Cybersecurity company Palo Alto Networks (PANW) received a boost after its CEO, Nikesh Arora, disclosed buying $10 million worth of the company’s stock, boosting his direct stake by more than 24% through an open-market purchase of 68,085 shares.

JPMorgan analysts also viewed this as a bullish signal, calling the move a “substantial vote of confidence.” Analyst Brian Essex believes that the stock’s selloff has moved beyond reason, and this insider support looks encouraging.

Should you do the same and load up on Palo Alto Networks’ stock?

About Palo Alto Networks Stock

Headquartered in Santa Clara, California, Palo Alto Networks is a leading American multinational cybersecurity company, specializing in operations centered on next-generation firewalls, cloud-based security platforms, and integrated solutions that enable Zero Trust architectures for worldwide enterprises.

The company delivers threat intelligence, AI-driven security operations, and real-time cloud protection, helping organizations secure networks, applications, and data across hybrid environments through innovative platforms and expert services. Palo Alto Networks has a market capitalization of $131.1 billion.

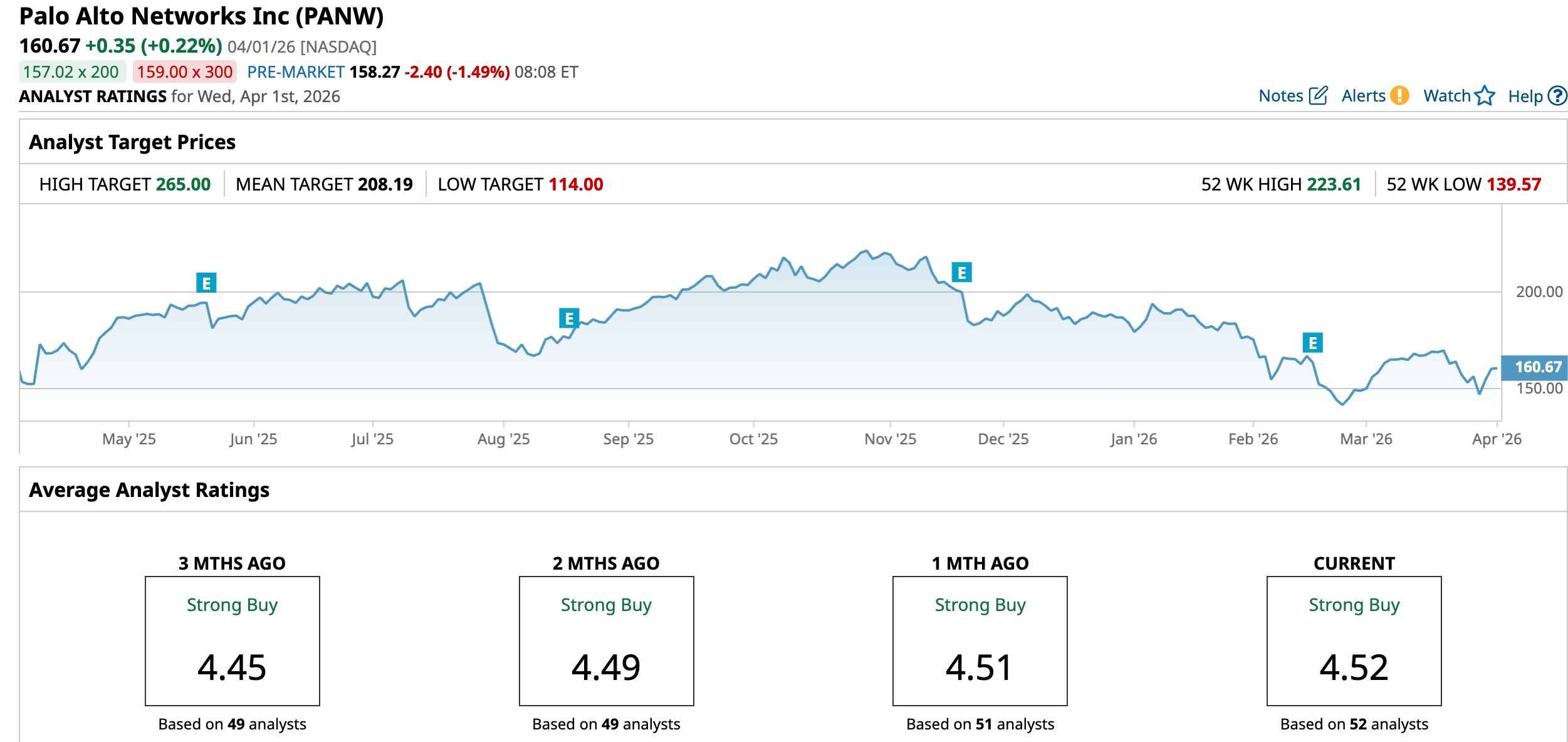

Palo Alto Networks is going through a tough time on Wall Street as its FY2026 forecast has weighed on sentiment. Moreover, the company’s aggressive acquisition spree has created concerns about its margin growth. Over the past 52 weeks, Palo Alto Networks’ stock has declined by 6.2%, and it is down 12.77% year-to-date (YTD). However, the stock is up 4.86% over the past five days due to its CEO’s purchase. Its shares reached a 52-week low of $139.57 on Feb. 24, but are up 15.12% from that level.

On a forward-adjusted basis, Palo Alto Networks’ price-to-earnings (non-GAAP) ratio of 43.53 times is considerably higher than the industry average of 21.41 times.

Palo Alto Networks' Acquisition Spree

Palo Alto Networks has been on an aggressive buying spree over the past year. The spree began last summer with the purchase of Protect AI, an AI application and model security platform. As the company’s customers rush to adopt AI, the security risks pile up. Therefore, this acquisition addresses the need to secure the entire AI ecosystem.

Palo Alto Networks followed this purchase with the acquisition of Chronosphere, which addresses the challenge of being unable to see the huge data volumes that power modern businesses and secure them efficiently. Customers gain real-time visibility into the AI systems that drive applications.

