Regional banking company Lakeland Financial (NASDAQGS:LKFN) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 7.4% year on year to $69.71 million. Its GAAP profit of $1.04 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy Lake City Bank? Find out by accessing our full research report, it’s free.

Lake City Bank (LKFN) Q1 CY2026 Highlights:

- Net Interest Income: $56.77 million vs analyst estimates of $57.94 million (7.4% year-on-year growth, 2% miss)

- Net Interest Margin: 3.5% vs analyst estimates of 3.5% (in line)

- Revenue: $69.71 million vs analyst estimates of $70.18 million (7.4% year-on-year growth, 0.7% miss)

- Efficiency Ratio: 50.4% vs analyst estimates of 49.5% (93 basis point miss)

- EPS (GAAP): $1.04 vs analyst estimates of $1.01 (2.7% beat)

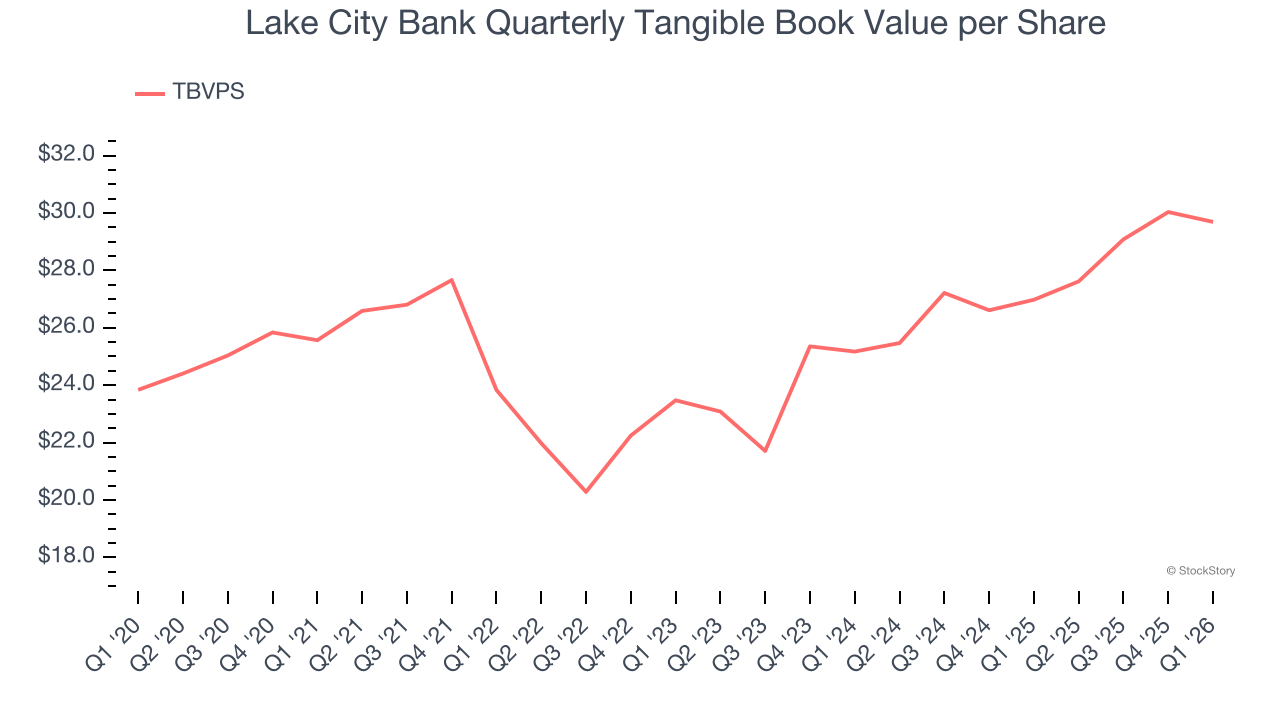

- Tangible Book Value per Share: $29.69 vs analyst estimates of $30.37 (10.1% year-on-year growth, 2.2% miss)

- Market Capitalization: $1.51 billion

As announced on April 14, 2026, the board of directors approved a cash dividend for the first quarter of $0.52 per share, payable on May 5, 2026, to shareholders of record as of April 25, 2026. The first quarter dividend per share represents a 4% increase from the $0.50 dividend per share paid for the first quarter of 2025. Kristin L. Pruitt, President, commented, “We continue to operate with strong levels of capital to support our organic loan growth strategy and cash dividend return to shareholders, which increased by 4% in 2026. In addition, we opportunistically repurchased 3% of our year-end outstanding common stock during the last two quarters, reflecting our confidence in our continued ability to generate future shareholder value.”

Company Overview

Dating back to 1872 and deeply rooted in Indiana's communities, Lakeland Financial Corporation (NASDAQ: LKFN) operates Lake City Bank, providing commercial and consumer banking services throughout Northern and Central Indiana.

