Since September 2025, Wyndham has been in a holding pattern, posting a small loss of 3.1% while floating around $78.47.

Is there a buying opportunity in Wyndham, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Wyndham Will Underperform?

We don't have much confidence in Wyndham. Here are three reasons why WH doesn't excite us and a stock we'd rather own.

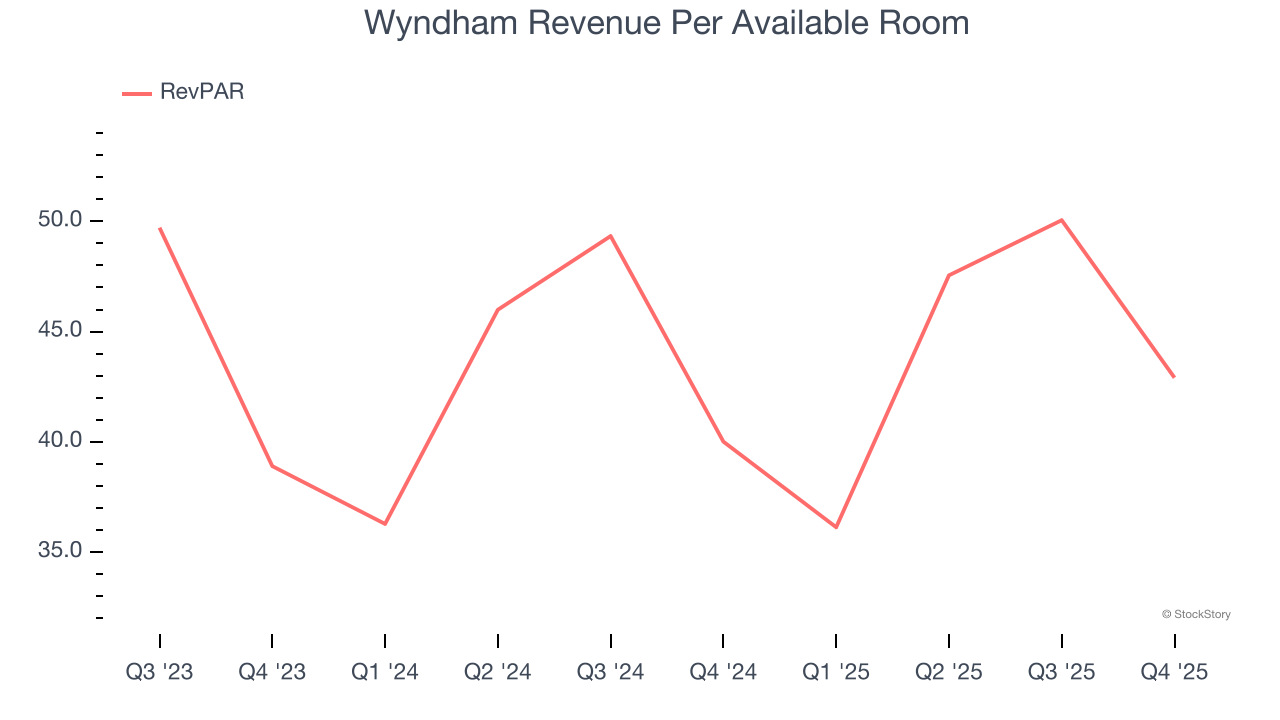

1. Weak RevPAR Growth Points to Soft Demand

Investors interested in Consumer Discretionary - Travel and Vacation Providers companies should track RevPAR (revenue per available room) in addition to reported revenue. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Wyndham’s demand characteristics.

Wyndham’s RevPAR came in at $42.91 in the latest quarter, and over the last two years, its year-on-year growth averaged 2.3%. This performance was underwhelming and suggests it might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

2. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Wyndham historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 11.8%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

3. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Wyndham’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

We see the value of companies helping consumers, but in the case of Wyndham, we’re out. That said, the stock currently trades at 16× forward P/E (or $78.47 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Wyndham

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.