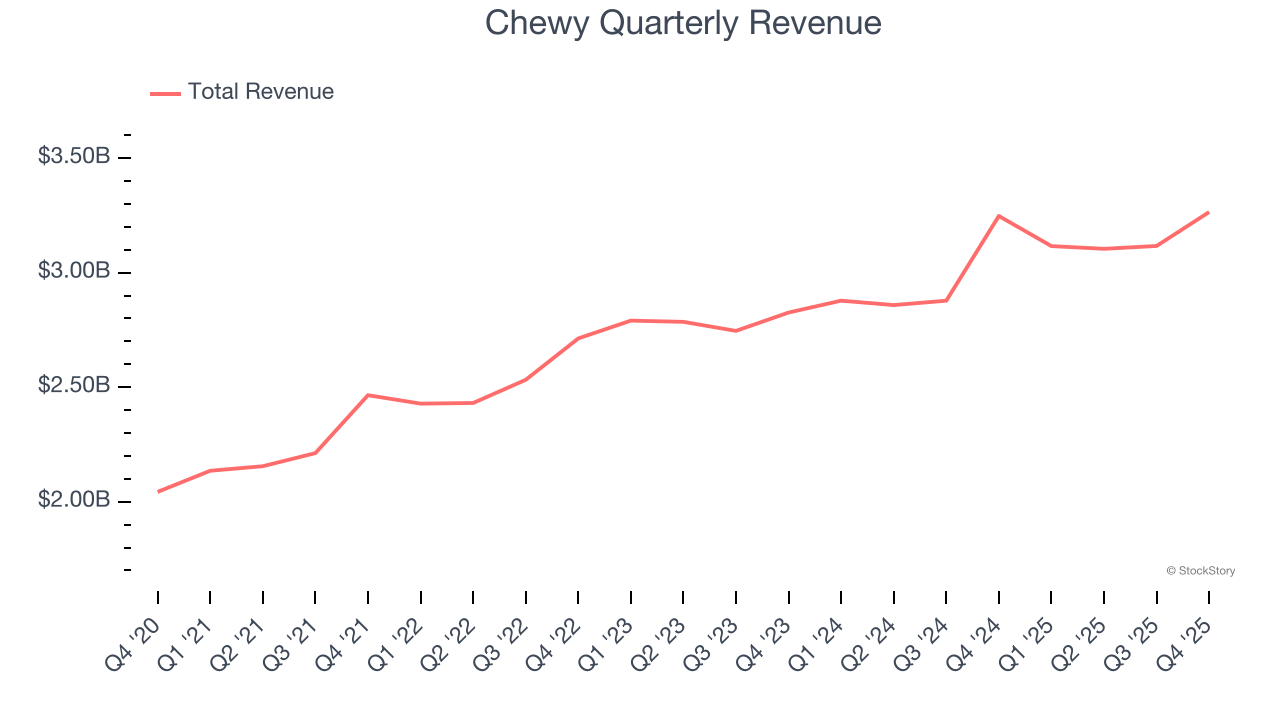

E-commerce pet food and supplies retailer Chewy (NYSE: CHWY) met Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $3.26 billion. Its non-GAAP profit of $0.27 per share was in line with analysts’ consensus estimates.

Is now the time to buy Chewy? Find out by accessing our full research report, it’s free.

Chewy (CHWY) Q4 CY2025 Highlights:

- Revenue: $3.26 billion vs analyst estimates of $3.27 billion (flat year on year, in line)

- Adjusted EPS: $0.27 vs analyst estimates of $0.28 (in line)

- Adjusted EBITDA: $162.3 million vs analyst estimates of $160.6 million (5% margin, 1.1% beat)

