UnitedHealth Group (UNH) was one of the worst-performing large-cap stocks of 2025. For the full year, shares fell roughly 33%.

This was due to several setbacks, including allegations of fraud and misconduct related to its billing practices, unexpectedly higher medical costs — particularly within its Medicare programs — and weak earnings results accompanied by poor forward guidance. On top of all of that, the company's CEO abruptly resigned.

Adding to the pressure, a U.S. Senate committee investigating the company’s practices found that UnitedHealth used “aggressive tactics” to collect diagnosis data that boosted Medicare Advantage payments.

The report concluded that the insurer had “turned risk adjustment into a business, which was not the original intent.”

The Wall Street Journal also reported that some of the added diagnoses triggered billions of dollars in federal payments, noting that several of the diagnoses were questionable or inaccurate. In some cases, patients allegedly never received treatment for the additional conditions.

Separately, UnitedHealth is facing a renewed federal probe into allegations that it paid nursing homes thousands of dollars to limit the transfer of seriously ill residents to hospitals.

However, despite these ongoing, severe challenges — and the accompanying erosion of public trust — many Wall Street analysts remain bullish on the stock.

The Bull Case for UNH Stock

UnitedHealth appears confident in its future and has kept its dividend intact. The company recently paid a quarterly dividend of $2.21 per share, marking 24 years of dividend payments. Its annual dividend yield of 2.6% is more than double the S&P 500 SPDR’s (SPY) 1.05% yield.

Even with UnitedHealth's ongoing issues, Evercore ISI analyst Elizabeth Anderson says most of the chaos has been priced into the stock. With an “Outperform” rating and a $400 price target, the analyst argues that 2026 is a year of stabilization. She also says that, as margins normalize and execution improves, the stock should see a clear recovery moving forward.

RBC Capital reiterated an “Outperform” rating on UNH with a $408 price target, citing confidence in the company’s strategic execution. Analysts at Bernstein also reiterated an “Outperform” rating on the stock with a price target of $444, citing an attractive valuation.

Analysts Are Optimistic Ahead of Earnings

Analysts are cautiously optimistic about UNH ahead of fourth-quarter earnings, scheduled for release on Jan. 27.

At the moment, Wall Street expects UnitedHealth to post adjusted earnings per share (EPS) of $2.09, down about 69% from the $6.81 posted last year. For fiscal 2025, UNH is expected to post adjusted EPS of $16.30 a share, a 41% drop year-over-year from $27.66 in fiscal 2024. Adjusted EPS is expected to grow about 8% year-over-year to $17.60 in fiscal 2026.

While short-term challenges exist, analysts are hopeful that strategic changes and market dynamics will lead to a stronger financial performance.

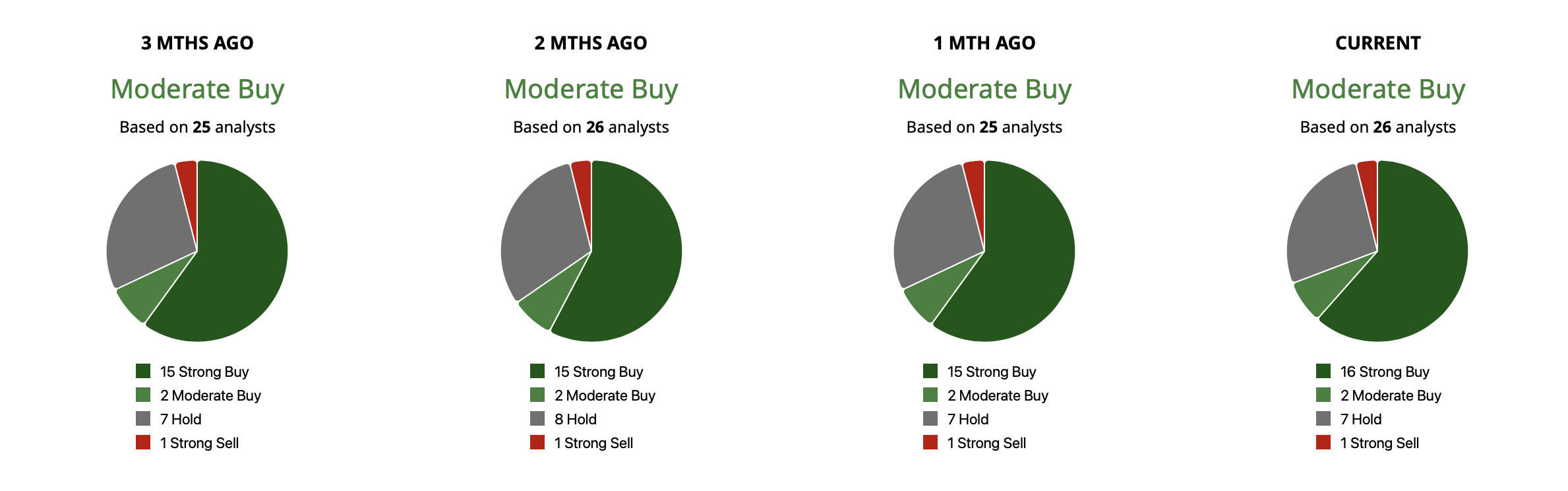

Overall, UNH has a “Moderate Buy” rating among 26 analysts. Of those, 16 have a “Strong Buy” rating, two have a “Moderate Buy” rating, seven have a “Hold” rating, and one rates it as a “Strong Sell.” At the moment, UNH has a mean price target of $396.61, implying a potential 16% gain. The high target is $444, implying potential upside of 30%.

On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Trump Just Juiced the Bull Case for Lockheed Martin to $1.5 Trillion. Does That Make LMT Stock a Buy Here?

- A $2.65 Billion Reason to Buy Bloom Energy Stock in January 2026

- This 1 Greenland Stock Has Surged in the Past Month. Should You Chase the Rally Here?

- This Memory Stock Is Up 745% in the Past 6 Months. Is It Unstoppable?