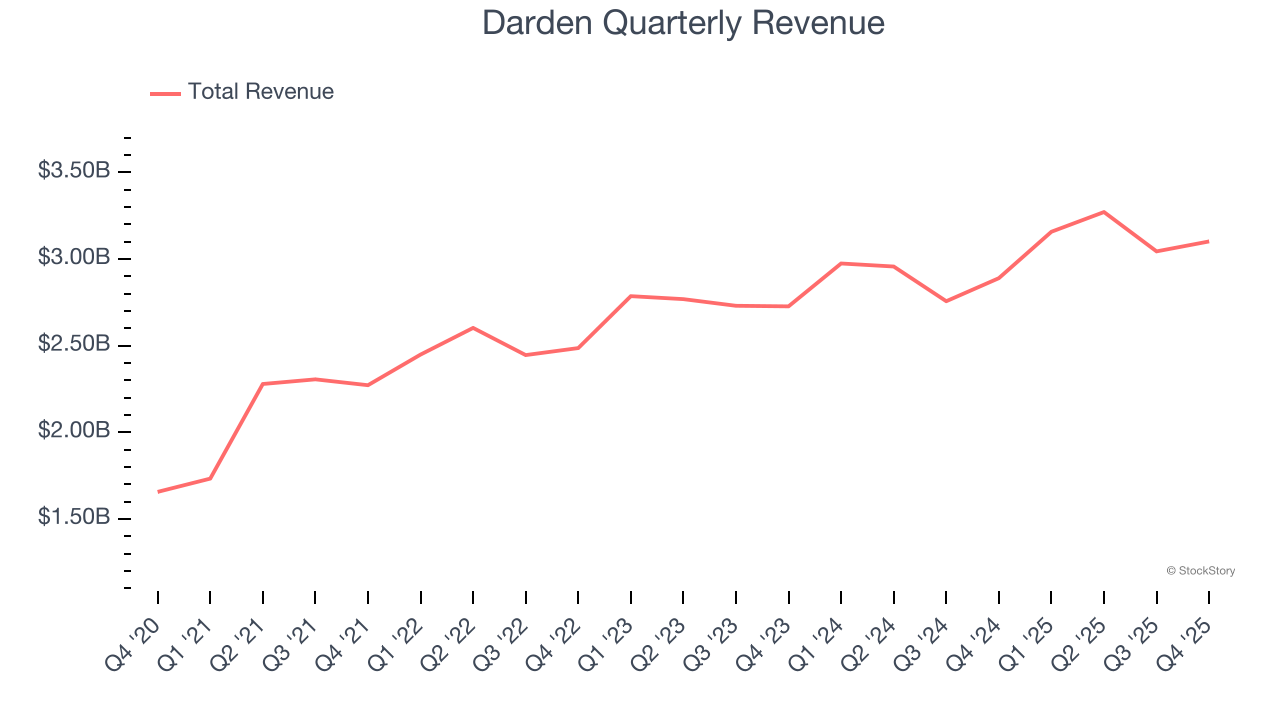

Restaurant company Darden (NYSE: DRI) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 7.3% year on year to $3.10 billion. Its non-GAAP profit of $2.08 per share was 0.8% below analysts’ consensus estimates.

Is now the time to buy Darden? Find out by accessing our full research report, it’s free for active Edge members.

Darden (DRI) Q4 CY2025 Highlights:

- Revenue: $3.10 billion vs analyst estimates of $3.07 billion (7.3% year-on-year growth, 1% beat)

- Adjusted EPS: $2.08 vs analyst expectations of $2.10 (0.8% miss)

- Adjusted EBITDA: $482.2 million vs analyst estimates of $465.7 million (15.5% margin, 3.5% beat)

- Management reiterated its full-year Adjusted EPS guidance of $10.60 at the midpoint

