Quanta currently trades at $436.93 and has been a dream stock for shareholders. It’s returned 535% since December 2020, blowing past the S&P 500’s 82.9% gain. The company has also beaten the index over the past six months as its stock price is up 21.8% thanks to its solid quarterly results.

Is now still a good time to buy PWR? Or are investors being too optimistic? Find out in our full research report, it’s free for active Edge members.

Why Is PWR a Good Business?

A construction engineering services company, Quanta (NYSE: PWR) provides infrastructure solutions to a variety of sectors, including energy and communications.

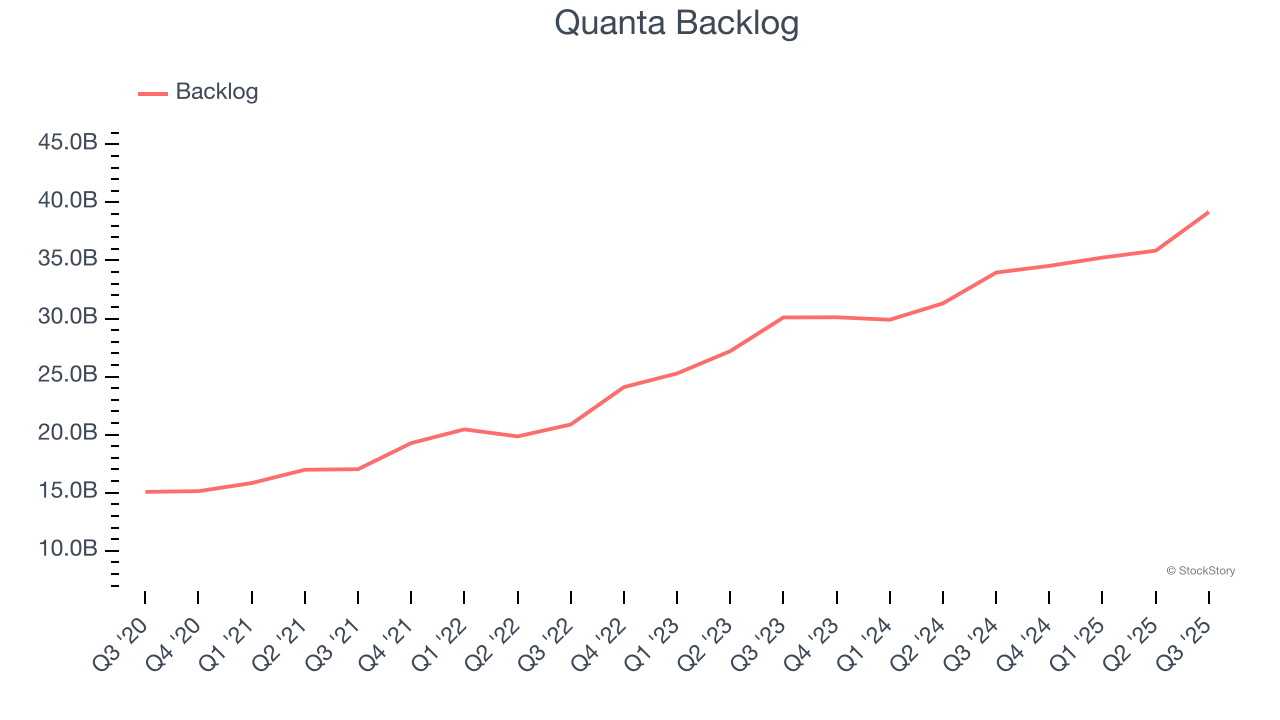

1. Surging Backlog Locks In Future Sales

We can better understand Energy Products and Services companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Quanta’s future revenue streams.

Quanta’s backlog punched in at $39.17 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 16.7%. This performance was fantastic and shows the company has a robust sales pipeline because it is accumulating more orders than it can fulfill. Its growth also suggests that customers are committing to Quanta for the long term, enhancing the business’s predictability.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Quanta’s revenue to rise by 12.8%. While this projection is below its 18% annualized growth rate for the past two years, it is particularly noteworthy for a company of its scale and implies the market sees success for its products and services.

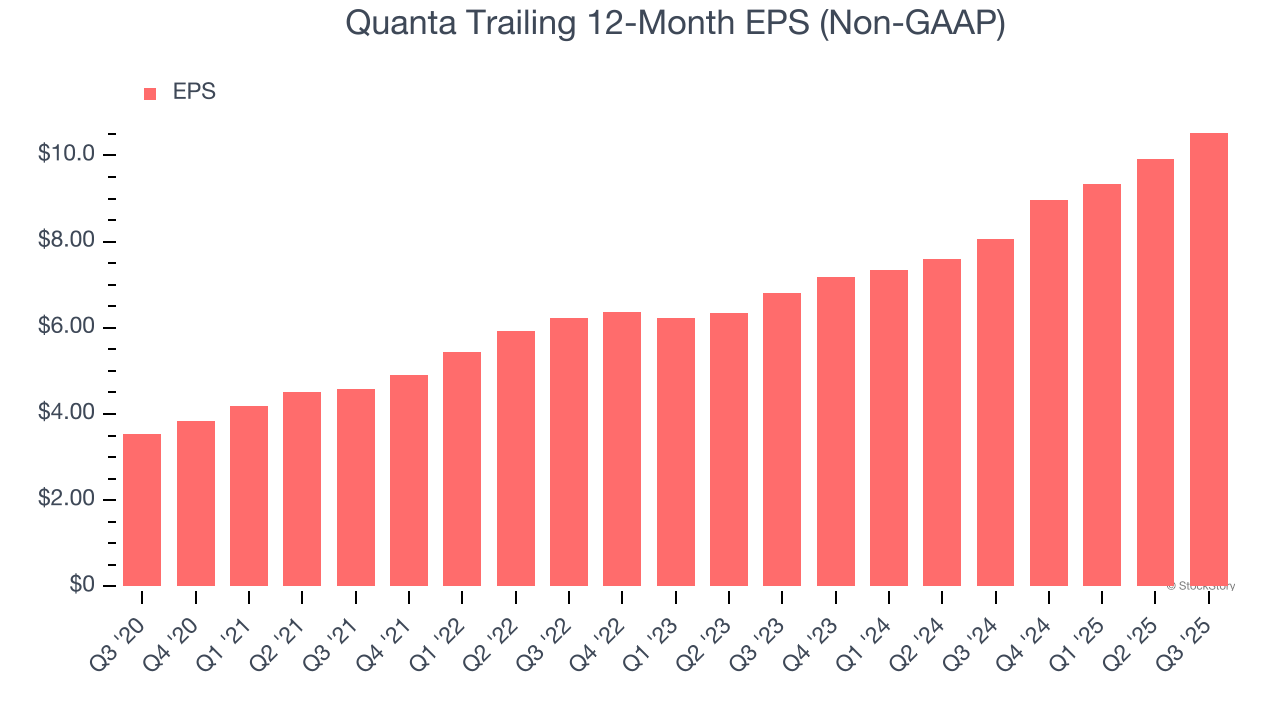

3. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Quanta’s EPS grew at an astounding 24.4% compounded annual growth rate over the last five years, higher than its 19% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we think Quanta is a high-quality business, and with its shares beating the market recently, the stock trades at 36.3× forward P/E (or $436.93 per share). Is now the right time to buy? See for yourself in our full research report, it’s free for active Edge members.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.