Expedia currently trades at $228.13 per share and has shown little upside over the past six months, posting a middling return of 4.8%. However, the stock is beating the S&P 500’s 2.8% decline during that period.

Given the relative strength, is there still a buying opportunity in EXPE? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does Expedia Spark Debate?

Originally founded as a part of Microsoft, Expedia (NASDAQ: EXPE) is one of the world’s leading online travel agencies.

Two Things to Like:

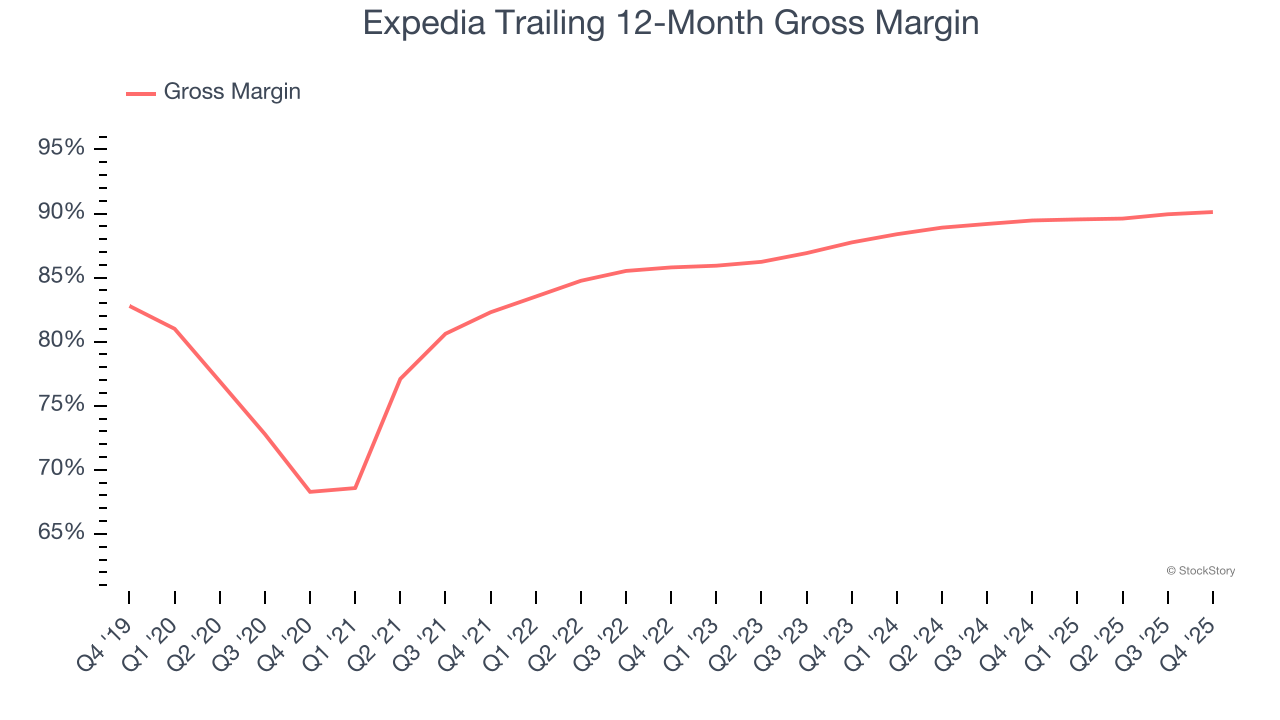

1. Elite Gross Margin Powers Best-In-Class Business Model

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

For online travel businesses like Expedia, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer support, payment processing, fulfillment fees (paid to the airlines, hotels, or car rental companies), and data center expenses to keep the app or website online.

Expedia’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 89.8% gross margin over the last two years. Said differently, roughly $89.80 was left to spend on selling, marketing, and R&D for every $100 in revenue.