- Operating Margin: 1.3%, up from -0.3% in the same quarter last year

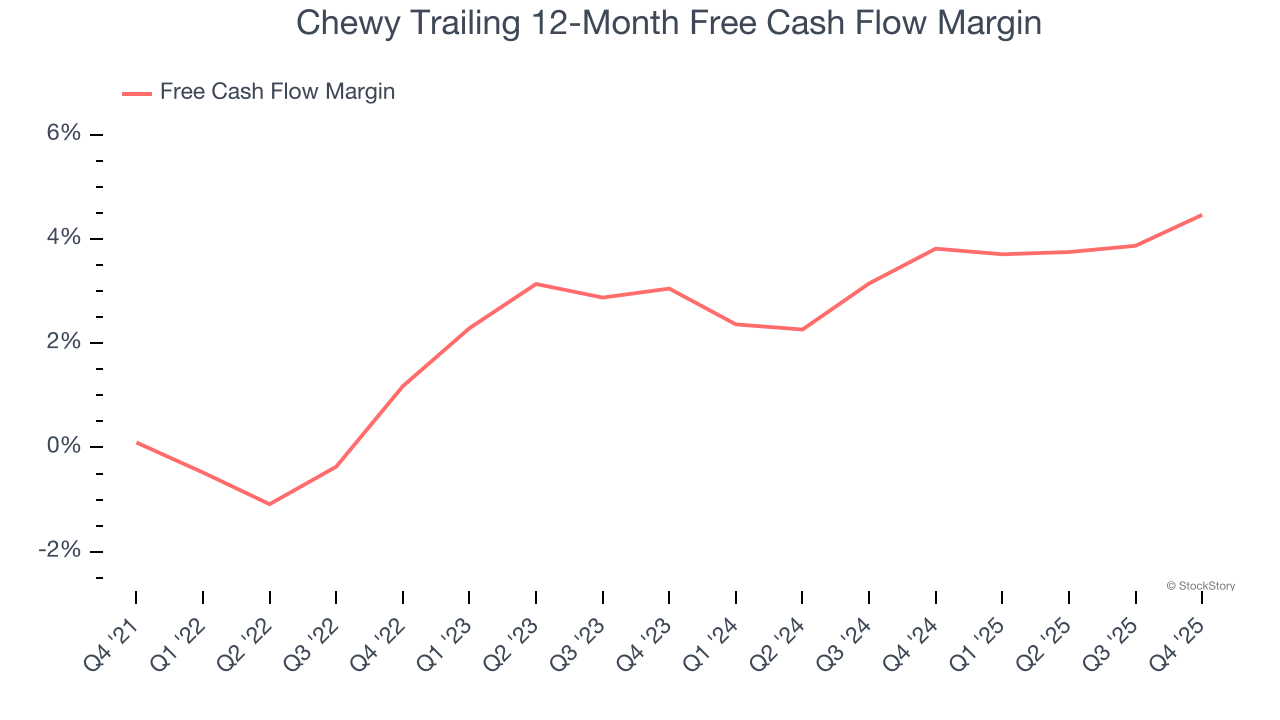

- Free Cash Flow Margin: 7.1%, up from 5.6% in the previous quarter

- Market Capitalization: $9.73 billion

Company Overview

Founded by Ryan Cohen, who later became known for his involvement in GameStop, Chewy (NYSE: CHWY) is an online retailer specializing in pet food, supplies, and healthcare services.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Chewy’s 7.6% annualized revenue growth over the last three years was tepid. This fell short of our benchmark for the consumer internet sector and is a rough starting point for our analysis.

This quarter, Chewy’s $3.26 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.7% over the next 12 months, similar to its three-year rate. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Chewy has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.1%, below what we’d expect for a consumer internet business.

Taking a step back, an encouraging sign is that Chewy’s margin expanded by 3.3 percentage points over the last few years. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Chewy’s free cash flow clocked in at $232 million in Q4, equivalent to a 7.1% margin. This result was good as its margin was 2.3 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Chewy’s Q4 Results

It was good to see Chewy top analysts’ EBITDA expectations this quarter on in-line revenue. Zooming out, we think this was a decent quarter, and with seemingly lower expectations, the shares reacted positively. The stock traded up 12.1% to $26.11 immediately following the results.

So do we think Chewy is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).