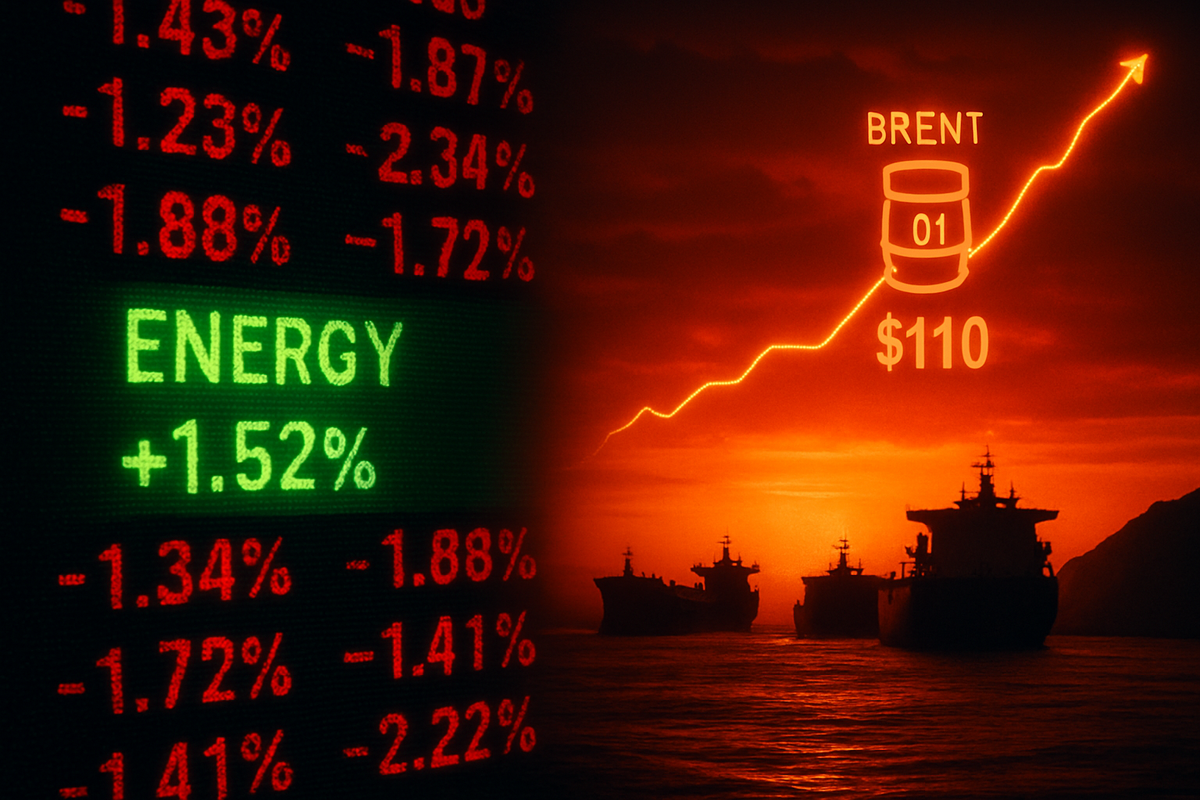

On a day marked by deepening anxiety and a sea of red across Wall Street, the Energy sector emerged as the sole bastion of growth in the S&P 500, closing up 1.52% on March 20, 2026. This stark divergence comes as the broader index fell nearly 0.84%, breaking below critical support levels and ending its fourth consecutive week of losses. Investors are fleeing to the perceived safety of "hard assets" as a violent geopolitical escalation in the Middle East threatens to choke off a fifth of the world’s oil supply, sending Brent crude prices on a parabolic trajectory toward historic highs.

The immediate implications of this market split are profound, signaling a return to the high-inflation, low-growth "stagflation" fears that have haunted the global economy for years. While the energy surge provides a temporary hedge for commodity-heavy portfolios, the rising cost of Brent crude—which settled near $108.65 per barrel today after a mid-month peak of $120—is acting as an "implicit tax" on the American consumer. With diesel and jet fuel prices skyrocketing, the rest of the S&P 500 is grappling with the reality of compressed margins and a potential slowdown in discretionary spending.

A Month of Escalation: The Strait of Hormuz Crisis

The current market volatility is the direct result of a rapid military escalation known as the "Strait of Hormuz Crisis," which began in late February 2026. The spark was ignited on February 28 during "Operation Epic Fury," a coordinated series of U.S. and Israeli airstrikes targeting Iranian nuclear infrastructure and military command centers following a definitive collapse in regional diplomacy. This move prompted an immediate and asymmetrical response from Iran, which initiated a maritime blockade of the Strait of Hormuz—the world’s most vital oil artery—and launched drone strikes against key regional energy hubs.

As of today, March 20, the impact on global supply remains catastrophic. Major infrastructure, including Qatar’s Ras Laffan industrial complex, Saudi Arabia’s SAMREF refinery (NYSE: ARMCO), and the UAE’s al-Hosn gas field, have reported significant damage or operational suspensions. By removing an estimated 7 to 10 million barrels of oil per day from the global market practically overnight, the conflict has created a supply vacuum that the International Energy Agency (IEA) has struggled to fill. The initial market reaction was one of panic, with Brent crude skyrocketing from a stable $72 per barrel in late February to its current elevated levels.

Key stakeholders, including the U.S. Treasury and the Department of Energy, have spent the last three weeks in emergency sessions. The closure of the Strait has not only halted physical oil shipments but has also triggered "actuarial warfare," where maritime insurance providers have withdrawn coverage for any vessels operating in the Persian Gulf. This has effectively rendered the region impassable for commercial shipping, forcing tankers to reroute around the Cape of Good Hope, adding weeks to transit times and doubling freight rates for global commerce.

