AI is having a clear effect on how companies think about dividends in corporate America. In 2026 alone, companies tied to artificial intelligence infrastructure have been raising their payouts at a pace that would have looked unusually strong just a few years ago.

GE Aerospace (GE) raised its quarterly dividend by 31%, Monolithic Power Systems (MPWR) increased its payout by 28%, and Equinix (EQIX) lifted its dividend by 10%, while also committing to grow it by at least 8% a year for the next five years. These are not small increases. They show that companies benefiting from AI demand are bringing more of that cash back to shareholders.

Applied Materials (AMAT) just sent a similar message. On March 13, 2026, the company's board of directors approved a 15% increase to its quarterly cash dividend, raising it from $0.46 to $0.53 per share, payable June 11, 2026. That move marks nine straight years of dividend growth.

CFO Brice Hill said the company has more than doubled its dividend per share over the past four years, with the payout growing at an 18% annual rate over the last decade. Over the past 10 fiscal years, Applied has also returned nearly 90% of its free cash flow to shareholders through dividends and share buybacks combined.

That kind of record from a chip equipment company deeply tied to the AI chip market raises a fair question: with AMAT's dividend growing faster than most and its business becoming more important to the future of chip manufacturing, is this a stock worth owning right now? Let’s find out.

The Numbers Behind the Bull Case for AMAT

Applied Materials makes the tools chip companies use to produce advanced semiconductors, and it makes most of its money by selling wafer fabrication equipment while also generating high-margin recurring revenue from services and spare parts over the life of those tools.

Over the past 52 weeks, AMAT stock has jumped 124%, with another 35% gain year-to-date (YTD).

That strong run also shows up in valuation, with AMAT trading at a forward P/E of 30.76x compared with about 21.31x for its sector.

Income investors are getting something here, too. The stock has an annual dividend yield of 1.84% based on its most recent quarterly dividend of $0.46 per share, and that points to a forward payout ratio of just 18.77%, with nine straight years of dividend increases and a quarterly payout schedule that looks solid against the technology sector’s average yield of 1.37%.

On the financial side, AMAT generated annual sales of $28.37 billion and net income of $6.998 billion, while its 60-month beta of 1.65 shows the stock can be volatile but also tends to respond strongly when the cycle turns up. In its latest quarter, revenue came in at $7.01 billion, down 2% from a year ago, but margins remained strong, with GAAP gross margin at 49.0% and non-GAAP gross margin at 49.1%. GAAP EPS was $2.54, and non-GAAP EPS was $2.38, up 75% and flat year-over-year (YoY), respectively.

Semiconductor Systems posted record DRAM revenue, Applied Global Services delivered record services and spares revenue, and the company generated $1.69 billion in cash from operations while returning $702 million to shareholders through $337 million in buybacks and $365 million in dividends.

Why Applied Materials Still Has Room to Grow

Applied Materials is working with Micron Technology (MU) to develop next-generation DRAM, high-bandwidth memory (HBM), and NAND for AI systems, bringing together Applied’s EPIC Center in Silicon Valley and Micron’s innovation center in Boise to support the U.S. semiconductor pipeline. The two companies are working on new materials, process technologies, and advanced packaging to build high-bandwidth, low-power memory solutions for demanding AI workloads.

Applied is also in a long-term R&D partnership with SK Hynix focused on next-generation DRAM and HBM for AI and high-performance computing, with engineers from both companies working together at the EPIC Center. That work is centered on new materials, more complex integration approaches, and HBM-class advanced packaging to improve both performance and manufacturability as memory designs move beyond current nodes. It also connects with Applied’s advanced packaging R&D capabilities in Singapore.

On the logic side, Applied is introducing new deposition, etch, and materials modification systems built to improve the performance of leading-edge logic chips at 2 nm and beyond. These tools support the shift to gate-all-around (GAA) transistors and angstrom-class nodes, delivering atomic-scale improvements that account for a meaningful share of the total energy-efficient performance gains in each GAA process transition.

What Wall Street Sees Next for AMAT Stock

Next earnings are due on May 21, 2026, and Wall Street is already looking for $2.66 in earnings per share for the current quarter ending April 2026, up 11.30% from the $2.39 reported in the same quarter last year. Expectations keep rising from there. Q3 estimates stand at $2.86, which would be up 15.32% YoY, while full-year fiscal 2026 earnings are projected at $10.96, up 16.35% from fiscal 2025's $9.42. For fiscal 2027, analysts expect $13.69, which points to another 24.91% growth.