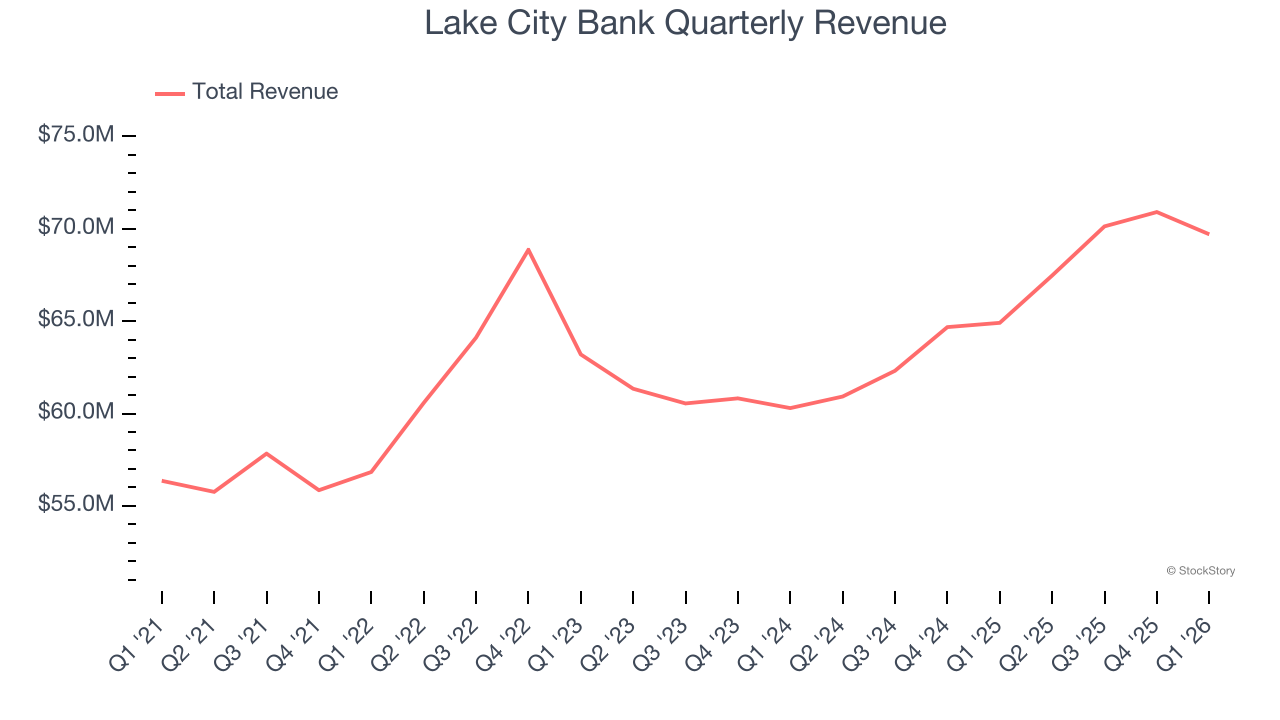

Sales Growth

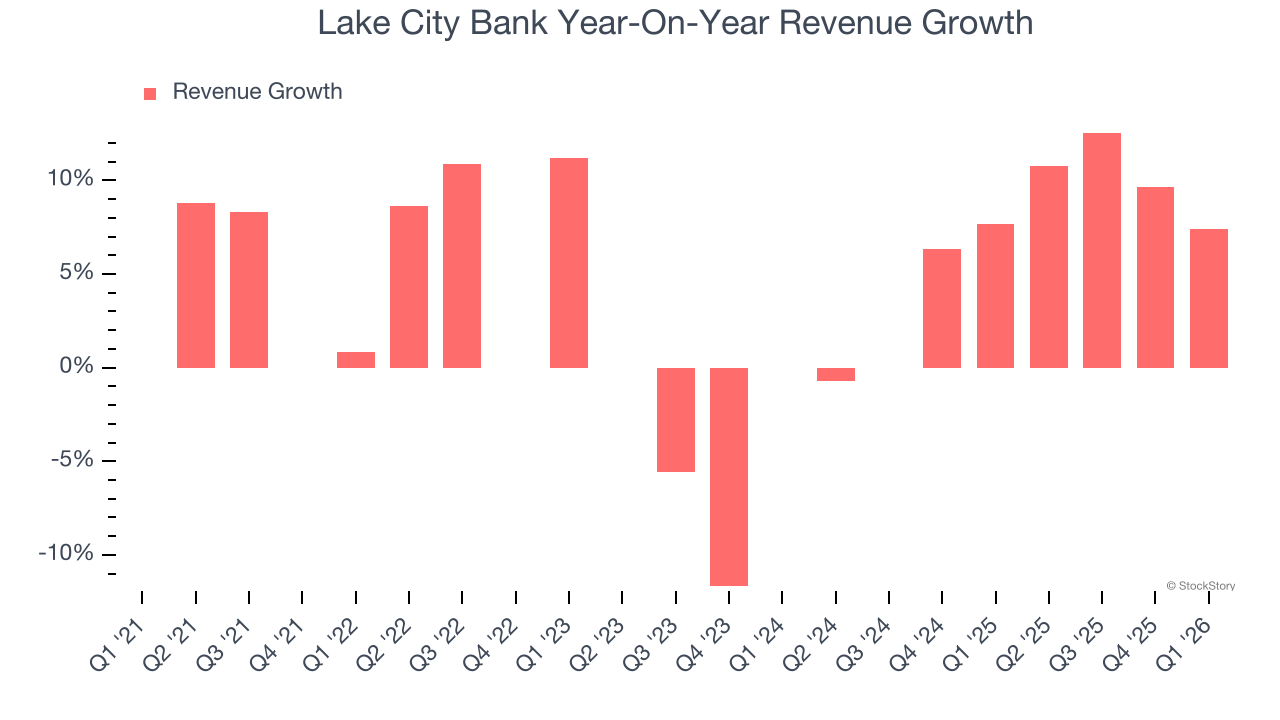

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Regrettably, Lake City Bank’s revenue grew at a sluggish 5% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Lake City Bank’s annualized revenue growth of 7% over the last two years is above its five-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Lake City Bank’s revenue grew by 7.4% year on year to $69.71 million, missing Wall Street’s estimates.

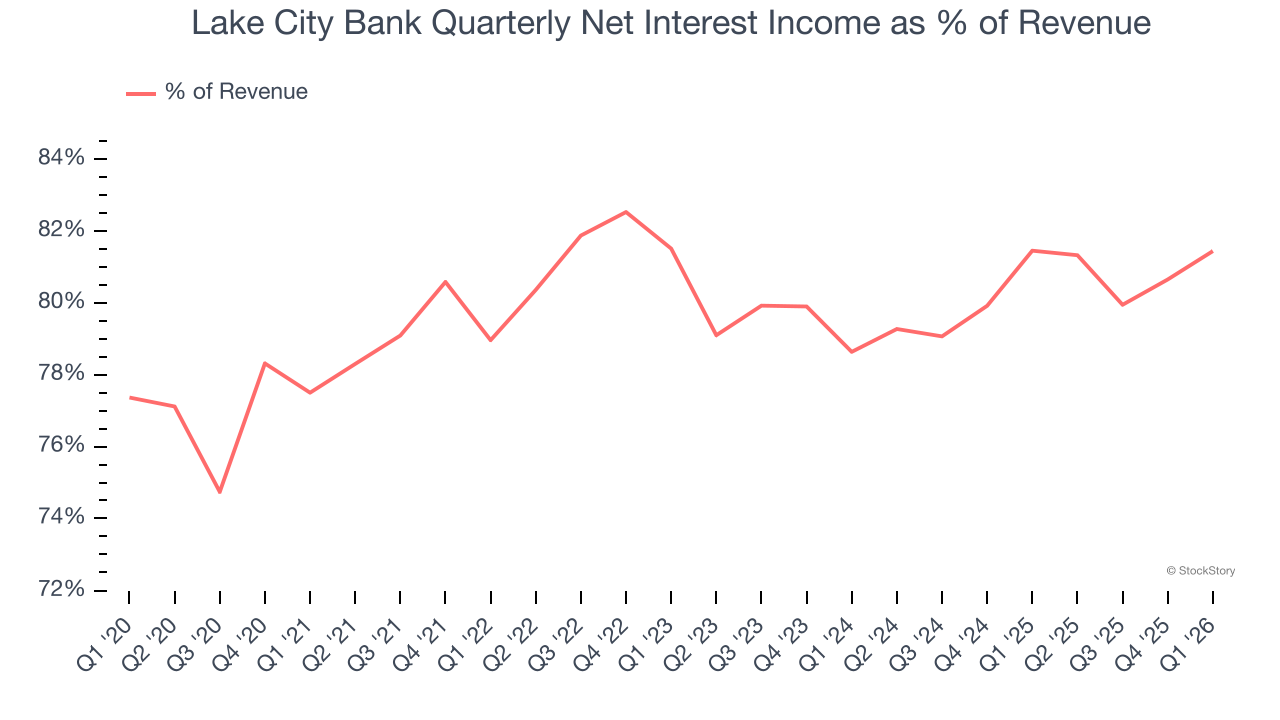

Net interest income made up 80.2% of the company’s total revenue during the last five years, meaning Lake City Bank barely relies on non-interest income to drive its overall growth.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

Lake City Bank’s TBVPS grew at a tepid 3% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 8.6% annually over the last two years from $25.17 to $29.69 per share.

Over the next 12 months, Consensus estimates call for Lake City Bank’s TBVPS to grow by 11% to $32.95, mediocre growth rate.

Key Takeaways from Lake City Bank’s Q1 Results

Lake City Bank's EPS beat in the quarter. However, its net interest income, efficiency ratio, and tangible book value per share fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $59.68 immediately after reporting.

The latest quarter from Lake City Bank’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).