The following month, in February, Palo Alto Networks entered the identity security market through the acquisition of CyberArk, helping the company secure identities across the enterprise, either human, machine, or agentic. While CyberArk would have a stand-alone platform, Palo Alto Networks would also integrate the acquired company’s offerings into its own security platform.

Now, Palo Alto Networks is gearing up to acquire Koi, an agentic endpoint security firm. As the endpoint attack surface evolves beyond traditional executables, agentic endpoint security becomes increasingly important. Additionally, the company’s Prisma AIRS is expected to be integrated with Koi’s agentic endpoint security capabilities.

Palo Alto Networks Reported Better-Than-Expected Second-Quarter Results

For the second quarter of fiscal 2026 (quarter ended Jan. 31), Palo Alto Networks reported $2.59 billion in revenues, increasing 14.9% year-over-year (YOY). This growth was largely driven by subscription and service growth. This top line figure was slightly better than the $2.58 billion that Street analysts had expected.

Its non-GAAP operating margin grew YOY from 28.4% to 30.3%. The company’s non-GAAP net income per share increased by 27.2% from the prior-year period to $1.03, exceeding the $0.93 figure that analysts had expected. Additionally, PANW reported that its next-generation security ARR grew 33% YOY to $6.30 billion, while its RPO grew 23% to $16 billion.

However, the acquisition spree is expected to put pressure on the company’s bottom line, as Palo Alto Networks lowered its fiscal 2026 non-GAAP EPS forecast from $3.80-$3.90 to $3.65-$3.70. Street analysts have a cooler prediction, expecting an EPS of $2.14, up 30.5% YOY for fiscal 2026.

What Analysts Think About Palo Alto Networks' Stock

Last month, analysts at Wells Fargo initiated coverage on Palo Alto’s stock with a bullish “Overweight” rating and a $200 price target. Wells Fargo analysts believe the selloff in Palo Alto Networks’ stock has created a favorable entry point, given the company's exposure to almost every cybersecurity space’s secular trend.

In a different release, JPMorgan analysts kept an “Overweight” rating on the stock but cut the price target from $225 to $200 after the company’s Q2 earnings release. Analysts also highlighted a contraction in the peer multiple.

In February, Citi analyst Fatima Boolani lowered Palo Alto Networks’ price target from $235 to $210, but kept a “Buy” rating on the stock, viewing the company’s earnings as “noisy.” Furthermore, Stifel analysts took the same steps, keeping a “Buy” rating but cutting the price target from $200 to $185, noting that Q2 results had several moving parts due to its acquisitions.