- Operating Margin: 10.3%, in line with the same quarter last year

- Free Cash Flow Margin: 3.4%, down from 7.6% in the same quarter last year

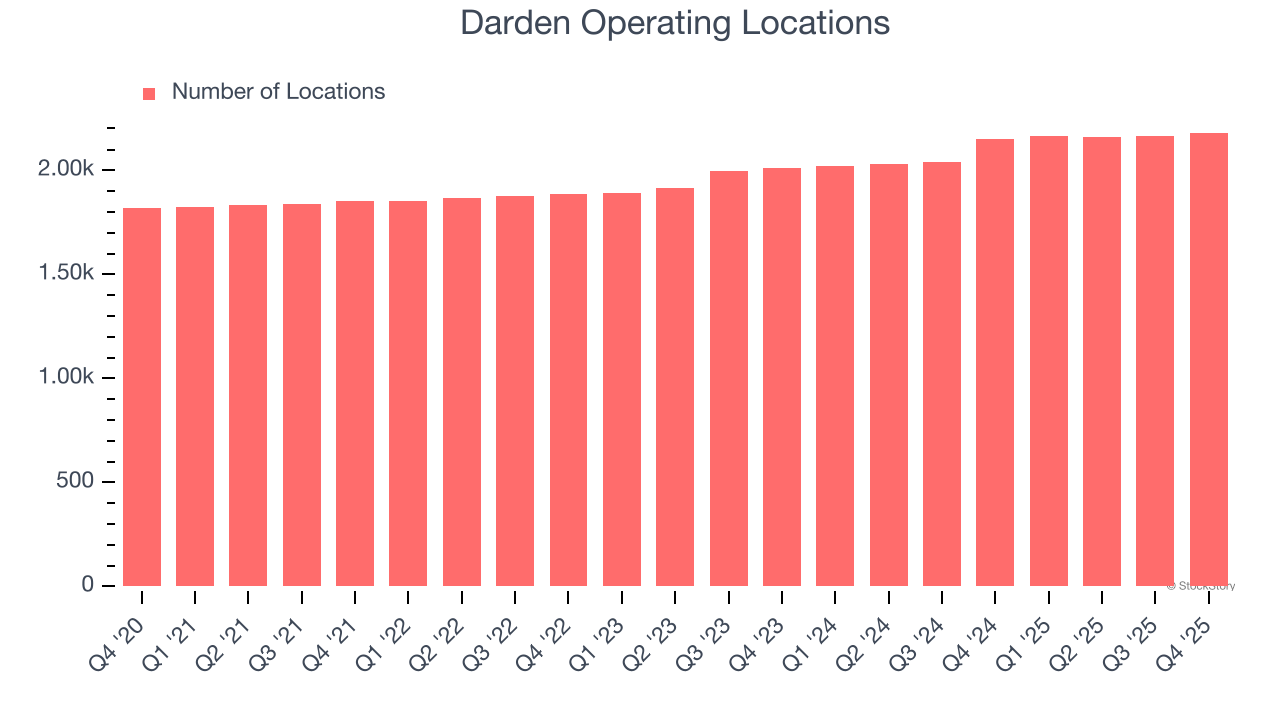

- Locations: 2,182 at quarter end, up from 2,152 in the same quarter last year

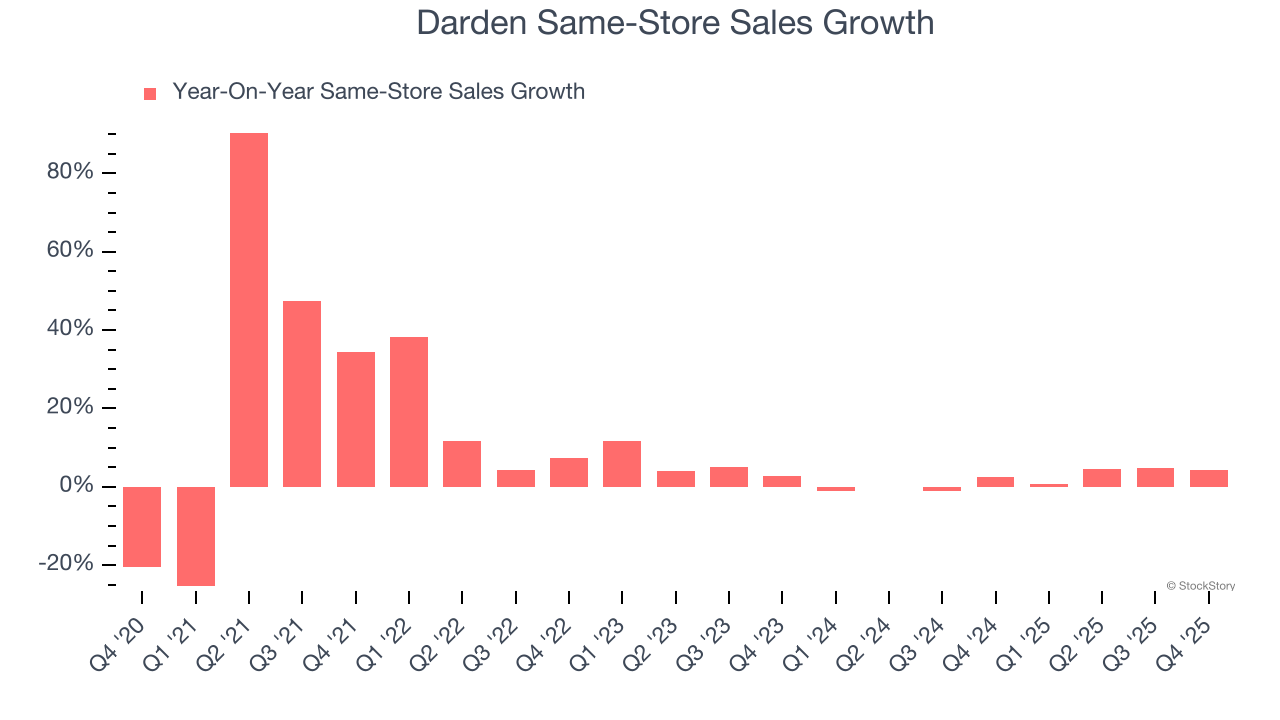

- Same-Store Sales rose 4.3% year on year (2.4% in the same quarter last year)

- Market Capitalization: $22.04 billion

"The second quarter exceeded our top-line expectations as every segment delivered positive same-restaurant sales," said Darden President & CEO Rick Cardenas.

Company Overview

Founded in 1968 as Red Lobster, Darden (NYSE: DRI) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $12.58 billion in revenue over the past 12 months, Darden is one of the most widely recognized restaurant chains and benefits from customer loyalty, a luxury many don’t have. Its scale also gives it negotiating leverage with suppliers, enabling it to source its ingredients at a lower cost. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing restaurant banners have penetrated most of the market. For Darden to boost its sales, it likely needs to adjust its prices, launch new chains, or lean into foreign markets.

As you can see below, Darden’s 6.4% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was mediocre as it barely increased sales at existing, established dining locations.

This quarter, Darden reported year-on-year revenue growth of 7.3%, and its $3.10 billion of revenue exceeded Wall Street’s estimates by 1%.

Looking ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, similar to its six-year rate. This projection doesn't excite us and suggests its newer menu offerings will not lead to better top-line performance yet.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Restaurant Performance

Number of Restaurants

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Darden operated 2,182 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 5.4% annual growth, much faster than the broader restaurant sector.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

Darden’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.8% per year. This performance suggests it should consider improving its foot traffic and efficiency before expanding its restaurant base.

In the latest quarter, Darden’s same-store sales rose 4.3% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Darden’s Q4 Results

We enjoyed seeing Darden beat analysts’ same-store sales expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 3.8% to $196.81 immediately after reporting.

Darden may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.