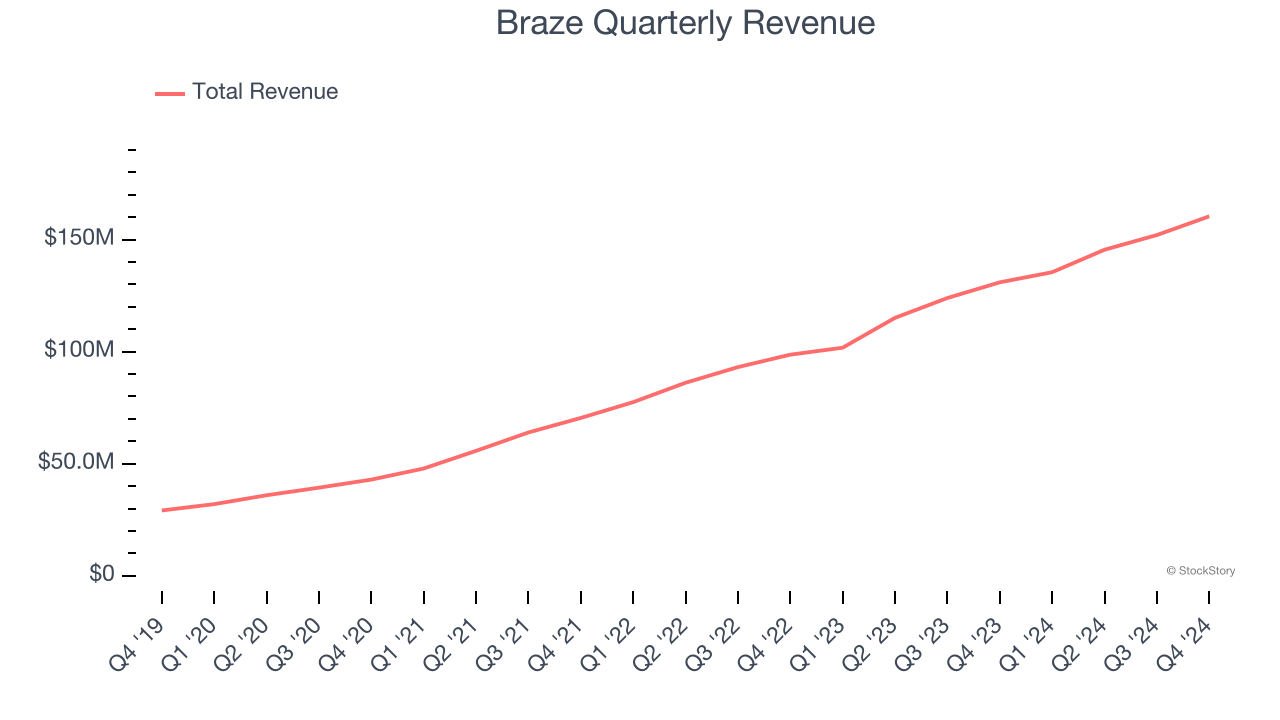

Customer engagement software provider Braze (NASDAQ: BRZE) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 22.5% year on year to $160.4 million. The company expects next quarter’s revenue to be around $158.5 million, close to analysts’ estimates. Its non-GAAP profit of $0.12 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Braze? Find out by accessing our full research report, it’s free.

Braze (BRZE) Q4 CY2024 Highlights:

- Revenue: $160.4 million vs analyst estimates of $155.7 million (22.5% year-on-year growth, 3% beat)

- Adjusted EPS: $0.12 vs analyst estimates of $0.05 (significant beat)

- Adjusted Operating Income: $7.95 million vs analyst estimates of $2.50 million (5% margin, significant beat)

- Management’s revenue guidance for the upcoming financial year 2026 is $688.5 million at the midpoint, in line with analyst expectations and implying 16% growth (vs 26.2% in FY2025)

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.33 at the midpoint, beating analyst estimates by 13.4%

- Operating Margin: -13.4%, up from -24.7% in the same quarter last year

- Free Cash Flow was $15.21 million, up from -$14.25 million in the previous quarter

