Beer, wine, and spirits company Constellation Brands (NYSE: STZ) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 9.8% year on year to $2.22 billion. Its non-GAAP profit of $3.06 per share was 16.2% above analysts’ consensus estimates.

Is now the time to buy Constellation Brands? Find out by accessing our full research report, it’s free for active Edge members.

Constellation Brands (STZ) Q4 CY2025 Highlights:

- Revenue: $2.22 billion vs analyst estimates of $2.16 billion (9.8% year-on-year decline, 2.9% beat)

- Adjusted EPS: $3.06 vs analyst estimates of $2.63 (16.2% beat)

- Adjusted EBITDA: $807.2 million vs analyst estimates of $790.1 million (36.3% margin, 2.2% beat)

- Management reiterated its full-year Adjusted EPS guidance of $11.45 at the midpoint

- Operating Margin: 31.1%, down from 32.2% in the same quarter last year

- Free Cash Flow Margin: 16.7%, down from 18.5% in the same quarter last year

- Organic Revenue fell 2% year on year vs analyst estimates of 4.4% declines (243.4 basis point beat)

- Market Capitalization: $25 billion

Company Overview

With a presence in more than 100 countries, Constellation Brands (NYSE: STZ) is a globally renowned producer and marketer of beer, wine, and spirits.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $9.38 billion in revenue over the past 12 months, Constellation Brands is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To expand meaningfully, Constellation Brands likely needs to tweak its prices, innovate with new products, or enter new markets.

As you can see below, Constellation Brands struggled to increase demand as its $9.38 billion of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a tough starting point for our analysis.

This quarter, Constellation Brands’s revenue fell by 9.8% year on year to $2.22 billion but beat Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to decline by 3.6% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and implies its products will face some demand challenges.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

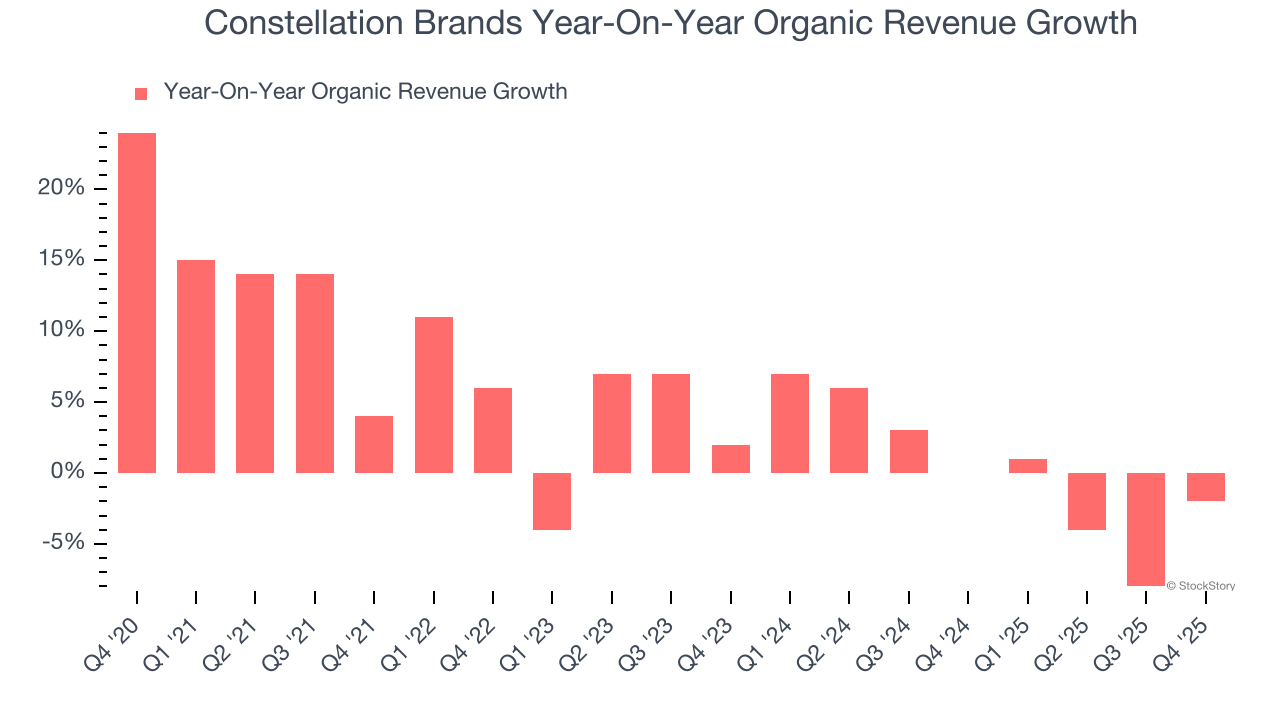

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Constellation Brands’s products has barely risen over the last eight quarters. On average, the company’s organic sales have been flat.

In the latest quarter, Constellation Brands’s organic sales fell by 2% year on year. This decline was a reversal from its historical levels. We’ll keep a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Constellation Brands’s Q4 Results

We enjoyed seeing Constellation Brands beat analysts’ organic revenue expectations this quarter. We were also glad its gross margin outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 1.9% to $144.20 immediately after reporting.

Indeed, Constellation Brands had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.