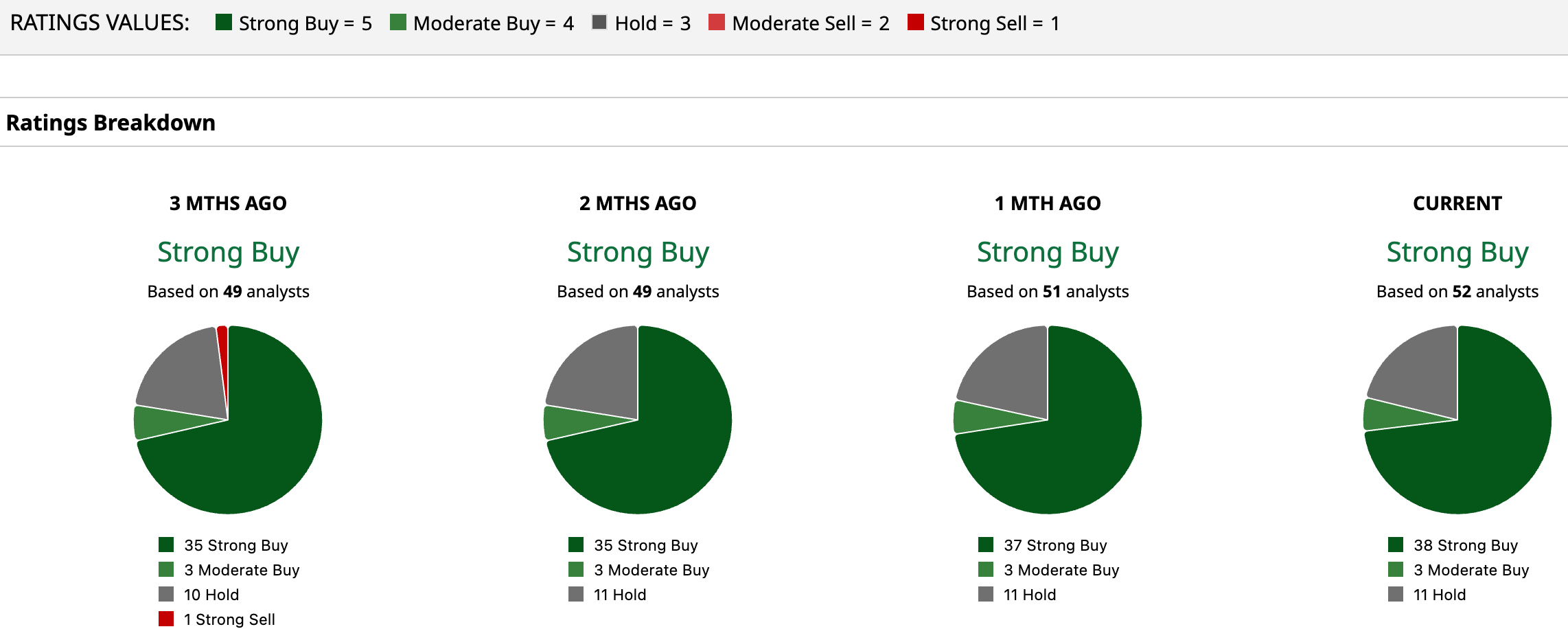

Palo Alto Networks is gaining some praise on Wall Street, with analysts awarding it a consensus “Strong Buy” rating. Of the 52 analysts rating the stock, a majority of 38 analysts have rated it a “Strong Buy,” three analysts suggest a “Moderate Buy,” while 11 analysts are playing it safe with a “Hold” rating. The consensus price target of $208.19 represents a 29.6% upside from current levels. The Street-high price target of $265 indicates a 64.9% upside.

Key Takeaways

Bullish sentiment, especially from analysts and investors, suggests that more upside may remain. The company is also a beneficiary of the AI-driven shift in the cyberthreat landscape, and the acquisitions point to a robust push into enterprise-wide security. Therefore, Palo Alto Networks might be a buy now.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why the Best Space Stock to Buy, as Artemis II Heads for the Moon, Could Be 1 Company You Probably Have Never Heard Of

- Sandisk Was the Top-Performing S&P 500 Stock in Q1. Can SNDK Continue Its Run in Q1?

- Iran Identifies Palantir as a ‘Legitimate Target’ for Threatened Attacks: Should You Sell PLTR Stock Now?

- Boeing Is Stacking Wins, But Is It Still Too Risky to Buy?