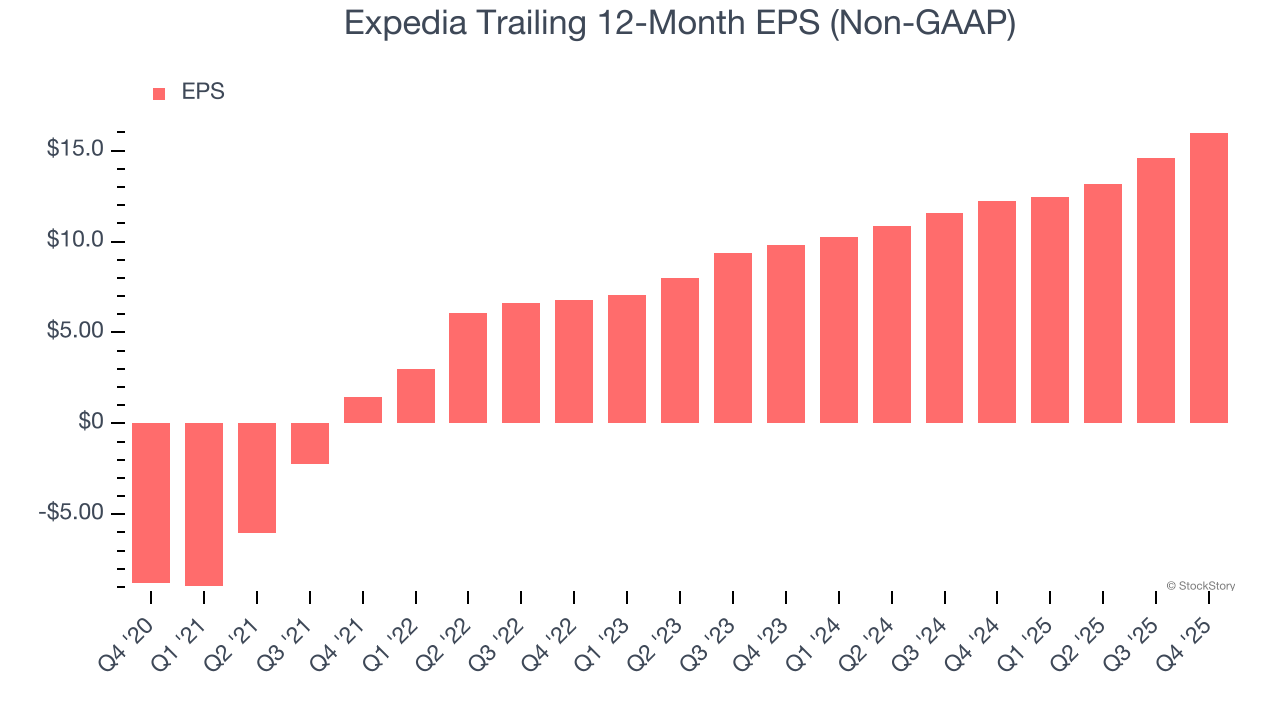

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Expedia’s EPS grew at 33% compounded annual growth rate over the last three years, higher than its 8.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

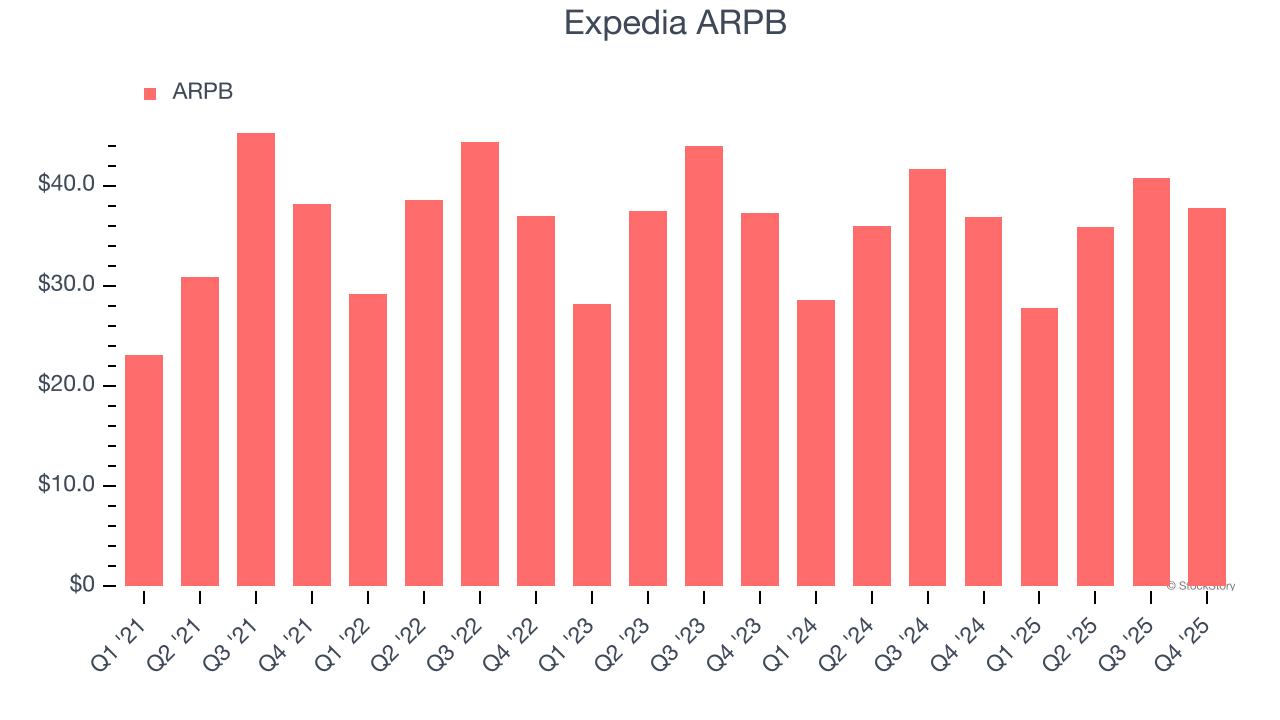

Customer Spending Decreases, Engagement Falling?

Average revenue per booking (ARPB) is a critical metric to track because it not only measures how much users book on its platform but also the commission that Expedia can charge.

Expedia’s ARPB fell over the last two years, averaging 1.5% annual declines. This isn’t great, but the increase in room nights booked is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Expedia tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether bookings can continue growing at the current pace.

Final Judgment

Expedia’s positive characteristics outweigh the negatives, and with its recent outperformance in a weaker market environment, the stock trades at 7.7× forward EV/EBITDA (or $228.13 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Expedia

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.