Winners in the Oil Patch and Losers in the Skies

The 1.52% gain in the energy sector today was led by domestic giants and infrastructure plays that are positioned to benefit from the supply crunch. Oneok, Inc. (NYSE: OKE) was among the top performers, gaining over 4%, while Chevron Corp (NYSE: CVX) mirrored the sector's overall rise with a 1.52% jump. Occidental Petroleum Corp (NYSE: OXY) has continued its month-long rally, having gained nearly 7% this week alone as investors bet on its significant domestic production capacity. Meanwhile, Cheniere Energy, Inc. (NYSE: LNG) saw its shares remain near all-time highs as the disruption of Qatari LNG exports redirected global gas demand toward American liquefaction terminals.

Conversely, the transportation and logistics sectors are bearing the brunt of the "energy tax." American Airlines Group Inc. (NASDAQ: AAL) has been the hardest hit among carriers, as its unhedged fuel strategy left it fully exposed to the 85% surge in jet fuel prices since the conflict began. Similarly, United Airlines Holdings (NASDAQ: UAL) and Delta Air Lines, Inc. (NYSE: DAL) saw their stock prices slide today as analysts slashed earnings estimates for the remainder of 2026. The rising cost of fuel is not just a problem for airlines; trucking giant Schneider National, Inc. (NYSE: SNDR) has seen its value erode as diesel prices at the pump jumped by an average of $1.25 per gallon in just two weeks.

Logistics heavyweights like FedEx Corp. (NYSE: FDX) and United Parcel Service, Inc. (NYSE: UPS) have been forced to implement massive fuel surcharges, reaching upwards of 34% for international air exports. These surcharges are being passed directly to retailers and consumers, further dampening the outlook for the Consumer Discretionary sector, which fell 2.6% today. For these companies, the "win" for energy represents a direct "loss" in operating margin, as the cost of moving goods around the globe reaches levels not seen in decades.

Historical Precedents and Systemic Paralysis

The 2026 Strait of Hormuz Crisis is already being compared to the 1973 Oil Embargo and the 1979 Iranian Revolution, though many analysts argue the current situation is more dangerous. While the 1973 crisis saw a 5% reduction in global supply, the 2026 blockade has effectively removed 20% of the world’s oil and a similar share of its liquefied natural gas. The scale of the disruption is nearly four times that of the supply shocks seen during the 2022 invasion of Ukraine, making this the most significant energy event of the 21st century.

Furthermore, this event fits into a broader trend of geopolitical fragmentation and the "weaponization" of supply chains. Unlike past crises where the threat was purely physical, the 2026 conflict has leveraged the global financial and insurance systems to paralyze trade. The withdrawal of maritime insurance has created a "phantom blockade," where even if the Strait were physically clear, no ship could afford to sail through it. This systemic paralysis has ripple effects on every industry from agriculture to technology, as the cost of the plastic, fuel, and electricity needed for production enters a period of extreme volatility.

Regulatory and policy implications are also mounting. The U.S. government has been forced to consider unprecedented measures, such as a broad 60-day waiver of the Jones Act to allow foreign-flagged vessels to transport fuel between U.S. ports to ease domestic bottlenecks. There are also whispers in Washington about "un-sanctioning" millions of barrels of Iranian oil currently held in offshore storage—a paradoxical move that highlights the desperation of the current administration to stabilize global prices before the upcoming election cycle.

The Road Ahead: SPR Depletion and Strategic Pivots

Looking forward, the market’s attention is fixed on the U.S. Strategic Petroleum Reserve (SPR), which entered this crisis at a historic low of roughly 413 million barrels—only 60% of its capacity. President Trump has authorized a massive 172-million-barrel drawdown over the next 120 days, but experts warn of "flow rate" limits. The SPR can only pump about 2 million barrels per day into the market, which offsets only a fraction of the 20-million-barrel shortfall caused by the Middle East blockade. This suggests that high energy prices may be a permanent fixture for the remainder of 2026.

In the long term, this crisis may force a strategic pivot in how global corporations manage energy risk. Companies that have historically ignored fuel hedging are now scrambling to enter derivative markets, potentially driving even more volatility into energy futures. For the energy sector itself, the challenge will be to translate these short-term price spikes into long-term infrastructure investment. However, with the threat of further military escalation always present, the "geopolitical risk premium" on oil is likely to remain embedded in the market for the foreseeable future.

Market opportunities may emerge for renewable energy providers and domestic energy services, as the unreliability of Middle Eastern supply accelerates the shift toward energy independence. However, the short-term challenge remains the "demand destruction" caused by $110 oil. If Brent crude continues its climb toward the $130 mark, economists warn that a global recession by the third quarter of 2026 may be unavoidable, as the consumer's ability to absorb higher costs reaches its breaking point.

Final Assessment: A Fragile Equilibrium

As we wrap up a tumultuous day on the markets, the key takeaway is the sheer fragility of the global supply chain. The Energy sector's 1.52% gain today is less a sign of industrial health and more a symptom of a world in crisis. While investors in Exxon Mobil Corp (NYSE: XOM) or Chevron may find solace in today’s green numbers, the broader market remains in a state of high alert. The "Hormuz Premium" is now the primary driver of global equity valuations, overshadowing traditional metrics like corporate earnings or interest rate forecasts.

Moving forward, the market will be hyper-sensitive to any news regarding the insurance status of Gulf tankers or the success of the SPR drawdown. Investors should watch for the performance of the "losers"—the airlines and shipping companies—as their ability to survive this fuel spike will be the ultimate barometer for the health of the global economy. For now, Energy remains the only game in town, but it is a game played on the edge of a geopolitical precipice.

This content is intended for informational purposes only and is not financial advice.