- Customers: 2,296, up from 2,211 in the previous quarter

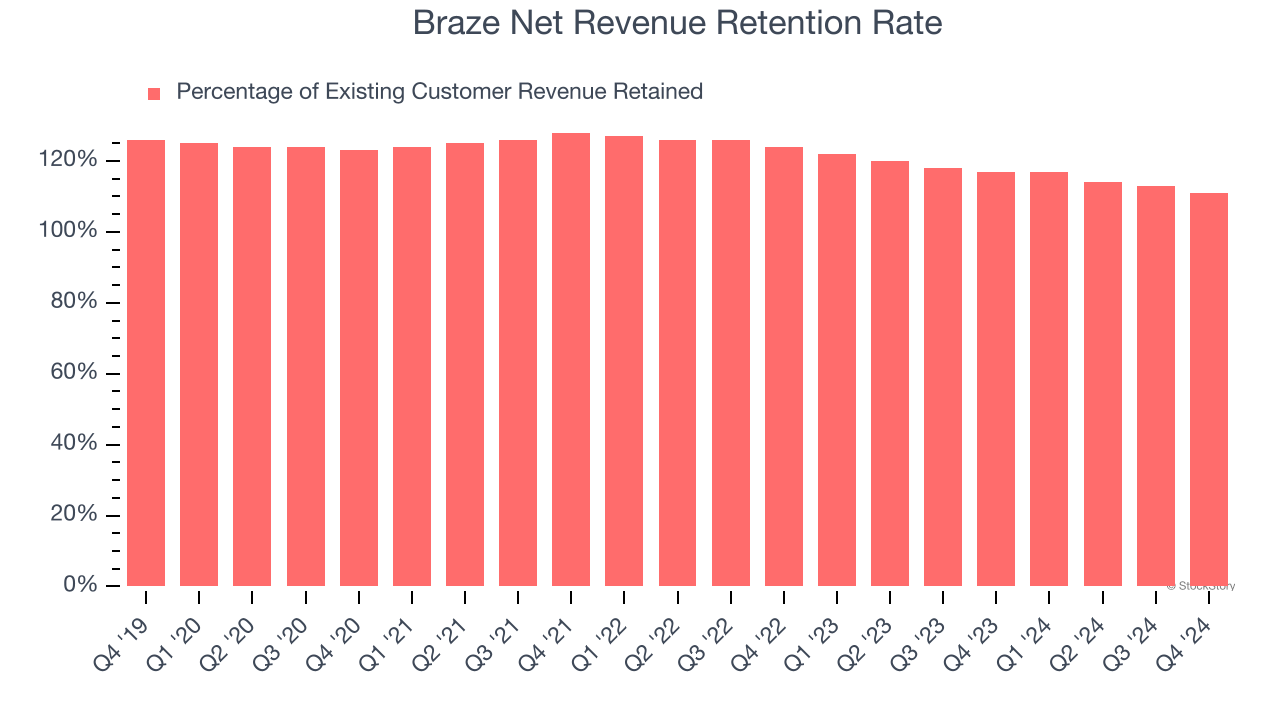

- Net Revenue Retention Rate: 111%, down from 113% in the previous quarter

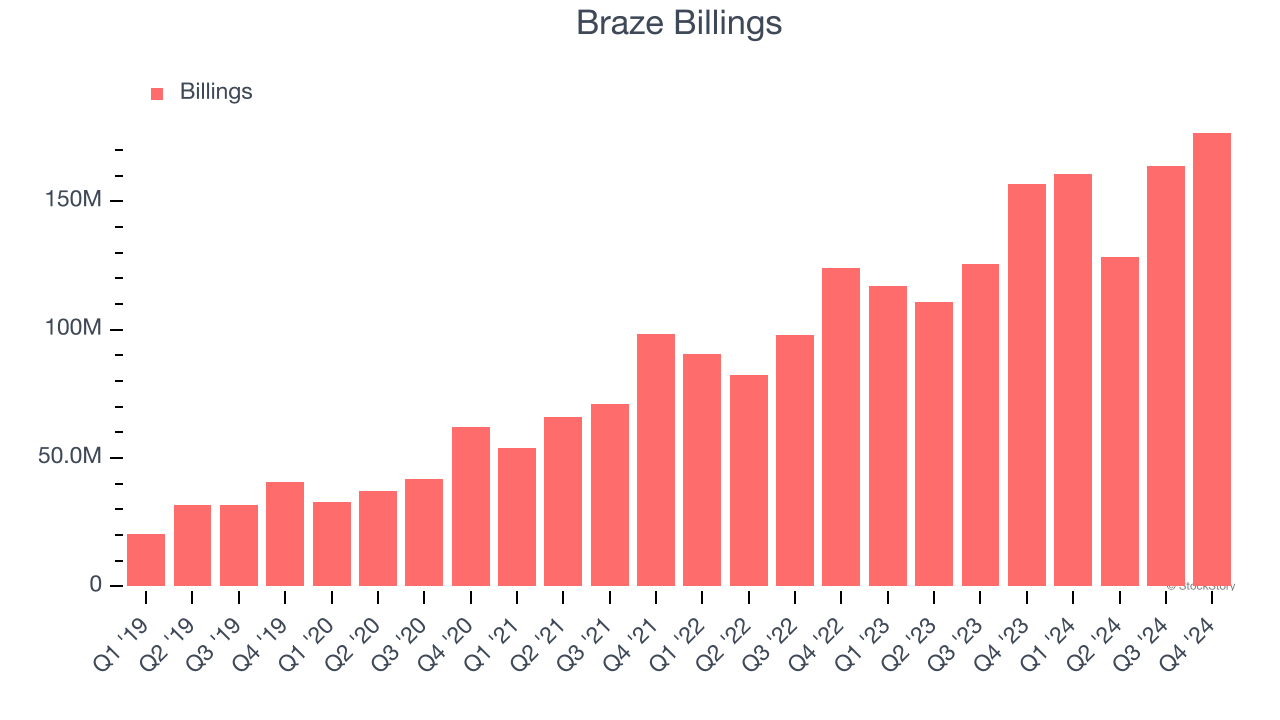

- Billings: $176.8 million at quarter end, up 12.8% year on year

- Market Capitalization: $3.86 billion

"Fiscal 2025 was a milestone year for Braze that reinforced our position as the leading Customer Engagement platform through robust customer growth and continued advancements in our product, including meaningful new investments in AI and machine learning. We grew revenue 26% while continuing to drive strong operating leverage, ending the year with three straight quarters of non-GAAP net income profitability,” said Bill Magnuson, Cofounder and CEO of Braze.

Company Overview

Founded in 2011 after the co-founders met at NYC Disrupt Hackathon, Braze (NASDAQ: BRZE) is a customer engagement software platform that allows brands to connect with customers through data-driven and contextual marketing campaigns.

Marketing Software

Whether or not companies market their products through social media, all businesses need to meet customers where they are; and increasingly, that is social media. As more and more people use a greater number of social media platforms, social media management software become more valuable to their customers.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, Braze grew its sales at an excellent 35.6% compounded annual growth rate. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, Braze reported robust year-on-year revenue growth of 22.5%, and its $160.4 million of revenue topped Wall Street estimates by 3%. Company management is currently guiding for a 17% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 15.9% over the next 12 months, a deceleration versus the last three years. Still, this projection is admirable and implies the market is baking in success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Braze’s billings punched in at $176.8 million in Q4, and over the last four quarters, its growth was impressive as it averaged 24% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Braze’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 114% in Q4. This means Braze would’ve grown its revenue by 13.7% even if it didn’t win any new customers over the last 12 months.

Despite falling over the last year, Braze still has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

Key Takeaways from Braze’s Q4 Results

We were impressed by Braze’s strong growth in customers this quarter, enabling it to beat analysts' revenue, EPS, and adjusted operating income estimates. We were also glad its full-year EPS guidance topped Wall Street’s estimates. On the other hand, its billings fell short. Still, this quarter had some key positives. The stock traded up 13.7% to $41.70 immediately after reporting.

Indeed, Braze had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.