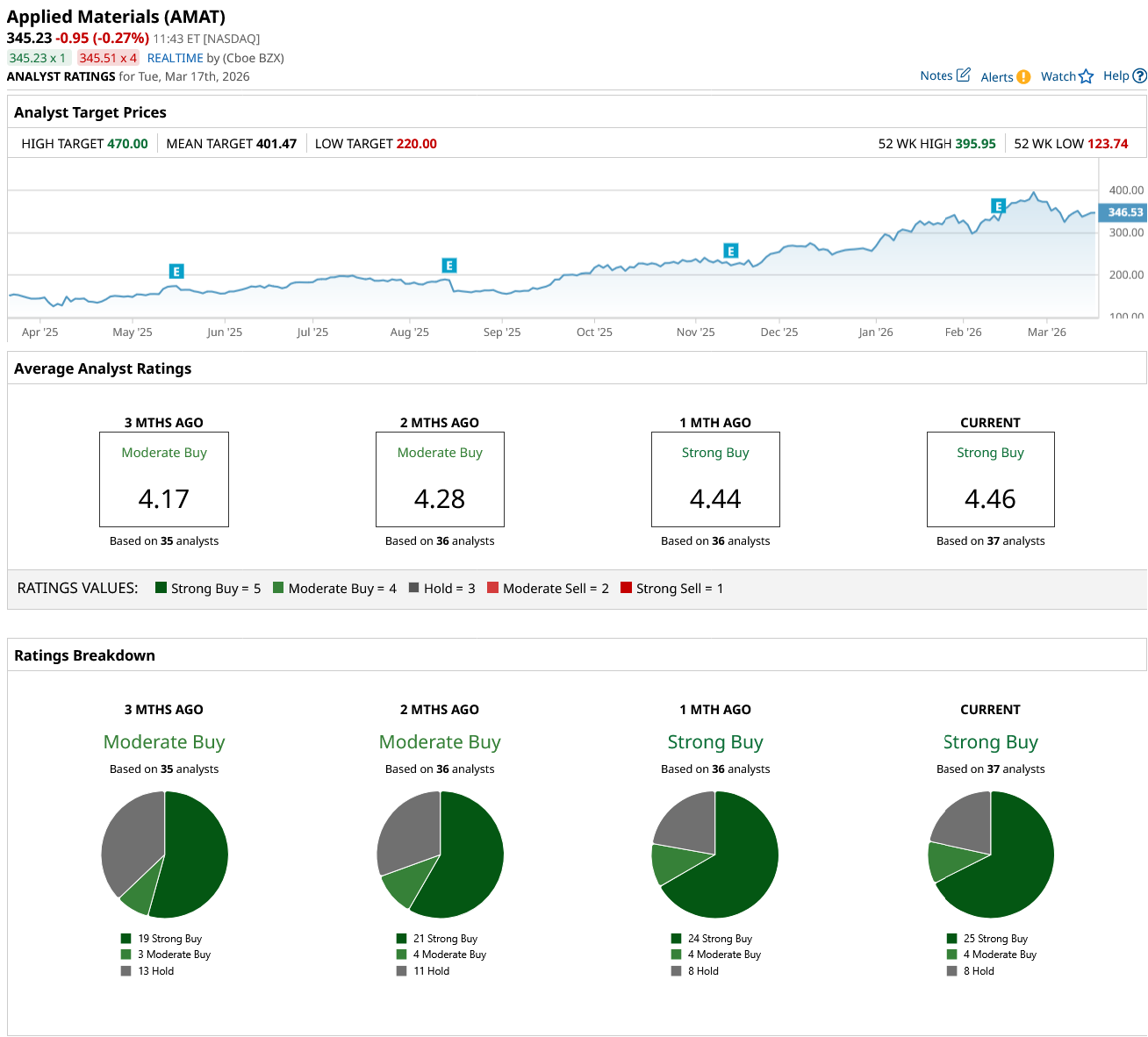

Deutsche Bank analyst Melissa Weathers upgraded AMAT to "Buy" from "Hold" and set a $390 price target, pointing to a more favorable environment for wafer fabrication equipment spending. She also said her own earnings estimates are about 10% above Wall Street consensus, which suggests she sees room for Applied Materials to outperform even the current forecasts. Her upgrade came after similar bullish calls earlier in the month from Susquehanna and Barclays, while KeyBanc also lifted its price target to $380.

The broader analyst view is just as positive. All 37 analysts covering AMAT currently rate it a consensus "Strong Buy." The average price target is $401.47, and compared with the current share price, that implies roughly 14% upside from current levels.

Conclusion

So, should you buy AMAT stock? Based on everything the numbers say, the answer leans yes for investors with a medium- to long-term horizon. A payout ratio under 19%, nine straight years of dividend increases, unanimous analyst conviction, accelerating earnings growth through 2027, and a front-row seat to the AI memory buildout through partnerships with Micron and SK Hynix. The premium valuation is real, but the earnings trajectory arguably justifies it. With the Street's average price target implying over 17% upside and one of the most cash-generative business models in semiconductors, the path of least resistance for AMAT shares still looks higher.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Applied Materials Raises Its Dividend 15%, Should You Buy AMAT Stock?

- 'The Miami Cab Driver Is Bearish on Software Stocks': Why You Should Buy the Dip in These 5 Oversold Names Now

- Delta Air Lines Just Broke Above Its 200-Day Moving Average. Should You Buy DAL Stock Here?

- Stop Fighting Time Decay: How Credit Spreads Change the Game for Options Traders