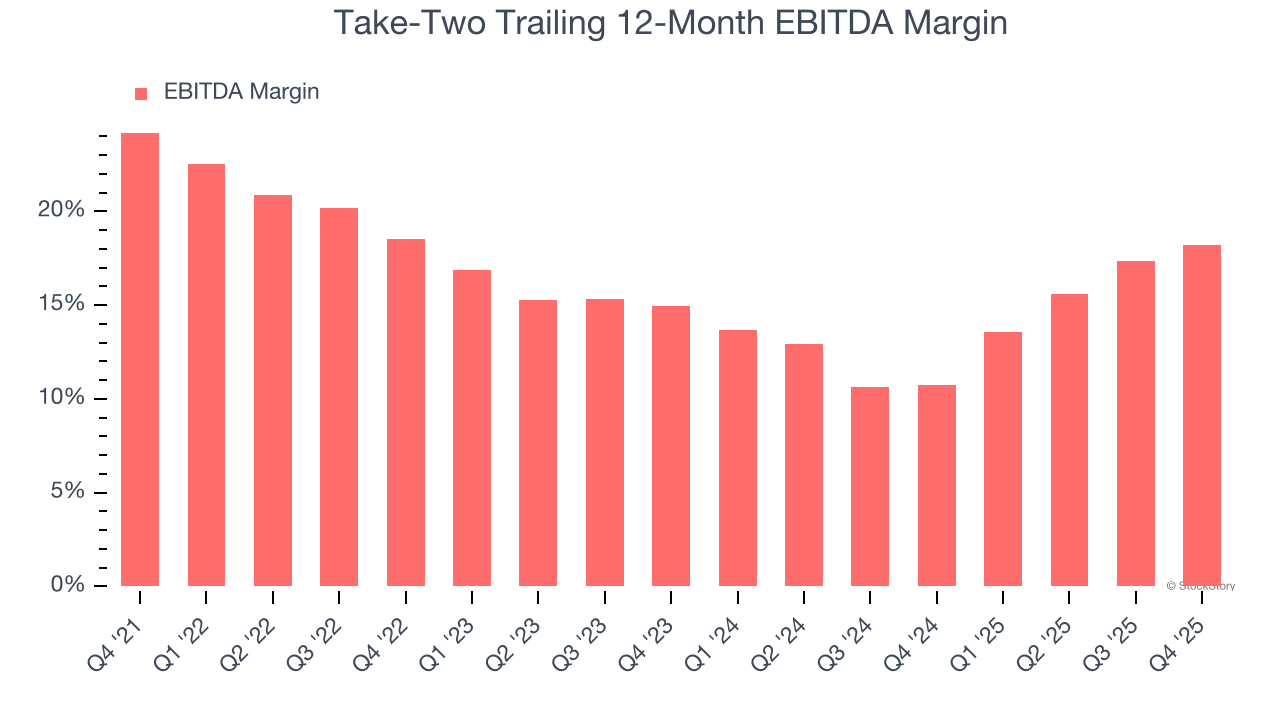

2. EBITDA Margin Reveals a Well-Run Organization

EBITDA is a good way of judging operating profitability for consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a more standardized view of the business’s profit potential.

Take-Two’s EBITDA margin has been trending up over the last 12 months and averaged 14.9% over the last two years. On top of that, its profitability was top-notch for a consumer internet business, showing it’s an well-run company with an efficient cost structure.

One Reason to be Careful:

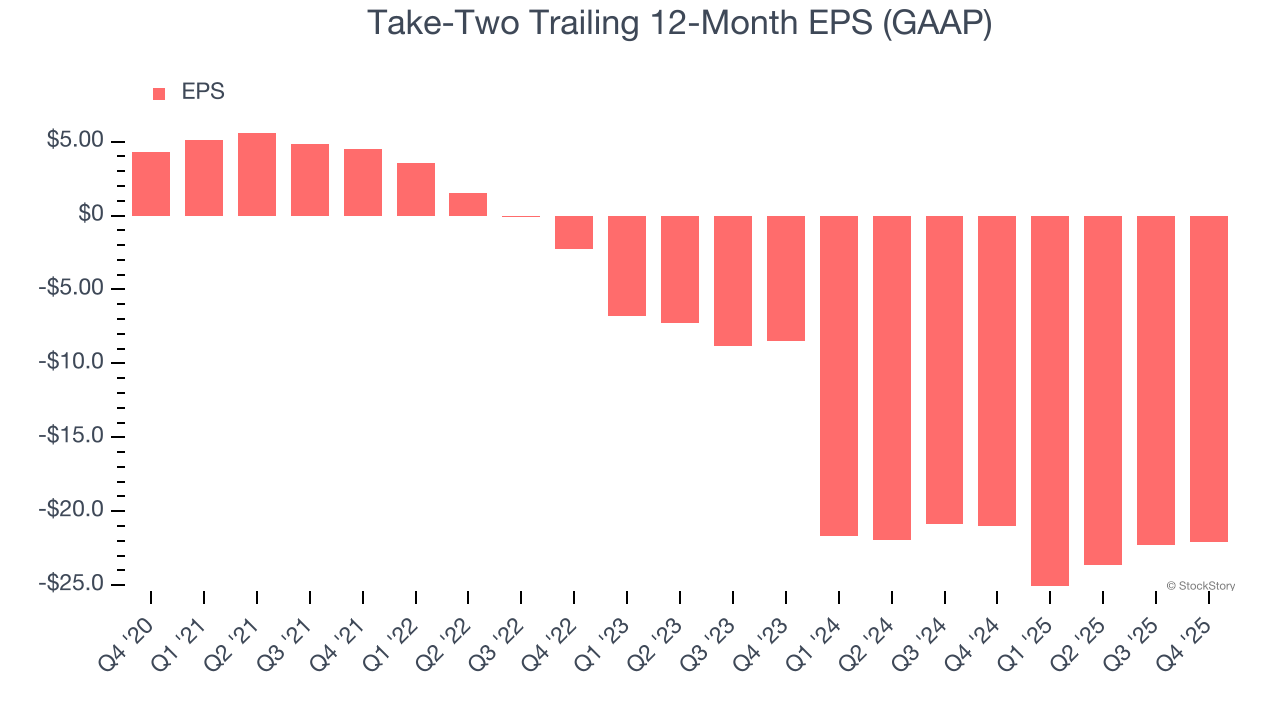

EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Take-Two’s earnings losses deepened over the last three years as its EPS dropped annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

Final Judgment

Take-Two’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 24.7× forward EV/EBITDA (or $211.24 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Take-Two

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.